PUBLISHER: Reed Electronics Research | PRODUCT CODE: 1388512

PUBLISHER: Reed Electronics Research | PRODUCT CODE: 1388512

2023 Yearbook of World Electronics Data - 2 Volume Set: West Europe (Vol 1), plus America, Japan & Asia-Pacific (Vol 2)

VOLUME ONE: WEST EUROPE

Introduction

In providing the forecasts for the current study, which were made in June, we have considered developments in the European and global economy. However, significant downside risks remain which could lead to growth in 2023 and 2024 being lower than forecast. We currently expect growth to ease over the course of the second half of 2023 and into 2024 before gaining momentum in the latter half of the year and then accelerate over the remainder of the forecast period. Component shortages have continued to ease over the course of 2023 and are expected to normalise in 2024. The forecasts for 2023 through to 2026 are based on constant 2022 exchange rates and prices and therefore exclude the impact of inflation.

In Euro's the production of electronic equipment in Western Europe increased by an estimated 5.9% in 2022 to Euro 127.3 billion and compared to growth of 6.4% in the prior year as output rebounded from the pandemic. Based on current indicators we are forecasting that growth in electronic equipment output in Western Europe will ease to 2.2% in 2023, edge-up to 2.9% in 2024 with growth gaining momentum in the second half of the year then accelerate to 3.9% and 4.1% in 2025 and 2026, respectively.

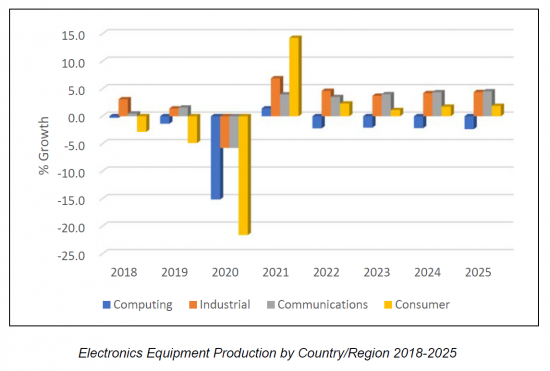

The industrial segment, which accounted for an estimated 61.9% of electronics equipment output in 2022, has been a key driver of growth following the COVID-19 led-recession. Despite the expected slowdown in 2023/2024 growth is forecast to accelerate in the later part of the forecast. By the end of 2026 its share of the total will account for 62.7%.

Growth in the communications segment rebounded in 2021 with growth of 3.9% and increased by a further 4.7% in 2022. Defence spending, which was expected to be reduced as governments look to reduce the deficit arising from measures introduced to support the economy through the pandemic, will benefit from the escalation in geopolitical tensions including the war in Ukraine. The aerospace segment, which was hit hard by the collapse in the commercial aviation sector as a result of the pandemic, is gradually returning to pre-pandemic levels though in the short-term growth is forecast to be impacted by the slowdown in the global economy. Computer output will continue to decline over the forecast period as will the production of video and audio equipment.

In 2022, the production of electronic components in Western Europe amounted to Euro 50.0 billion, 28.2% of overall electronics production. The shortage of components in 2021, which fuelled higher prices and the move by companies to increase output, continued in 2022 leading to a second year of double-digit growth (2021: 14.9%/2022: 12.1%).

In 2022, active components accounted for 62.3%, passive 31.3% and other 6.4% while Germany accounted for the largest share of production at 34.5%, followed by France 14.9%, Ireland 14.7%, Italy 11.1% and the UK 5.6%. With the EU and several countries, notably Germany, France and Italy, looking to secure the future supply of leading-edge semiconductors a number of advanced wafer fabs have been announced with construction planned to start in 2024/2025. In addition, investment has or is being made in existing fabs in the region which will boost output over the period to 2026. Western Europe is also home to a number of fabless semiconductor companies and remains a centre for research and design with a strong start-up culture.

At Euro 257.5 billion in 2022 the West European market for electronic equipment and components was 9.4% higher than the Euro 235.4 billion reported in the prior year and is forecast to reach Euro 262.4 billion in 2023, this despite the anticipated slowdown in the second half of the year.

The Yearbook of World Electronics Data - tracking developments in the global electronics industry

With a history now extending over 50 years, the first edition of the ‘Volume 1 of the Yearbook of World Electronics Data’ was first published in 1973, the Yearbook series has been extended to cover 53 countries globally to provide an invaluable and unique insight into the global trends, regional variations and the underlying state of the global electronics market for all stages of the supply chain - OEM, contract manufacturing and design, components and materials suppliers to financial /industry analysts and government and academia.

Although encompassing a range of published and bespoke products the core of RER's research programme is one of the most comprehensive statistical databases covering the global electronics industry, with the resulting analysis being published through three concise and clear demographic volumes, as a series of individual country reports, through customised solutions to meet specific client requirements and a series of Excel databases providing the combination of both historical and forecasted data.

Published since 1973 the ‘Volume 1 of the Yearbook of World Electronics Data’ provides:

- A single source solution allowing you to track the electronics industry in 16 countries in Western Europe.

- 13 major product groups.

- Market and production forecasts.

- Summaries provided in US dollars and Euros.

- CD-option allows you to manipulate the data quickly and easily: produce your own subsets or summaries of the data, create your own forecasts or cut and paste the data into your own in-house reports and presentations.

VOLUME TWO: AMERICAS, JAPAN, ASIA PACIFIC

In providing the forecasts for the current study, which were made in October 2023, we have considered developments in the global economy. However, significant downside risks remain which could lead to growth in 2023 and 2024 being lower than forecast. We currently expect growth to ease over the final months of 2023 and into 2024 before gaining momentum in the latter half of the year and then accelerate. Component shortages have continued to ease over the course of 2023 and are expected to normalise in 2024. The forecasts for 2023 through to 2026 are based on constant 2022 exchange rates and prices and therefore exclude the impact of inflation.

Americas

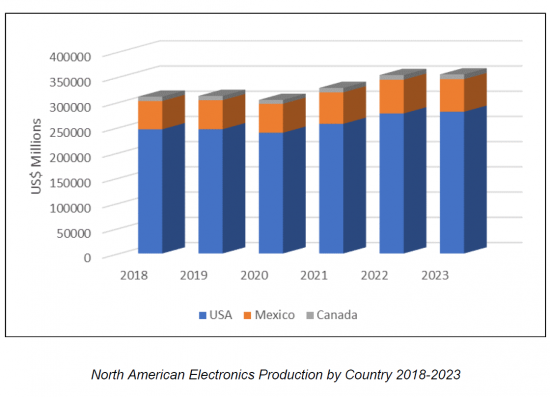

Within the Yearbook series the Americas covers Brazil and the three countries making-up North America. In 2022, electronics production in North America amounted to US$354 billion in 2022 with the US dominating accounting for 78.5% of the total. Mexico, which acts as the low-cost production base for the region, accounted for 18.9% while Canada accounted for only 2.6%. After increasing in US dollars by 7.8% in both 2021 and 2022, growth is forecast to ease to 0.4% in 2023.

The Brazilian electronics industry is focused on the production of electronics equipment with computing, including office equipment, the dominant sector accounting for 48% of total electronics equipment output in 2022 and was followed by communications and radar with a 28% share. Electronic component production at US$2.0 billion accounted for 9.9% of electronics output in 2022.

Japan

After three years of declining output between 2018 and 2020 electronics production posted its second year of consecutive growth in 2022, although at 2.2% it was below the prior year's increase of 8.9%. Based on official figures for the first six months of the year overall electronics output, is forecast to be flat in 2023 an 8.4% rise in electronic equipment production offset by a 6.7% decline in electronics component output.

Asia

In 2022, the production of electronics equipment and components in Asia was valued at US$1,518 billion of which components accounted for 43%. Electronics equipment production, which accounted for 57% of the total, is dominated by computing and communications.

The Yearbook of World Electronics Data - tracking developments in the global electronics industry

With a history spanning 50 years the ‘Yearbook of World Electronics Data’ has provided an invaluable insight into the global trends, regional variations and the underlying state of the global electronics market for all stages of the supply chain - OEM, contract manufacturing and design, components and materials suppliers to financial /industry analysts and government and academia.

Although encompassing a range of published and bespoke products the core of RER's research programme is one of the most comprehensive statistical databases covering the global electronics industry, with the resulting analysis being published through three concise and clear demographic volumes, as a series of individual country reports, through customised solutions to meet specific client requirements and, from 2012, as a series of Excel databases providing the combination of both historical and forecasted data.

Published since 1983 the ‘Volume 2 of the Yearbook of World Electronics Data’ provides:

- A single source solution allowing you to track the electronics industry in 19 countries in the Americas, Japan and Asia Pacific.

- 13 major product groups.

- Market and production forecasts.

- CD-option allows you to manipulate the data quickly and easily: produce your own subsets or summaries of the data, create your own forecasts or cut and paste the data into your own in-house reports and presentations.

Table of Contents

Volume One

1. INTRODUCTION

2. SUMMARY DATA

- 2.1. Economic Overview

- 2.2. Electronics Overview

- 2.3. Imports 2020-2021

- 2.4. Exports 2020-2021

- 2.5. Consolidated Summary of Production 2020

- 2.6. Consolidated Summary of Production 2021

- 2.7. Consolidated Summary of Production 2022

- 2.8. Consolidated Summary of Production 2023

- 2.9. Summary of EDP Production

- 2.10. Summary of Control & Instrumentation Production

- 2.11. Summary of Medical & Industrial Production

- 2.12. Summary of Communications & Radar Production

- 2.13. Summary of Telecommunications Production

- 2.14. Summary of Consumer Production

- 2.15. Summary of Components Production

- 2.16. Summary of Active Component Production

- 2.17. Summary of Passive Component Production

- 2.18. Summary of Other Component Production

- 2.19. West Europe Total Production

- 2.20. Consolidated Summary of Markets 2020

- 2.21. Consolidated Summary of Markets 2021

- 2.22. Consolidated Summary of Markets 2022

- 2.23. Consolidated Summary of Markets 2023

- 2.24. Consolidated Summary of Markets 2024

- 2.25. Consolidated Summary of Markets 2025

- 2.26. Consolidated Summary of Markets 2026

- 2.27. Summary of EDP Markets

- 2.28. Summary of Control & Instrumentation Markets

- 2.29. Summary of Medical & Industrial Markets

- 2.30. Summary of Communications & Radar Markets

- 2.31. Summary of Telecommunications Markets

- 2.32. Summary of Consumer Markets

- 2.33. Summary of Components Markets

- 2.34. Summary of Active Component Markets

- 2.35. Summary of Passive Component Markets

- 2.36. Summary of Other Component Markets

- 2.37. West Europe Total Markets

3. COUNTRY DATA

- 3.1. AUSTRIA

- 3.1.1. Economic Outlook

- 3.1.2. Electronics Industry Overview

- 3.1.3. Austria Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.1.4. Austria Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.2. BELGIUM

- 3.2.1. Economic Outlook

- 3.2.2. Electronics Industry Overview

- 3.2.3. Belgium Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.2.4. Belgium Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- 3.3. DENMARK

- 3.3.1. Economic Outlook

- 3.3.2. Electronics Industry Overview

- 3.3.3. Denmark Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.3.4. Denmark Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.4. FINLAND

- 3.4.1. Economic Outlook

- 3.4.2. Electronics Industry Overview

- 3.4.3. Finland Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.4.4. Finland Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.5. FRANCE

- 3.5.1. Economic Outlook

- 3.5.2. Electronics Industry Overview

- 3.5.3. France Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.5.4. France Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.6. GERMANY

- 3.6.1. Economic Outlook

- 3.6.2. Electronics Industry Overview

- 3.6.3. Germany Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.6.4. Germany Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.7. GREECE

- 3.7.1. Economic Outlook

- 3.7.2. Electronics Industry Overview

- 3.7.3. Greece Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.7.4. Greece Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2013-2019

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.8. IRELAND

- 3.8.1. Economic Outlook

- 3.8.2. Electronics Industry Overview

- 3.8.3. Ireland Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.8.4. Ireland Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.9. ITALY

- 3.9.1. Economic Outlook

- 3.9.2. Electronics Industry Overview

- 3.9.3. Italy Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.9.4. Italy Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.10. NETHERLANDS

- 3.10.1. Economic Outlook

- 3.10.2. Electronics Industry Overview

- 3.10.3. Netherlands Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.10.4. Netherlands Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.11. NORWAY

- 3.11.1. Economic Outlook

- 3.11.2. Electronics Industry Overview

- 3.11.3. Norway Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.11.4. Norway Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.12. PORTUGAL

- 3.12.1. Economic Outlook

- 3.12.2. Electronics Industry Overview

- 3.12.3. Portugal Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.12.4. Portugal Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.13. SPAIN

- 3.13.1. Economic Outlook

- 3.13.2. Electronics Industry Overview

- 3.13.3. Spain Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.13.4. Spain Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.14. SWEDEN

- 3.14.1. Economic Outlook

- 3.14.2. Electronics Industry Overview

- 3.14.3. Sweden Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.14.4. Sweden Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.15. SWITZERLAND

- 3.15.1. Economic Outlook

- 3.15.2. Electronics Industry Overview

- 3.15.3. Switzerland Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.15.4. Switzerland Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.16. UNITED KINGDOM

- 3.16.1. Economic Outlook

- 3.16.2. Electronics Industry Overview

- 3.16.3. UK Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.16.4. UK Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

4. APPENDICES

- 4.1. Consolidated Summary of West European Electronics Production 2020-2023(Euro)

- 4.2. Consolidated Summary of West European Electronics Production 2020-2026(Euro)

- 4.3. Exchange Rates

- 4.4. Guide to Interpretation of the Statistics

- 4.5. Guide to Statistical Trade Classifications

- 4.6. Guide to the Definition of the Electronic Product Headings

- 4.7. List of Sources

Volume 2

1. INTRODUCTION

2. SUMMARY DATA

- 2.1. Economic Overview

- 2.2. Electronics Overview

- 2.2.1. Americas

- 2.2.2. Japan

- 2.2.3. Asia

- 2.3. Imports 2020-2021

- 2.4. Exports 2020-2021

- 2.5. Consolidated Summary of Production 2020

- 2.6. Consolidated Summary of Production 2021

- 2.7. Consolidated Summary of Production 2022

- 2.8. Consolidated Summary of Production 2023

- 2.9. Summary of Medical & Industrial Production

- 2.10. Summary of Consumer Production

- 2.11. Summary of Components Production

- 2.12. Summary of Active Component Production

- 2.13. Summary of Passive Component Production

- 2.14. Summary of Other Component Production

- 2.15. America, Japan, Asia Pacific Total Production

- 2.16. Consolidated Summary of Markets 2020

- 2.17. Consolidated Summary of Markets 2021

- 2.18. Consolidated Summary of Markets 2022

- 2.19. Consolidated Summary of Markets 2023

- 2.20. Consolidated Summary of Markets 2024

- 2.21. Consolidated Summary of Markets 2025

- 2.22. Consolidated Summary of Markets 2026

- 2.23. Summary of Medical & Industrial Markets

- 2.24. Summary of Consumer Markets(Value)

- 2.25. Summary of Components Markets

- 2.26. Summary of Active Component Markets

- 2.27. Summary of Passive Component Markets

- 2.28. Summary of Other Component Markets

- 2.29. America, Japan, Asia Pacific Total Markets

3. COUNTRY DATA

- 3.1. AUSTRALIA

- 3.1.1. Economic Outlook

- 3.1.2. Electronics Industry Overview

- 3.1.3. Australia Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.1.4. Australia Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.2. BRAZIL

- 3.2.1. Economic Outlook

- 3.2.2. Electronics Industry Overview

- 3.2.3. Brazil Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.2.4. Brazil Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.3. CANADA

- 3.3.1. Economic Outlook

- 3.3.2. Electronics Industry Overview

- 3.3.3. Canada Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.3.4. Canada Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.4. CHINA

- 3.4.1. Economic Outlook

- 3.4.2. Electronics Industry Overview

- 3.4.3. China Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.4.4. China Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.5. HONG KONG

- 3.5.1. Economic Outlook

- 3.5.2. Electronics Industry Overview

- 3.5.3. Hong Kong Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.5.4. Hong Kong Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.6. INDIA

- 3.6.1. Economic Outlook

- 3.6.2. Electronics Industry Overview

- 3.6.3. India Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.6.4. India Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.7. INDONESIA

- 3.7.1. Economic Outlook

- 3.7.2. Electronics Industry Overview

- 3.7.3. Indonesia Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.7.4. Indonesia Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.8. ISRAEL

- 3.8.1. Economic Outlook

- 3.8.2. Electronics Industry Overview

- 3.8.3. Israel Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.8.4. Israel Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.9. JAPAN

- 3.9.1. Economic Outlook

- 3.9.2. Electronics Industry Overview

- 3.9.3. Japan Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.9.4. Japan Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.10. MALAYSIA

- 3.10.1. Economic Outlook

- 3.10.2. Electronics Industry Overview

- 3.10.3. Malaysia Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.10.4. Malaysia Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.11. MEXICO

- 3.11.1. Economic Outlook

- 3.11.2. Electronics Industry Overview

- 3.11.3. Mexico Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.11.4. Mexico Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.12. PHILIPPINES

- 3.12.1. Economic Outlook

- 3.12.2. Electronics Industry Overview

- 3.12.3. Philippines Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Other 2020-2023

- 3.12.4. Philippines Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.13. SINGAPORE

- 3.13.1. Economic Outlook

- 3.13.2. Electronics Industry Overview

- 3.13.3. Singapore Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.13.4. Singapore Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.14. SOUTH AFRICA

- 3.14.1. Economic Outlook

- 3.14.2. Electronics Industry Overview

- 3.14.3. South Africa Production

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.14.4. South Africa Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.15. SOUTH KOREA

- 3.15.1. Economic Outlook

- 3.15.2. Electronics Industry Overview

- 3.15.3. South Korea Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.15.4. South Korea Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.16. TAIWAN

- 3.16.1. Economic Outlook

- 3.16.2. Electronics Industry Overview

- 3.16.3. Taiwan Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.16.4. Taiwan Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.17. THAILAND

- 3.17.1. Economic Outlook

- 3.17.2. Electronics Industry Overview

- 3.17.3. Thailand Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.17.4. Thailand Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.18. USA

- 3.18.1. Economic Outlook

- 3.18.2. Electronics Industry Overview

- 3.18.3. USA Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.18.4. USA Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

- 3.19. VIETNAM

- 3.19.1. Economic Outlook

- 3.19.2. Electronics Industry Overview

- 3.19.3. Vietnam Production

- Computing 2020-2023

- Office Equipment 2020-2023

- Control & Instrumentation 2020-2023

- Medical & Industrial 2020-2023

- Communications & Radar 2020-2023

- Telecommunications 2020-2023

- Consumer 2020-2023

- Video 2020-2023

- Audio 2020-2023

- Personal 2020-2023

- Components 2020-2023

- Active 2020-2023

- Passive 2020-2023

- Other 2020-2023

- 3.19.4. Vietnam Markets

- Computing 2020-2026

- Office Equipment 2020-2026

- Control & Instrumentation 2020-2026

- Medical & Industrial 2020-2026

- Communications & Radar 2020-2026

- Telecommunications 2020-2026

- Consumer 2020-2026

- Video 2020-2026

- Audio 2020-2026

- Personal 2020-2026

- Components 2020-2026

- Active 2020-2026

- Passive 2020-2026

- Other 2020-2026

4. APPENDICES

- 4.1. Exchange Rates

- 4.2. Guide to Interpretation of the Statistics

- 4.3. Guide to Statistical Trade Classifications

- 4.4. Guide to the Definition of Electronic Product Headings

- 4.5. List of Sources