PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1406118

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1406118

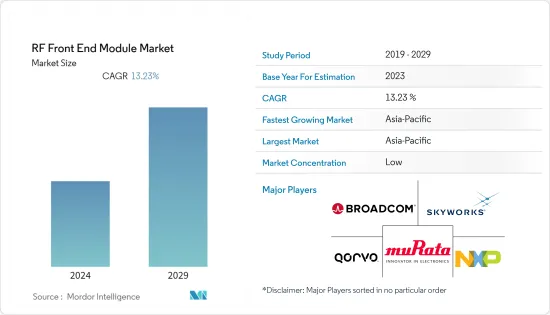

RF Front End Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

The RF Front End Module Market size is expected to grow from USD 25.83 billion in 2024 to USD 42.45 billion by 2029, at a CAGR of 13.23% during the forecast period (2024-2029).

In recent years, the development of low-cost nanosatellites has grown considerably. It has been made viable due to the availability of low-cost launch vectors and "commercial off-the-shelf components" (COTS). Most COTS components are usually not space-qualified, and to make them work and withstand the harsh space environment, they need extra effort in-circuit redesign and implementation. The RF front-end design is considered one of the better and more feasible choices in expert research, which consists of an S-band transceiver that is fully implemented using COTS components. If further implemented in nanosatellites, the market in this sector shall grow significantly during the forecast period.

Key Highlights

- An RF front-end module refers to the circuitry in a radio receiver circuit between a radio receiver's antenna input and the mixer stage or the transmitter's power amplifier.

- The exponential increase in mobile communication devices on a unit basis and rising data traffic due to data-intensive applications have led RF FEM providers to lead innovation, such as high-frequency bands in handsets. Additionally, per the Cisco Visual Networking Index, the global mobile data traffic is expected to increase sevenfold between 2017 and 2022, with a CAGR of 46%, reaching 77.5 exabytes per month by 2022.

- Qorvo introduced the first dual-band front-end module (FEM) for Wi-Fi 6, the SKY85334-11 and SKY85750-11. It is designed ideally for customer premise equipment (CPE), combining the performance required to deliver HD/4K video with the efficiency needed for IoT. Also, by featuring linearity, power dissipation, and efficiency for access points, routers, and gateways, where regulatory, thermals or Power-over-Ethernet (PoE) limitations demand low current consumption, the modules overlook integration at switching, low-noise amplifier (LNA) with bypass and power amplifier (PA) as applications.

- Moreover, the constant increase in defense budgets in developing and developed nations and the demand for technologically-advanced products in the arsenal of national and international armed forces are expected to further fuel the global market's growth. Military radio frequency and electronic warfare applications are expected to grow in addition to the technological advancements in autonomous vehicles and drones.

- RF power amplifiers (PA), thus, form an integral part of all the base stations for wireless mobile infrastructure. They represent one of the most expensive components of sub-assemblies in modern infrastructure equipment. The GaN RF semiconductors used in these power amplifiers must evolve with the economic and technical realities facing the designers and users of these RF PAs.

- Due to government-imposed lockdowns and travel and trade restrictions, many industries, such as electronics, automotive, aerospace & defense, and telecommunications, were forced to shut down their operations, lowering the demand for RF power semiconductors in 2020. As of 2022, several RF component makers have reorganized their supply chains by working with regional raw material suppliers. In the future, this is projected to reduce the burden of the COVID-19 pandemic on producers.

Radio Frequency (RF) Front End Module Market Trends

RF Filters to Witness Significant Growth

- Radiofrequency (RF) filters are widely used in the communication industry to eliminate white noise interference when receiving and transferring data across various channels. These filters are often employed in operating fields, such as television broadcasting, wireless communication, and radios operating from medium to high frequencies. This is done to provide reliable, error-free, and appropriate communication from one end to the other. Band-reject, high-pass, band-pass, and low-pass filters are the four types of RF filters.

- RF filters are used with radio receivers to ensure that only the appropriate frequencies are broadcasted, filtering out undesirable bands of frequencies. They are a crucial component of wireless technology. These filters are built to function at frequencies ranging from medium to extremely high, such as megahertz and gigahertz. Due to their working feature, they are most commonly employed in equipment like broadcast radio, wireless communications, and television.

- Mobile computing devices are becoming more popular among mobile users and business travelers who need constant mobility and connection. Consumers use these gadgets for various tasks, including accessing social media applications, surfing the web, reading news, and checking emails. The growing internet penetration rate and the availability of high data rates at affordable speeds are driving the demand for mobile computing devices.

- Network traffic is increasing exponentially, owing to the growing use of mobile computing devices. The proliferation of mobile computing devices (such as smartphones, tablets, and laptops) with increased capabilities is driving internet bandwidth. The increased need for new RF functionalities in smartphones and tablets has resulted from incorporating advanced wireless technologies, such as LTE and Wi-Fi.

- Furthermore, RF filters play an essential function in the cell phone environment. Mobile phones, for example, require a particular number of bands to function effectively. Without the right RF filter, the various bands cannot coexist simultaneously. This will result in the rejection of certain bands, such as the Wi-Fi, public safety, and global navigation satellite system (GNSS). RF filters are crucial because they allow all bands to coexist simultaneously.

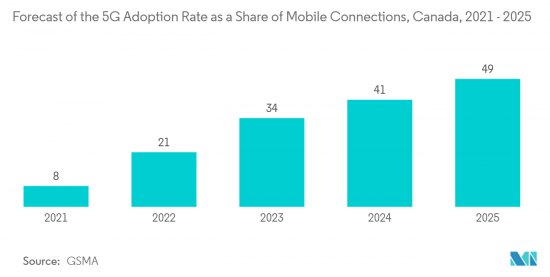

- The increasing demand for 5G smartphones will further boost the demand for RF filters. According to GSMA, the 5G adoption rate as a share of mobile connections in Canada will reach 49% by 2025 from 8% in 2021.

Asia-Pacific to Witness Significant Growth

- The Asia-Pacific is expected to witness significant growth. The advancement in consumer electronics and growing defense equipment requirements with the considerable growth of major emerging economies, such as China, India, and South Korea, will further boost the demand for the RF component market.

- The flourishing Integrated Circuit (IC) industry, expanding the SOI ecosystem in the Asia-Pacific, and increasing the use of SOI in IoT applications act as growth opportunities for the RF Front End Module (RFFE). According to Forbes, the number of IoT devices will surpass 3.5 billion by 2023, with Asia leading the highest market share. By 2023, Northeast Asia will be a market for more than 2.2 billion devices.

- For data transmission over 2G, 3G, and 4G/ Long-term Evolution (LTE), mobile devices require dedicated front-end modules (FEMs). FEMs use RF-SOI chips, which integrate switches, power amplifiers, antenna tuning components, power management units, and filters on a single platform for IoT applications. Hence, this caters to the market growth in the region.

- Further, increasing the production of vehicles in the Asia-Pacific is expected to drive the demand for compact dual-band RF front-end modules for global positioning system (GPS) operating in the L1-band (1574.42-1576.42 MHz) and satellite digital audio radio system (SDARS) operating in the S-band (2320-2345 MHz. This, in turn, may boost the market in the region. China is the largest maker of electric vehicles and leads with the highest level of EV uptake over the projection period. By 2030, the share of EVs in new vehicle sales is estimated to reach 57% across all road transport modes (i.e., two-wheelers, cars, buses, and trucks).

- Furthermore, as front-end modules are essential to many wireless applications, such as base stations and 5G smartphones, China's massive capital investment project designed to nurture the domestic semiconductor industry has rolled out its second funding phase. The project is scheduled for the next five years with a budget of YUAN 204.15 billion (USD 28.9 billion). By addressing RF front-end modules, Huawei creates an opportunity to ponder areas that need attention for developing the necessary technologies, designs, and IPs, possibly expected to begin designing a whole integrated module system in China. This further penetrates future growth for the market.

Radio Frequency (RF) Front End Module Industry Overview

The RF front-end module market is fragmented due to high market rivalry. With increasing innovation, partnerships, and mergers, the market is expected to have high competition in the forecasted period. Key players in the market are Broadcom Inc., Skyworks Solutions, Inc., etc.

In June 2022, Qualcomm Technologies Inc. announced the launch of Wi-Fi 7 front-end modules that offered enhanced wireless performance in automotive and internet-connected devices. The introduction of the RFFE modules aligned with the company's objective to extend its handset range with modem-to-antenna solutions for automotive and IoT.

In February 2022, Murata Manufacturing announced the expansion of its millimeter-wave RF front-end portfolio for 5G wireless infrastructure applications. The three beam-forming ICs and two up-down converters offered flexibility to interchange ICs for full IF-to-RF coverage across the n257, n258, and n260 bands.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope Of The Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment Of The Impact Of COVID-19 On The Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Popularity of RF-SOI and the Increasing Adoption of Smart Devices

- 5.1.2 Adoption of Bluetooth IoT Applications

- 5.2 Market Challenges

- 5.2.1 Low Demand due to the Impact of COVID-19

- 5.2.2 Expensive to Fabricate and Smaller Wafer Sizes

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 RF Filters

- 6.1.2 RF Switches

- 6.1.3 RF Power Amplifiers

- 6.1.4 Other Components

- 6.2 By Application

- 6.2.1 Consumer Electronics

- 6.2.2 Automotive

- 6.2.3 Military

- 6.2.4 Wireless Communication

- 6.2.5 Other Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 India

- 6.3.3.2 China

- 6.3.3.3 Japan

- 6.3.3.4 Rest of Asia-Pacific

- 6.3.4 Rest of the World

- 6.3.4.1 Latin America

- 6.3.4.2 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Broadcom Inc.

- 7.1.2 Skyworks Solutions Inc.

- 7.1.3 Murata Manufacturing Co. Ltd

- 7.1.4 Qorvo Inc.

- 7.1.5 NXP Semiconductors NV

- 7.1.6 Texas Instruments Incorporated

- 7.1.7 Infineon Technologies AG

- 7.1.8 Qualcomm Technologies Inc.

- 7.1.9 Teradyne, Inc. (LitePoint Corporation)

- 7.1.10 RDA Microelectronics Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET