PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1406903

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1406903

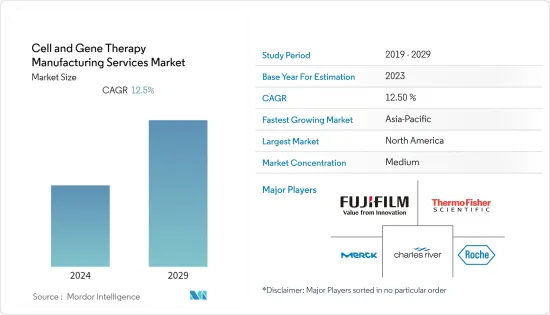

Cell and Gene Therapy Manufacturing Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

The cell and gene therapy manufacturing services market is projected to register a CAGR of 12.5% during the forecast period.

During the COVID-19 pandemic, the cell and gene therapy manufacturing services market was significantly affected. There were two primary reasons for that, the limited running capacity protocols introduced by the governments and the disruption of supply chain and logistics processes. However, new cell and gene therapy products were also launched during the pandemic for the treatment of COVID-19, which also impacted the market growth. For instance, in April 2022, the United States Food and Drug Administration (FDA) granted clearance to BioCardia's Investigational New Drug (IND) application to commence a Phase I/II clinical trial of COVID-19 stem cell therapy, BCDA-04, in adults recovering from COVID-19-linked acute respiratory distress syndrome (ARDS). These new IND applications in the treatment of COVID-19 helped to increase contract manufacturing services among companies. However, as the pandemic has subsided, the market is expected to have pre-pandemic growth levels during the study's forecast period.

Factors driving the market growth include the high prevalence of cancer and other target diseases and increasing R&D investments in pharmaceutical companies. For instance, according to an article published by the Chinese Medical Journal in February 2022, it was estimated that 2022 there were approximately 4,820,000 and 2,370,000 new cancer cases in China and the United States. The most common cancers were lung cancer in China and breast cancer in the United States. As the number of cancer cases increases, the reliance on gene therapy will also increase, thus, boosting the market's growth.

Furthermore, according to the data published by the National Cancer Center of Japan in June 2022, an estimated 158,200 new cancer cases were expected in Japan in the current year, out of which 89,500 were estimated to be in males and 68,700 in females. Such an increasing incidence of colorectal cancer is expected to drive the demand for gene and cell therapy products, fueling segment growth over the forecast period.

Moreover, as per the report published by the Journal of Orthopedic Surgery and Research in October 2021, the pooled prevalence of osteoporosis worldwide was reported to be 18.3%. Stem cell therapy for osteoporosis could potentially reduce the susceptibility to fractures. Thus, with the rising burden of orthopedic disorders, the demand for cell and gene therapy manufacturing services is also expected to grow.

Furthermore, the rising development of cell therapy facilities is also expected to boost the market growth. For instance, in June 2022, OrganaBio, LLC initiated Good Manufacturing Practice (GMP) manufacturing operations at its new cell therapy manufacturing facility in the United States. The new facility offered contract and development manufacturing for custom solutions for therapeutics developers.

Thus the above-mentioned factors such as the rising prevalence of various diseases such as cancer and osteoporosis, among others are expected to drive the growth of the studied market during the forecast period. However, high operational costs associated with the cell and gene therapy manufacturing are expected to restrain the market growth.

Cell and Gene Therapy Manufacturing Services Market Trends

Allogeneic Segment is Expected to Have a Significant Market Share During the Forecast Period

Allogeneic therapies rely on a single source of cells to treat many patients. They increase the risk of eliciting an immune response within a patient, and immunosuppressive therapies are sometimes administered with allogeneic products. Therefore, the increasing inclination of physicians toward the therapeutic use of allogeneic therapies and rising awareness about the use of cord cells and tissues across various therapeutic areas are some of the major factors driving growth. Allogenic cells have benefits as they produce immune stem cells that kill the cancer cells that remain even after high-dose treatment with cytotoxic drugs. The primary factors driving the growth are increasing awareness about allogeneic cell therapy, growing to fund new cell lines, increasing partnerships and acquisitions, and the development of advanced genomics methods for cell analysis.

For instance, in January 2022, Century Therapeutics and Bristol-Myers Squibb signed a research collaboration and license agreement to develop and commercialize up to four induced pluripotent stem cell-derived, engineered natural killer cell or T-cell programs for hematologic malignancies and solid tumors. These collaboration and license agreements are expected to significantly impact this segment's market growth.

Furthermore, in April 2023, the FDA approved Gamida Cell's allogenic stem cell transplant (SCT) therapy, Omisirge (omidubicel), for treating blood cancer patients undergoing SCT. The pivotal phase III trial found Omisirge superior to standard cord blood regarding median time to neutrophil engraftment. Such product approvals are expected to increase the demand for allogenic cell therapy manufacturing services during the forecast period.

Thus, all the above partnerships, collaborations, and license agreements among the companies are expected to augment cell therapy manufacturing services through the segment.

North America is Expected to Hold a Significant Share in the Market Over the Forecast Period

The United States is the most affected country worldwide, as gene therapies are widely used in diagnostic, therapeutic, drug discovery, or other research for oncology and other clinical disorders. Thus, the demand for the same will be significantly high in the North American region, as the patient population is increasing compared to other countries.

North America is expected to hold a significant share of the global cell and gene therapy manufacturing services market due to the rise in the geriatric population and the increasing prevalence and incidence of infectious diseases in this region. For instance, according to the data published by the Canadian Cancer Society in May 2022, around 24,300 Canadians were diagnosed with colorectal cancer, representing 10% of all cancer cases in Canada. The report also mentioned that 1 in 18 Canadian women developed colorectal cancer, and 1 in 14 Canadian men developed colorectal cancer in the current year. These factors increase demand for oncology cell and gene therapies in the region.

Moreover, the increase in research and development activities and the presence of favorable healthcare infrastructure are fueling the growth of the overall regional market to a large extent. For instance, in November 2022, Charles River Laboratories International, Inc. expanded its cell therapy contract development and manufacturing (CDMO) facility in Memphis, United States. The expanded space was suitable for clinical and commercial cell therapy manufacturing. This increase in the growth of the pharmaceutical sector facilitates the increasing cell and gene therapy manufacturing services, thereby propelling the growth of the market.

Thus, the factors mentioned above, such as the increasing prevalence of cancer and the development by various companies, are expected to drive the growth of the market in this region.

Cell and Gene Therapy Manufacturing Services Industry Overview

The cell and gene therapy manufacturing services market is consolidated, competitive, and consists of several major players. A few of the major players are currently dominating the market in terms of market share. Some companies currently dominating the market are Thermo Fisher Scientific Inc., Merck KGaA, Charles River Laboratories, Lonza, Catalent Inc., Takara Bio Inc., and F. Hoffmann-La Roche Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Prevalence of Cancer and Other Target Diseases

- 4.2.2 Increasing Grants and R&D Investments in the Pharmaceutical Sector

- 4.2.3 Increasing Organic and Inorganic Developments Between Pharmaceutical Companies and CDMOs

- 4.3 Market Restraints

- 4.3.1 High Operational Costs Associated with the Cell and Gene Therapy Manufacturing

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Service Type

- 5.1.1 Cell Therapy

- 5.1.1.1 Allogeneic

- 5.1.1.2 Autologous

- 5.1.1.3 Viral Vector

- 5.1.2 Gene Therapy

- 5.1.2.1 Non-viral Vectors

- 5.1.2.2 Viral Vectors

- 5.1.1 Cell Therapy

- 5.2 By Application

- 5.2.1 Clinical Manufacturing

- 5.2.2 Commercial Manufacturing

- 5.3 By Indication

- 5.3.1 Oncology

- 5.3.2 Cardiovascular Diseases

- 5.3.3 Orthopedic Diseases

- 5.3.4 Infectious Diseases

- 5.3.5 Other Indications

- 5.4 By End User

- 5.4.1 Pharmaceutical and Biotechnology Companies

- 5.4.2 Academic and Research Institutes

- 5.4.3 Other End Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Catalent Inc.

- 6.1.2 Cell and Gene Therapy Catapult

- 6.1.3 Charles River Laboratories

- 6.1.4 F. Hoffmann-La Roche Ltd

- 6.1.5 Fujifilm Holdings Corporation

- 6.1.6 Lonza

- 6.1.7 Merck KGaA

- 6.1.8 Nikon CeLL innovation Co. Ltd

- 6.1.9 Oxford Biomedica PLC

- 6.1.10 Takara Bio Inc.

- 6.1.11 Thermo Fisher Scientific Inc.

- 6.1.12 WuXi AppTec

7 MARKET OPPORTUNITIES AND FUTURE TRENDS