PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1441664

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1441664

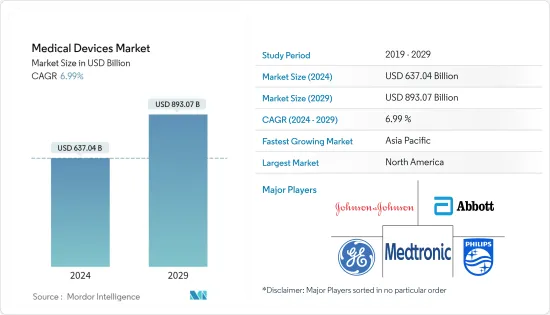

Medical Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Medical Devices Market size is estimated at USD 637.04 billion in 2024, and is expected to reach USD 893.07 billion by 2029, growing at a CAGR of 6.99% during the forecast period (2024-2029).

The COVID-19 pandemic severely impacted the overall medical devices market, with the various segments experiencing wide-ranging effects. The pandemic resulted in postponements and cancellations of non-essential and elective procedures. For instance, as per an article published in a healthcare journal in August 2022, titled "COVID-19 impact on diagnostic imaging procedures in UAE," there were around 80% fewer radiological procedures performed during the pandemic compared to pre-COVID times. This declining number of radiological procedures further decreased the demand for medical devices, which affected the market's growth during the COVID-19 pandemic.

However, the studied market supplying hospital equipment for the management of COVID-19, such as personal protective equipment (PPE), ventilators, and general hospital supplies, experienced a surge in sales to fulfill the overwhelming demand. For instance, ventilators, an important equipment for COVID-19 patients in critical conditions, were in high demand during the pandemic. In March 2020, Medtronic increased the production of ventilators by more than 40% to date. This impacted the growth of medical devices during the pandemic.

Factors such as the rising prevalence of chronic and related increases in disability-adjusted life years, technological advancements in medical devices, and a consistent increase in the aging population are boosting market growth.

The geriatric population is more likely to acquire age-related diseases that are less prevalent among younger people. For instance, as per a research study published in December 2021, the overall self-reported prevalence of diagnosed cardiovascular diseases (CVDs) in people aged 45 years and above was 29.4%. As per the same source, this prevalence rate increased with age, from 22% in the 45-54 age group to 38% in the 70+ age group, indicating that the geriatric population is at high risk of developing CVDs. This finding is expected to increase the demand for cardiac surgeries and devices that help in regularly monitoring heart conditions, thereby propelling the market's growth.

Additionally, the increasing burden of chronic diseases worldwide is driving the demand for effective and advanced treatment services that involve various diagnostic and surgical procedures. Thus, the demand for medical devices across the world is increasing. For instance, according to 2022 statistics published by IDF, about 2.9 million people were living with diabetes in Canada in 2021. In addition, as per the same source, this number is projected to reach 3.2 million and 3.4 million by 2030 and 2045, respectively. Thus, the expected increase in the number of people who have diabetes may propel the demand for various wearable and portable medical devices to regularly monitor the condition.

Moreover, the rising focus on developing technologically advanced medical devices and increasing product launches are also contributing to the market growth. For instance, in May 2022, Max ventilator launched multifunctional noninvasive ventilators, which come with inbuild oxygen therapy and humidifier, in India. Also, in April 2022, Medline UNITE launched Calcaneal Fracture Plating System and IM Fibula Implant. The launch provides a comprehensive titanium foot and ankle trauma system to address nearly all fractures requiring ORIF with plate and screw fixation.

However, strict regulations and uncertainty in reimbursement are likely to impede the growth of the medical devices market over the forecast period.

Medical Device Technologies Market Trends

Cardiology Devices Segment is Expected to Hold a Major Share in the Medical Device Market Over the Forecast Period

The cardiology segment is expected to witness significant growth in the medical devices market over the forecast period owing to factors such as the rising prevalence of cardiovascular diseases, strategic initiatives by key market players, and technological advancement in cardiology devices.

In addition, the increasing incidence and prevalence of obesity, diabetes, hypertension, and high cholesterol are also contributing to the demand for cardiological medical devices, as patients suffering from these diseases are likely to develop cardiac complications in their lifetime.

Cardiovascular devices are used for the diagnosis of heart diseases and the treatment of related health problems. The devices used in cardiology are classified into three categories, namely surgical, therapeutic, and diagnostic. Some of the widely used cardiovascular devices are electrocardiograms (ECG), defibrillators, pacemakers, cardiac rhythm management devices, catheters, grafts, heart valves, and stents.

The growing number of people suffering from cardiovascular diseases is the key factor driving the demand for medical devices. For instance, as per the 2021 data published by CDC, it has been observed that every year, 805,000 people in the United States have a heart attack, 605,000 of these result in a first-time heart attack, while 200,000 are caused by previous heart attacks in 2020. Additionally, according to 2021 statistics published by the American Heart Association, it was estimated that by the year 2035, more than 130 million adults in the United States will have some type of heart disease.

Moreover, growth in company activities and increasing technological advancements (such as the use of artificial intelligence in cardiac wearable devices) have led to an increasing number of patients being managed with cardiology devices, resulting in exponential therapeutical and monitoring outcomes. This is expected to increase the growth of the studied segment over the forecast period. For instance, in April 2022, Translumina launched its Dual Drug Polymer-Free Coated Stent named VIVO ISAR in the European market. Also, in June 2021, Medtronic launched Micra AV, a miniaturized, fully self-contained pacemaker that delivers advanced pacing technology to atrioventricular (AV) block patients via a minimally invasive approach. The device can sense atrial activity without a lead or device in the upper chamber of the heart.

Therefore, owing to the aforesaid factors, the segment is expected to witness growth over the forecast period.

North America Dominates the Market and is Expected to Continue the Growth Trend During the Forecast Period

North America is expected to dominate the medical devices market over the forecast period owing to the factors such as the growing burden of chronic diseases, high healthcare expenditures, and the presence of key players.

In addition, the increasing geriatric population is likely to increase the market growth over the forecast period. For instance, according to the 2022 statistics published by the United Nations Population Fund, in Canada, a large proportion of the population is estimated to be aged between 15 and 64 years and accounts for 65% of the total population in the current year. In addition, as per the same source, 19% of the population is aged 65 years and above in 2022 in Canada. Thus, the rising geriatric population is more prone to develop chronic diseases such as cardiopulmonary diseases, respiratory diseases, and orthopedic disorders, which increase the demand for diagnostic imaging as well as surgical procedures; this, in turn, is anticipated to fuel the growth of the medical devices, thereby propelling the market growth over the forecast period.

The rising prevalence of chronic diseases such as cardiovascular diseases, coronary heart diseases, stroke, and rising respiratory diseases such as acute respiratory syndrome among the population, leads to increased cardiopulmonary bypass procedures, resulting in an increasing demand for medical devices. For instance, according to 2022 statistics published by American Heart Association (AHA), the prevalence rate of heart failure in the United States in 2021 was 6 million, which is 1.8% of the total population. Thus, the high burden of cases of heart failure in the country is expected to increase the demand for medical devices for better diagnosis and treatment, which is further expected to boost the growth of the market over the forecast period.

Similarly, from a research study published by Cardiovascular Diabetology in June 2021, it was observed that a 31% increase in physical inactivity resulted in an increase in the number of cases of Type II diabetes (27,100), coronary heart disease (10,300), stroke (2200), myocardial infarction (1500), stroke deaths (400), and coronary heart disease deaths (350). Thus, changing lifestyles leading to physical inactivity can further increase the risk of heart disease, which is expected to increase the demand for medical devices due to increased heart surgeries to open the blocked arteries in patients, thereby boosting market growth.

Furthermore, the growing focus of companies on developing advanced products and adopting various business strategies, such as collaborations and acquisitions to withhold their market position, is also contributing to the market growth. For instance, in March 2022, Respira Labs, a respiratory healthcare tech business based in the United States, released Sylvee, an AI-powered wearable lung monitor that employs acoustic resonance to assess lung function and identify variations in lung air volume. It can aid in the early detection and treatment of chronic obstructive pulmonary disease (COPD), asthma, and COVID-19.

Moreover, in January 2021, PENTAX Medical increased the availability of the CapsoCam Plus video capsule system with Health Canada licensing in partnership with CapsoVision, Inc. This product expansion enables at-home administration of the CapsoCam Plus small bowel capsule endoscope during the COVID-19 pandemic for eligible patients, permitting a fully remote capsule endoscopy procedure and effectively eliminating the need for in-person interactions between clinicians and their patients.

Therefore, owing to the aforesaid factors, the market is expected to witness growth over the forecast period.

Medical Device Technologies Industry Overview

The medical devices market is competitive and consists of several major players. Companies like Abbott Laboratories Inc, F. Hoffmann-La Roche Ltd, Philips Healthcare, Siemens Healthineers (Siemens AG), Stryker Corporation, Boston Scientific Corporation, Johnson & Johnson, Medtronic PLC, Smith & Nephew PLC, and GE Healthcare hold substantial shares in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Geriatric Population Across the World

- 4.2.2 Rising Prevalence of Chronic Diseases and Related Increase in Disability-adjusted Life Years

- 4.3 Market Restraints

- 4.3.1 Strict Regulatory Polices and Uncertainty in Reimbursement

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Type of Device

- 5.1.1 Respiratory Devices

- 5.1.2 Cardiology Devices

- 5.1.3 Orthopedic Devices

- 5.1.4 Diagnostic Imaging Devices (Radiology Devices)

- 5.1.5 Endoscopy Devices

- 5.1.6 Ophthalmology Devices

- 5.1.7 Other Devices

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Middle East & Africa

- 5.2.4.1 GCC

- 5.2.4.2 South Africa

- 5.2.4.3 Rest of Middle East & Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott Laboratories Inc

- 6.1.2 Boston Scientific Corporation

- 6.1.3 F. Hoffmann-La Roche Ltd

- 6.1.4 GE Healthcare (General Electric Company)

- 6.1.5 Johnson & Johnson

- 6.1.6 Medtronic PLC

- 6.1.7 Koninklinje Philips NV

- 6.1.8 Siemens Healthineers (Siemens AG)

- 6.1.9 Smith & Nephew PLC

- 6.1.10 Stryker Corporation

- 6.1.11 Fresenius Medical Care AG & Co. KGaA

- 6.1.12 3M Company

- 6.1.13 Cardinal Health Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS