PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1437322

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1437322

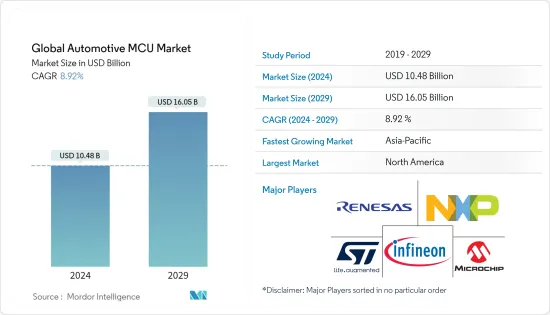

Global Automotive MCU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Global Automotive MCU Market size is estimated at USD 10.48 billion in 2024, and is expected to reach USD 16.05 billion by 2029, growing at a CAGR of 8.92% during the forecast period (2024-2029).

An increased demand for devices designed for extreme operating conditions, providing real-time response and high reliability, even in extreme temperatures, and incorporating features for functional safety to meet automotive design challenges, is expected to offer lucrative opportunities for growth of the studied market.

Key Highlights

- The rise in automation has generated a significant need for microcontrollers responsible for the automatic operation of vehicle functions. MCUs are being used in automobiles to perform automatic functions like keeping the exhaust system clean, distributing electricity to various vehicle components, and reducing fuel consumption. Further, the electrification of vehicles is creating a need for new and specialized MCUs that are optimized for the needs of electric vehicles (EVs). To cater to the upsurge in demand for EVs, companies in the market are innovating advanced products and investing in extensive R&D projects.

- For instance, aiming to keep the impetus going for zonal architecture-related solutions, in February 2022, ST released Stellar E MCUs, a new offering optimized for software-defined EVs Built around 32-bit, 300 MHz Arm Cortex-M7 cores. The MCUs feature up to 2 MB of on-chip Flash and 16 Kbyte of cache per core. The new MCUs, an extension of the Stellar family, are meant to be powerful, centralized domain and zone controllers to simplify design and scalability for a zonal architecture automobile. Also, the new MCUs aim to allow for easy control of wide-bandgap power electronics, such as silicon carbide, which has become a mainstay for efficient power conversion in EVs.

- Additionally, in July 2021, Sterling Gtake E-mobility Ltd, a manufacturer of motor control units for electric vehicles, announced that it had bagged an order worth INR 60 crore from a leading electric two-wheeler maker. The company said it is also in the advanced stages of discussions with over 20 electric vehicle (EV) manufacturers to supply motor control units (MCUs) for different vehicle types, including two-wheelers and three-wheelers passenger vehicles and commercial vehicles.

- On the flip side, as the global automotive sector is recovering from a slump in sales caused by Covid-19, another crisis is dampening its revival. A global semiconductor shortage disrupts global automotive production and may cause a delay in the sales of new vehicles. Microcontrollers, a crucial component of electronic control units used in modern infotainment systems, anti-lock braking systems (ABS), advanced driver assist systems (ADAS), and other electronic stability systems are in short supply forcing carmakers to reduce output. Resultantly, the carmakers are selectively idling plants until the shortage eases. However, the market is expected to make quick progress in the near future.

- Moreover, the possibilities of operational failure of the automotive MCUs in extreme climatic conditions, coupled with their design complexity, might hamper the growth of the studied market.

Automotive Microcontrollers Market Trends

Surging Demand for ADAS is Likely to Drive the Market Growth

- According to World Health Organization (WHO), approximately 1.3 million people die each year due to road traffic crashes which cost most countries approximately 3% of their gross domestic product (GDP). Further, according to Safe International Road Travel, more than 46,000 people die in crashes on U.S. roadways every year. The U.S. traffic fatality rate is 12.4 deaths per 100,000 inhabitants. An additional 4.4 million are injured seriously enough to require medical attention. Road crashes are the leading cause of death in the U.S. for people aged 1-54. Also, the U.S. suffers the most road crash deaths of any high-income country, about 50% higher than similar countries in Western Europe, Canada, Australia, and Japan.

- Vehicles installed with Advanced Driver Assistance Systems (ADAS) can detect and classify objects on the road and alert drivers according to the road conditions. Additionally, these systems can automatically decelerate vehicles, depending on the situation. A few essential safety-critical ADAS applications include pedestrian detection/avoidance, lane departure warning/correction, traffic sign recognition, automatic emergency braking, blind-spot detection, etc. These lifesaving systems are crucial to ensuring the success of ADAS applications, incorporating the latest interface standards, and running multiple vision-based algorithms to support real-time multimedia, vision co-processing, and sensor fusion subsystems.

- According to National Safety Council, ADAS technologies have the potential to prevent 20,841 deaths per year, or about 62% of total traffic deaths. The emergence of advanced driver assistance systems (ADAS) is changing how designers use, specify, and manufacture microcontrollers (MCUs). The evolving and complex nature of ADAS is expected to offer several opportunities for innovation, collaborations, and technological breakthroughs in the studied market.

- For instance, in April 2022, SemiDrive Technology Ltd., a Chinese smart car microchip designer, released its E3 series microcontrollers. The automotive microcontroller adopts a TSMC 22nm automotive grade which can be used in many automotive application fields such as chassis by wire, brake control, BMS, ADAS, LCD panel, HUD, streaming media system, and CMS, among others. It is designed to reach high stability and safety levels. Its vehicle specification is AEC-Q100 Grade 1, and the functional safety standard is ISO 26262 ASIL D.

- Moreover, in March 2022, Renesas Electronics, a supplier of advanced semiconductor solutions, announced the expansion of its collaboration with Honda in the field of advanced driver-assistance systems (ADAS). Honda adopted Renesas' R-Car automotive system on a chip (SoC) and RH850 automotive MCU for its Honda SENSING Elite system. Honda SENSING Elite (featured in the Legend, which went on sale in March 2021) incorporates advanced technology that qualifies for Level 3 automated driving (conditional automated driving in limited areas). Further, Honda has selected R-Car and RH850 for use in the Honda SENSING 360 omnidirectional safety and driver assistance system, which builds on the knowledge and expertise gained through research and development work on the earlier technology.

The Asia Pacific Region is Expected to Witness a High Market Growth

- The growing environmental concerns and rising government subsidy programs, coupled with factors such as better fuel economy, enhanced performance, and reasonable cost, are augmenting the penetration rate of hybrid electric vehicles in the Asia-Pacific region.

- For instance, according to EV-Volumes.com, approximately 672.9 thousand plug-in hybrid electric vehicles (PHEVs) were sold across the Asia-Pacific region in 2021. This was a dramatic increase from 2020 when around 264.26 thousand plug-in hybrid electric vehicles were sold. The increasing demand for these vehicles is likely to boost the maker growth of automotive MCUs in the region.

- Further, the Asia Pacific has emerged as a significant hub for manufacturing semiconductors and semiconductor-based devices. For instance, according to World Semiconductor Trade Statistics (WSTS) estimates, the semiconductor industry revenue in the Asia Pacific region (excluding Japan) was USD 257.88 billion in 2019 and USD 290.85 billion in 2021. The region is also home to prominent electronics and automotive manufacturing companies, thus, offering scope for the evolution of the studied market.

- The future of automotive system design lies in a vehicle-centralized, zone-oriented E/E architecture, which heightens the need for automotive chips that address the challenges these innovative architectures create for future vehicle generations. The companies in the region are launching advanced solutions to cater to the needs of their consumers.

- For instance, in November 2021, Renesas Electronics Corporation (Tokyo, Japan) introduced a powerful new group of microcontrollers (MCUs), the RH850/U2B MCUs, designed to address the growing need to integrate multiple applications into a single chip and realize a unified electronic control unit (ECU) for the evolving electrical-electronic (E/E) architecture. Delivering a combination of flexibility, high performance, freedom from interference, and security, the cross-domain RH850/U2B MCUs are built for the rigorous workloads required by vehicle motion in terms of hybrid ICE and xEV traction inverter, connected gateway, high-end zone control, and domain control applications.

Automotive Microcontrollers Industry Overview

The global automotive MCU market is moderately fragmented with the presence of prominent players like Infineon Technologies AG, Microchip Technology Inc., NXP Semiconductors, Texas Instruments Incorporated, etc. The competition, frequent changes in consumer preferences, and rapid technological advancements are expected to pose a threat to the market's growth during the forecast period.

- January 2022 - Infineon Technologies announced the extension of its AURIX microcontroller family and the availability of the first samples of its new AURIX TC4x family of 28nm microcontrollers for next-generation eMobility, ADAS, automotive E/E architectures, and affordable artificial intelligence (AI) applications. The new family delivers an upward migration path for the company's leading AURIX TC3x MCU family. It features the next-generation TriCore 1.8 and scalable performance enhancements from the AURIX accelerator suite.

- April 2021 - Nuvoton Technology Corporation launched a new series of Arm Cortex-M0 NUC131U 32-bit microcontrollers for automotive applications, running up to 50 MHz, qualified by AEC-Q100 Grade 2 and build-in Controller Area Network (CAN) 2.0 B interface. It is equipped with a rich peripheral comprising six sets of UARTs, two sets of I2Cs, 1 set of SPI, and 24 channels of 100 MHz PWM to make accurate control to drive both stepping motor or HVAC compressor. 12-bit ADC delivers up to 800 k SPS to sense voltage, current, or temperature sensors for automotive applications to reduce the number of external peripheral components and the form factor of the end product.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption And Market Defination

- 1.2 Scope of the study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Primary Research Approach And Key Respondents

- 2.5 Data Triangulation And Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power Of Suppliers

- 4.2.2 Bargaining Power Of Buyers

- 4.2.3 Threat Of New Entrants

- 4.2.4 Threat Of Substitutes

- 4.2.5 Intensity Of Competitive Rivalry

- 4.3 Value Chain Analysis

- 4.4 Assessment of the Impact of Covid-19 on the Market

- 4.5 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Emergence of Internet of Things (IoT)

- 5.1.2 Surge in demand for electronic vehicles (Evs)

- 5.1.3 Increasing popularity of infotainment in automobiles

- 5.2 Market Challenges/Restraints

- 5.2.1 Operational failure in extreme climatic conditions

- 5.2.2 Design Complexity

- 5.3 Market Opportunities

- 5.3.1 Technological Advancements and Innovations

6 MARKET SEGMENTATION

- 6.1 Segmentation - By Product

- 6.1.1 8-bit

- 6.1.2 16-bit

- 6.1.3 32-bit

- 6.2 Segmentation - By Application

- 6.2.1 Powertrain and Chassis

- 6.2.2 Safety and Security

- 6.2.3 Body Electronics

- 6.2.4 Telematics and Infotainment

- 6.3 Segmentation - By Vehicle Type

- 6.3.1 Passenger ICE vehicle

- 6.3.2 Commercial ICE vehicle

- 6.3.3 Electric Vehicle

- 6.3.3.1 BEV

- 6.3.3.2 HEV

- 6.3.3.3 PHEV

- 6.3.3.4 FCEV

- 6.4 Segmentation - By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Infineon Technologies AG

- 7.1.2 Microchip Technology Inc.

- 7.1.3 NXP Semiconductors

- 7.1.4 Renesas Electronics Corporation

- 7.1.5 STMicroelectronics

- 7.1.6 Texas Instruments Incorporated

- 7.1.7 Toshiba Electronic Devices & Storage Corporation

- 7.1.8 Analog Devices Inc.

- 7.1.9 ROHM Semiconductor

- 7.1.10 Broadcom Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET