PUBLISHER: Analysys Mason | PRODUCT CODE: 955744

PUBLISHER: Analysys Mason | PRODUCT CODE: 955744

Fibre Infrastructure

Please contact us using the inquiry form for pricing information.

OVERVIEW

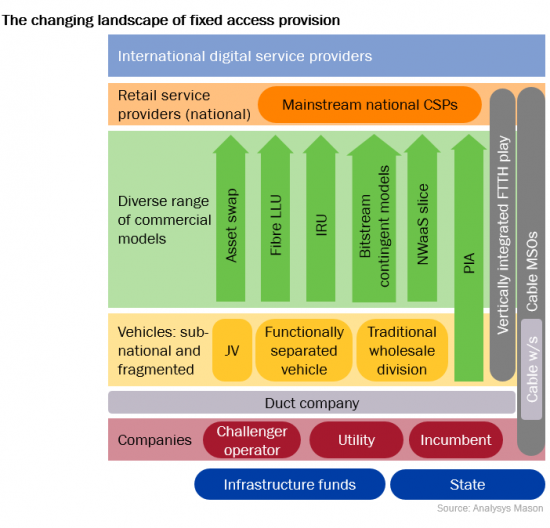

Full fibre build is at the top of the list of investment priorities of many operators, and excites the interest of new investors. It is the quintessential defensible asset, yet operators have to dig deep, metaphorically and literally, to have it, so getting the business model right is critical. Full-fibre broadband will be the main revenue generator, but other use cases bulk up revenue, new technologies can be deployed on the passive network, and possible new end points for the optical distribution network emerge. The programme covers the booming world of fibre access.

KEY THEMES

- Fibre capex, bill of costs and time for deployment

- Fibre coverage

- Business models for fibre monetisation, wholesale

- Emerging fixed access technologies: 10G/50G, SDAN

- Coax and wireless substitutes

- Ownership trends (co-investment, separation, sharing models)

- Policy

RECENTLY PUBLISHED

Strategy reports: key issues

- Decommissioning copper networks: operator case studies

- The future for fixed access OR the re-emergence of fixed-mobile substitution

- 5G fixed-wireless access: more of a challenge than a complement to fixed broadband

- The merits of FTTH infrastructure carve-outs and divestments

Forecasts, datasets and primary research

- FTTx capex and coverage: forecasts and analysis 2019-2025

- FTTx conversion: forecasts and analysis 2019-2025

- FTTx Wholesale Tariff Tracker

COMING IN THE NEXT FEW MONTHS

Strategy reports: key issues

- Strategic option for cable networks in the age of full-fibre

- New FTTP altnets: which models work best

- New FTTx wholesale trends

- Fibre to the everywhere: the case for the ultra-dense fixed network

Forecasts, datasets and primary research

- FTTx capex and coverage: forecasts and analysis 2020-2026

- FTTx conversion: forecasts and analysis 2020-2026

- FTTx Wholesale Tariff Tracker

- Tracker of fixed network sharing, spin-offs and co-investment

Please contact us using the inquiry form for pricing information.