PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1237860

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1237860

Inferior Vena Cava Filter Market - Growth, Trends, And Forecasts (2023 - 2028)

The inferior vena cava filter market is anticipated to grow with a CAGR of nearly 9.1%, during the forecast period.

COVID-19 had a significant impact on the studied market as it significantly increased the incidence of pulmonary embolism among patients. Inferior vena cava (IVC) filters are often used for treating pulmonary embolism, so the rising incidence of the disease during the early pandemic also increased the usage of IVC filters. For instance, according to an article published by BMC Respiratory Research in November 2021, a study was conducted in France which showed that the overall number of patients hospitalized with pulmonary embolism increased by approximately 16% during the early pandemic. These increases were mostly attributed to COVID-19 waves, which were associated with pulmonary embolism hospitalization in COVID-19 patients. Hence, the pandemic had a significant impact on the market initially. However, as the pandemic has currently subsided, the risk of getting a pulmonary embolism has also decreased, thus the studied market is expected to have stable growth during the forecast period of the study.

Factors such as the rising prevalence of cardiac ailments and the growing demand for minimally invasive techniques are the major factors driving the market growth. Pulmonary embolism (PE) and venous thromboembolism (VTE) are the two diseases where IVC filters are used for treatment. The rising prevalence of these diseases around the world is a major factor driving the growth of the market. For instance, according to an article published by the JAMA Network in October 2022, pulmonary embolism (PE) is often characterized by occlusion of blood flow in a pulmonary artery, which happens typically due to a thrombus that travels from a vein in a lower limb. The incidence of PE is estimated to be approximately 60 to 120 per 100,000 people per year globally.

Furthermore, according to an article published by Frontiers in March 2022, Venous thromboembolism (VTE) is often associated with pulmonary embolism (PE) and deep venous thrombosis (DVT). It is estimated that there are 375,000 - 425,000 newly diagnosed patients per year in the United States that are suffering from these diseases. Hence, the rising prevalence of such diseases is expected to increase the usage of IVC filters.

Additionally, the advantages of the treatment of VTE using IVC filters are also enhancing the market growth. For instance, according to an article updated by NCBI in August 2022, various organizations around the world such as the American Heart Association (AHA) and American College of Chest Physicians (ACCP) recommend the use of inferior vena cava (IVC) filters in patients that have the venous thromboembolic disease (VTE) and having a contraindication to anticoagulant medications.

Thus, the above-mentioned factors such as the increasing prevalence of pulmonary embolism (PE) and venous thromboembolism (VTE), and the advantages of IVC filters, are expected to boost the growth of the market. However, the risks associated with device malfunction and the lack of awareness in developing countries are expected to impede market growth.

Key Market Trends

Prevention of Pulmonary Embolism is Expected to Hold a Significant Share Over the Forecast Period

Pulmonary embolism (PE) is a disease that often occurs when a blood clot gets stuck in an artery in the lung, blocking blood flow to part of the lung. Blood clots most often start in the legs and travel up through the right side of the heart and into the lungs. Inferior vena cava (IVC) filters are often used for the treatment of pulmonary embolism. Factors such as the rising prevalence of pulmonary embolism, rising geriatric populations, and the increasing demand for minimally invasive techniques are expected to boost segment growth.

The increasing prevalence of pulmonary embolism is a major factor driving the segment growth, as it leads to more usage of IVC filters. For instance, according to an article published by Lung India in November 2021, a study was conducted in India and South Korea which showed the prevalence of pulmonary embolism to be 2% and 5%, respectively. The likelihood of getting PE was significantly higher in patients who were suffering from tachycardia, tachypnea, and respiratory alkalosis.

Furthermore, according to the data published by The Department of Health and Aged Care of Australia in June 2021, it is estimated that more than 17,000 Australians every year will have a pulmonary embolism, and the incidence is increasing as the population ages. Groups at higher risk of embolism are older people, people who have cancer, and people who are immobilized (for example, hospitalized). Hence, the high prevalence of pulmonary embolism is expected to increase the usage of IVC filters, thus leading to segment growth.

Moreover, old age is often associated with pulmonary embolism cases, and the rising geriatric population thus becomes a major factor driving the growth of the market. For instance, according to an article published by MDPI in August 2022, Pulmonary embolism (PE) and deep-vein thrombosis (DVT) are the two manifestations of Venous thromboembolism (VTE), and these diseases are uncommon in children and are often considered as an old age disease.

Hence, the factors such as the rising prevalence of pulmonary embolism and the rising geriatric population are expected to boost segment growth.

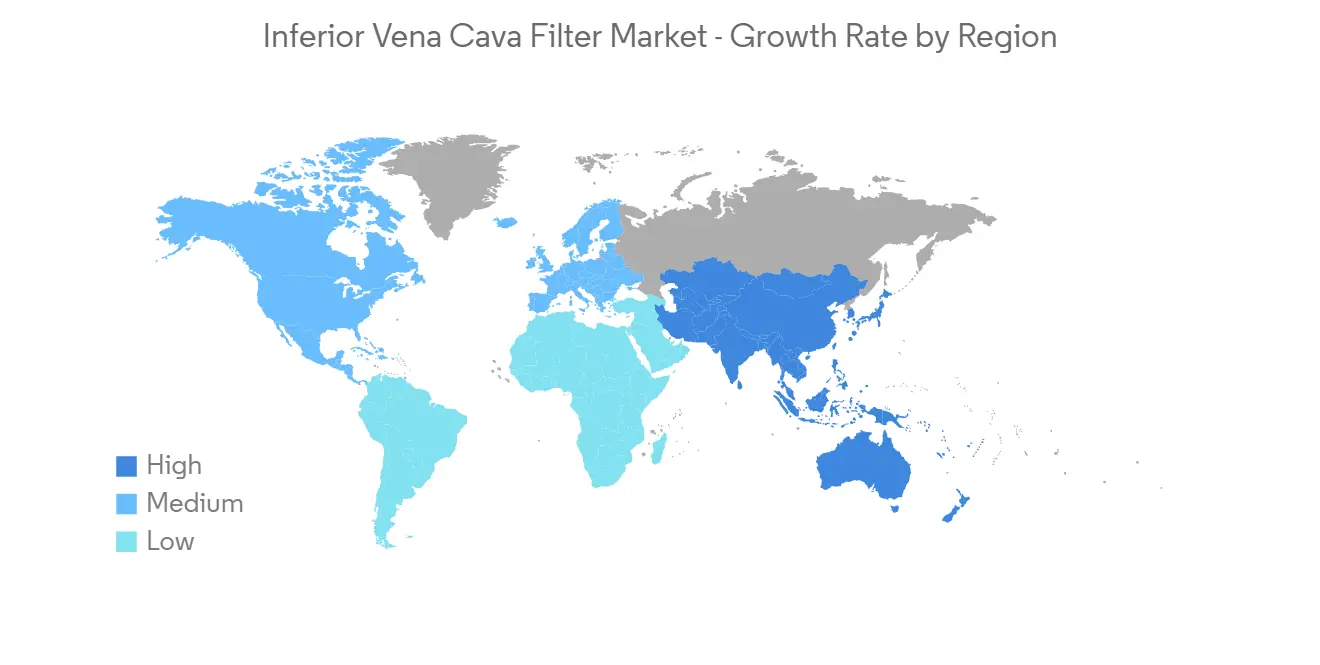

North America is Expected to Hold a Significant Share in the Market Over the Forecast Period

North America is expected to hold a significant share of the market due to the increasing usage of IVC filters for the treatment of venous thromboembolism (VTE) and pulmonary embolism (PE), the increasing prevalence of VTE and PE, and the rising geriatric population. For instance, according to the data updated by CDC in June 2022, it is estimated that as many as 900,000 people could be affected with deep vein thrombosis (DVT) or pulmonary embolism (PE) each year in the United States. Hence, the high prevalence of PE in the region is expected to boost the usage of IVC filters, leading to market growth.

Furthermore, according to an article updated by NCBI in August 2022, the incidence of pulmonary embolism (PE) ranges from 39 to 115 per 100,000 population annually, and for DVT, the incidence ranges from 53 to 162 per 100,000 people in the United States. The incidence of PE is noted to be more in males as compared to that females. Thus, the increasing incidence of such diseases is expected to boost market growth in the region.

Moreover, as VTE and PE are associated with old age, the rising geriatric population in the region is also a major factor driving the growth of the market. For instance, according to the data published by Statistics Canada in July 2022, it is estimated that around 7,330,605 people are aged 65 years or older in Canada, and this accounts for 18.8% of the total population.

Thus, due to the above mentioned factors such as the rising prevalence of VTE and PE, and the rising geriatric population, the market is expected to experience growth in the region.

Competitive Landscape

The inferior vena cava filter market is fragmented in nature and consists of a few major players. The companies have been following various strategies such as acquisitions, partnerships, investments in research activities, and new product launches to sustain themselves among the competitors in the global market. Companies like ALN, Argon Medical, B. Braun Melsungen AG, Becton, Dickinson and Company, Boston Scientific Corporation, Braile Biomedica, Cardinal Health, Cook Medical, and Volcano Corporation, among others, hold a substantial share in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Cardiac Ailments

- 4.2.2 Growing Demand of Minimally Invasive Techniques

- 4.3 Market Restraints

- 4.3.1 Risks associated with the Device Malfunction

- 4.3.2 Lack of Awareness in Developing Countries

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Application

- 5.1.1 Treatment of Venous Thromboembolism

- 5.1.2 Prevention of Pulmonary Embolism

- 5.2 By Product Type

- 5.2.1 Retrievable

- 5.2.2 Permanent

- 5.3 By End-User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Adient Medical Inc.

- 6.1.2 ALN

- 6.1.3 Argon Medical

- 6.1.4 B. Braun Melsungen AG

- 6.1.5 Becton, Dickinson and Company

- 6.1.6 Boston Scientific Corporation

- 6.1.7 Braile Biomedica

- 6.1.8 Cardinal Health

- 6.1.9 Cook Medical

- 6.1.10 Cordis

- 6.1.11 Volcano Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS