PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851889

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851889

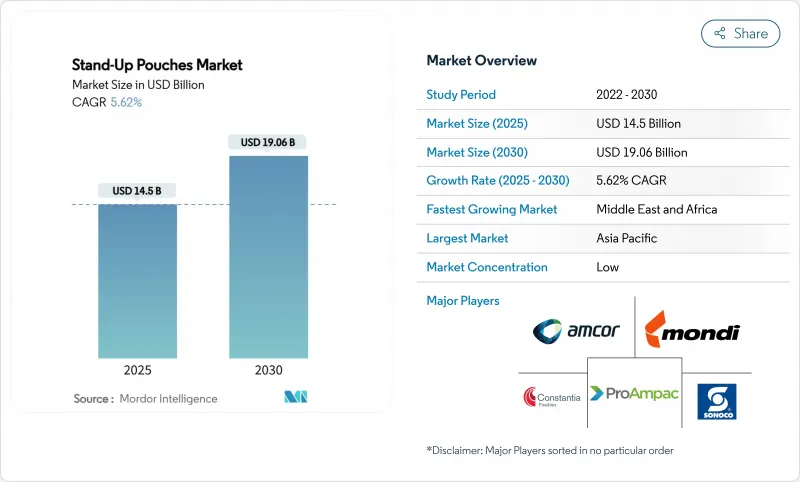

Stand-Up Pouches - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The spouted pouches market size reached USD 14.5 billion in 2024 and is forecast to expand to USD 19.06 billion by 2030, reflecting a 5.62% CAGR during 2025-2030.

Rising demand for lightweight, resealable, and visually engaging packaging underpins this growth momentum. Regulatory reforms in Europe, functional-beverage innovation in East Asia, and a rigid-to-flexible packaging shift among North American pet food brands are accelerating volume adoption. Early moves toward mono-material, recyclable formats give manufacturers cost and reputation advantages, while improvements in hot-fill and retort performance broaden end-use possibilities across food, beverage, and household categories. Production scale in Asia-Pacific, technology upgrades in Latin America, and a vibrant M&A pipeline led by Amcor, Mondi, and Sonoco are redefining competitive boundaries as companies chase efficiency and circularity.

Global Stand-Up Pouches Market Trends and Insights

Rapid Shift to Mono-Material Recyclable Pouch Structures in EU

The European Union Packaging and Packaging Waste Regulation effective February 2025 requires all consumer packs to be recyclable by 2030 and to contain 30% post-consumer recycled content for plastics. Producers are quickly moving from multi-layer aluminum structures to mono-material polyethylene films that remain compatible with curbside recycling streams. Amcor's Liquiflex AmPrima pouch meets these criteria and reports a 79% reduction in carbon emissions alongside an 84% cut in water use against legacy laminates. Brand owners adopting early see lower extended producer responsibility fees and improved shelf-appeal messaging, while late movers face R&D cost spikes and possible shelf-space loss. The pivot strengthens the spouted pouches market as converters license new sealing technologies and downgauge films without compromising barrier integrity.

On-the-Go Functional Beverage Boom in East Asia Spurring Hot-Fill Pouches

East-Asian consumers are embracing protein shakes, vitamin gels, and meal-replacement drinks in portable portions. Hot-fill tolerance beyond 85 °C allows processors to skip preservatives, extend ambient shelf life, and deliver nutrient-dense formulas. Japan's disaster-preparedness aisle now features Morinaga Seika's five-year "in Jelly Energy Long Life" pouch, validating extreme barrier and retort performance expectations. Start-ups in South Korea triple their year-over-year sales by marketing single-serve spouts for protein mixes targeting female millennials. These breakthroughs inspire adoption in Southeast-Asian convenience stores and premium gyms, giving the spouted pouches market fresh volume pipelines.

Limited Recycling Streams for Multi-Layer Laminates in United States

The U.S. requires USD 36-43 billion in infrastructure upgrades to lift plastics recycling rates to 61% by 2030. Until material recovery facilities can recognize and separate flexible laminates, brand owners hesitate to scale multilayer pouches. Producers are therefore accelerating mono-material development, but transition costs and legacy equipment risks temporarily slow the spouted pouches market.

Other drivers and restraints analyzed in the detailed report include:

- Migration from Metal Cans to Retort Pouches for Wet Pet Food in North America

- Growth of Aseptic Dairy Distribution in Africa Favoring Aluminum-Free Pouches

- Volatile EVOH & Nylon Resin Prices Squeezing APAC Converters

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic structures controlled 71.89% of the spouted pouches market in 2024 as processors valued polyethylene's sealability, polypropylene's heat stability, and PET's clarity. Biodegradable options record a 7.14% CAGR through 2030 on regulatory and consumer pull, yet still address small-run SKUs. Accredo Packaging's sugarcane-derived resin pouch offsets 43 grams of CO2 per unit while offering drop-in machinability. Meanwhile, Amcor's AmFiber paper-based barrier laminate targets snack producers searching for aluminum-free shelf life. Specialty EVOH barriers and nylon tie layers continue to protect oxygen-sensitive fillings, but cost spikes reposition them toward high-value nutraceutical lines. The spouted pouches market size for biodegradable grades is projected to cross USD 1 billion by 2028, yet plastics will still anchor core food and beverage volumes. Evolving design-for-recycle guidelines stimulate rapid experimentation, positioning plastics as both incumbent and innovation canvas in the spouted pouches market.

Round-bottom (Doyen) pouches enjoyed 38.66% revenue share in 2024, leveraging mature forming equipment and broad application adoption. Corner-bottom designs, however, climb at 5.77% CAGR due to improved base stability that supports larger fill volumes without secondary cartons. K-seal and delta-seal variants appeal to pharmaceutical fillers needing tamper-evident integrity. Foodservice buyers pursue 2-L and 5-L corner-bottom pouches for sauces and condiments, citing pallet efficiency and 79% emission savings over HDPE bottles. Nonetheless, technical challenges-chiefly head-space management during retort for SKUs exceeding 1 L-slow migration in European soup lines. Continuous R&D in gusset geometry and cap venting aims to minimize pressure differentials, promising to unlock new spouted pouches market share gains.

The Spouted Pouches Market Report is Segmented by Material Type (Plastic, Paper, and More), Product Type (Doyen/Round Bottom, K-Seal, Plow/Corner Bottom, Other Product Types), Application (Food, Beverage, Personal Care and Cosmetics, Healthcare and Pharmaceuticals, Pet Care, Other Application), Distribution Channel (Direct Sales, Indirect Sales), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated with 38.68% share of the spouted pouches market in 2024, underpinned by China's large-scale converting facilities, Japan's hot-fill R&D, and South Korea's premiumization playbook. Expected polyethylene oversupply-5 million tons of new capacity in 2025-pressures film pricing, offering converters raw-material leverage but compressing margins. Amcor's acquisition of Phoenix Flexibles in Gujarat extends reach into India's USD 20 million medical-packaging niche and accelerates localized production.

North America leverages entrenched food-processing infrastructure and pets-first culture to anchor steady demand. Infrastructure gaps loom large, with a USD 40 billion funding requirement to modernize material recovery facilities before 2030. Imminent 25% resin tariffs amplify cost pressures yet are stimulating regional resin investment and recycled resin trials. Coupled with California's 2026 recyclable-content mandate, such policies push the spouted pouches market toward mono-material PE retort formats.

Europe stands at the regulatory vanguard, compelling design-for-recycling across the spouted pouches market. Early adopters-Amcor, Mondi, and Bischof + Klein-already commercialize PP and PE single-web pouches that satisfy the 30% PCR threshold and deliver 79% CO2 cuts versus PET/Alu/OPE triplex structures. Nordic refill programmes prove that consumer uptake can be rapid when lower-carbon packaging meets online convenience.

Latin America emerges as a capacity hotspot. Brazil registers 7.2% food-industry growth, and PepsiCo's USD 240 million plant upgrade will commission three eight-lane pouch fillers in 2025. Mexico and Colombia extend tax credits for circular-packaging investments, attracting multinational converters and opening export corridors into the United States under USMCA provisions.

The Middle East and Africa experiences the fastest CAGR at 8.84%, led by aseptic milk, flavored water, and fruit nectar packed in aluminum-free pouches. SIG's Prime 55 installation in Kenya and Tetra Pak's promotional campaigns in Nigeria lower entry barriers. Energy-efficient sterilization and fitment affordability remain success factors poised to grow regional share within the spouted pouches market.

- Amcor Plc

- Mondi plc

- Sonoco Products Company

- Constantia Flexibles GmbH

- ProAmpac LLC

- Smurfit WestRock

- Swiss Pac USA

- Winpak Ltd

- Uflex Limited

- Glenroy Inc.

- Flair Flexible Packaging Corp.

- Sealed Air Corp.

- Huhtamaki Oyj

- Bischof + Klein SE

- Interflex Group

- DoyPak Solutions

- Clondalkin Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid shift to mono-material recyclable pouch structures in EU

- 4.2.2 On-the-go functional beverage boom in East Asia spurring hot-fill spouted pouches

- 4.2.3 Migration from metal cans to retort pouches for wet pet food in North America

- 4.2.4 Growth of aseptic dairy distribution in Africa favouring aluminium-free pouches

- 4.2.5 Nordic beauty e-commerce driving refill pouch SKUs with easy-pour features

- 4.2.6 CapEx surge in Brazilian pouch-filling lines accelerating rigid-to-flexible switch

- 4.3 Market Restraints

- 4.3.1 Limited recycling streams for multi-layer laminates in the U.S.

- 4.3.2 Volatile EVOH and nylon resin prices squeezing APAC converters

- 4.3.3 Brand-owner concerns over recycled-content migration

- 4.3.4 Retort head-space failures in >1-L European soup packs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Geopolitical Scenario Impact

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Plastic

- 5.1.1.1 Polyethylene Terephthalate (PET)

- 5.1.1.2 Polyethylene (PE)

- 5.1.1.3 Polypropylene (PP)

- 5.1.1.4 Ethylene Vinyl Alcohol Copolymer (EVOH)

- 5.1.1.5 Other Plastics

- 5.1.2 Paper

- 5.1.3 Metal Foil

- 5.1.4 Biodegradable and Compostable Materials

- 5.1.1 Plastic

- 5.2 By Product Type

- 5.2.1 Doyen / Round Bottom

- 5.2.2 K-Seal

- 5.2.3 Plow / Corner Bottom

- 5.2.4 Other Product Types

- 5.3 By Application

- 5.3.1 Food

- 5.3.1.1 Baked Food

- 5.3.1.2 Snacked Food

- 5.3.1.3 Pet Food

- 5.3.1.4 Confectionery

- 5.3.1.5 Other Food

- 5.3.2 Beverage

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Healthcare and Pharmaceuticals

- 5.3.5 Pet Care

- 5.3.6 Other Application

- 5.3.1 Food

- 5.4 By Distribution Channel

- 5.4.1 Direct Sales

- 5.4.2 Indirect Sales

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 United Arab Emirates

- 5.5.4.1.2 Saudi Arabia

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Egypt

- 5.5.4.2.4 Rest of Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor Plc

- 6.4.2 Mondi plc

- 6.4.3 Sonoco Products Company

- 6.4.4 Constantia Flexibles GmbH

- 6.4.5 ProAmpac LLC

- 6.4.6 Smurfit WestRock

- 6.4.7 Swiss Pac USA

- 6.4.8 Winpak Ltd

- 6.4.9 Uflex Limited

- 6.4.10 Glenroy Inc.

- 6.4.11 Flair Flexible Packaging Corp.

- 6.4.12 Sealed Air Corp.

- 6.4.13 Huhtamaki Oyj

- 6.4.14 Bischof + Klein SE

- 6.4.15 Interflex Group

- 6.4.16 DoyPak Solutions

- 6.4.17 Clondalkin Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment