PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043970

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043970

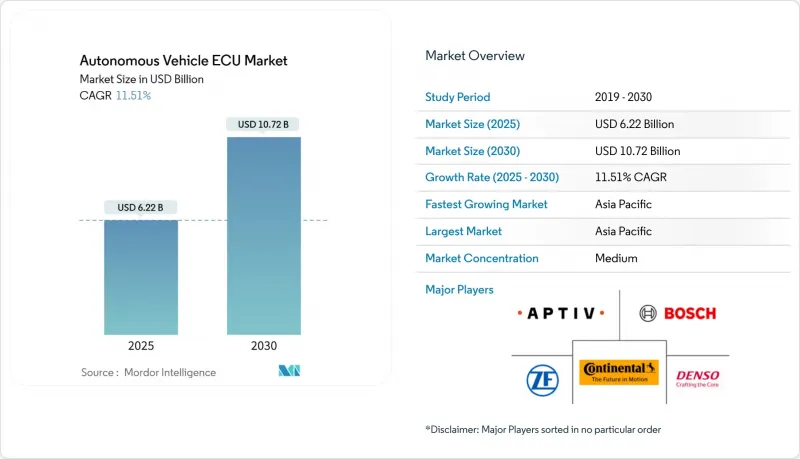

Autonomous Vehicle ECU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Autonomous Vehicle ECU market size is valued at USD 6.22 billion in 2025 and is projected to climb to USD 10.72 billion by 2030, registering an 11.51% CAGR during the forecast period.

Rapid consolidation of electronic control units into domain and zonal controllers, combined with electrification mandates and semiconductor breakthroughs, underpins this expansion. Automakers are replacing dozens of legacy ECUs with a handful of high-compute platforms that handle sensor fusion, fail-safe decision-making, and over-the-air (OTA) updates. As safety regulations tighten, centralized architectures shorten wiring harnesses, lower bill-of-materials costs, and create new software revenue streams. Semiconductor advances, especially 28 nm and wide-bandgap devices, ease thermal constraints and unlock the compute density necessary for Level 3-4 functions. Meanwhile, zoning strategies decrease complexity and enable modular vehicle upgrades, expanding addressable demand for performance-optimized controllers.

Global Autonomous Vehicle ECU Market Trends and Insights

Surge in ADAS Regulatory Safety Mandates

Governments now require automated emergency braking, lane keeping, and driver monitoring on new models, prompting immediate demand for ASIL-certified controllers. The EU General Safety Regulation applies from July 2024, while U.S. exemptions accelerate domestic testing, and UN Regulation No. 157 sets global standards for automated lane keeping. California's draft framework adds data-reporting obligations that favor centralized logging architecture. Each mandate increases compute loads for real-time fusion, redundancy, and secure diagnostics, cementing robust order books for safety-focused ECU suppliers.

Advances in Semiconductor Computing Enabling Centralized ECUs

Automotive-grade systems-on-chip integrate CPUs, GPUs, and NPUs on 28 nm nodes, doubling performance per watt over 40 nm parts. NXP's S32G family and Renesas' RH850/C1M-Ax line demonstrate hardware-accelerated routing, sensor fusion, and dual-motor control inside single packages. Silicon-carbide and gallium-nitride power devices allow compact inverter ECUs with higher switching frequencies, mitigating heat and boosting efficiency. OEMs can therefore retire 10-15 discrete modules in favor of two or three domain controllers without breaching thermal envelopes, reshaping the supplier landscape.

Thermal and Power Management Limits for High-Compute ECUs

AI-rich automotive chips push 100 W/cm2 die heat flux, challenging -40 °C to 85 °C reliability envelopes. Liquid loops and advanced interface materials add USD 200-500 per controller, pressuring cost-sensitive trims. For BEVs, controller cooling competes with battery conditioning, complicating pack-level thermal budgeting during hot-weather duty cycles.

Other drivers and restraints analyzed in the detailed report include:

- Electrification of Powertrains Boosting Domain Controllers

- Growth in Connected-Vehicle OTA Requiring Scalable Compute

- Cyber-Security and Functional-Safety Compliance Cost Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

ADAS controllers contributed 61.82% to the autonomous vehicle ECU market size in 2024, reflecting universal fitment of lane-keeping, emergency braking, and driver monitoring on mass-market models. The segment benefits from mandatory safety regulations and leverages mature 32-bit MCUs and radar-camera fusion algorithms that balance cost and performance. Suppliers focus on power-efficient SoCs and software toolchains that simplify ASIL B/C compliance.

Autonomous Driving Systems are projected to grow at a 13.21% CAGR through 2030. These platforms integrate CPUs, GPUs, and NPUs for end-to-end perception, planning, and actuation, swelling software payloads into the hundreds of gigabytes. Centralization enables OTA upgrades and cloud-based validation loops, positioning high-compute ECUs as the core enabler of Level 4 robo-taxis and hub-to-hub freight pilots.

Level 2 partial automation retained 40.38% of the autonomous vehicle ECU market share in 2024, thanks to the mass adoption of adaptive cruise and lane centering. These systems create a base of hardware-ready vehicles, accelerating the migration path to higher autonomy when regulations allow.

Level 4 stacks, however, are scaling fastest at 14.18% CAGR through 2030. Commercial pilots on fixed trucking lanes and urban robo-taxi corridors favor geo-fenced operation domains, reducing validation complexity. Controller designs emphasize redundancy, fail-degraded modes, and real-time image-lidar fusion to fulfill UN-ECE ALKS guidelines.

The Autonomous Vehicle ECU Market Report is Segmented by ECU Type (Advanced Driver Assistance Systems, and More), Level of Automation (Level 1, and More), Control Architecture (Centralized ECU, and More), Vehicle Type (Passenger Vehicles, and More), Propulsion Type (Internal Combustion Engine, and More), Distribution Channel (OEM and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific captured 41.28 % of the autonomous vehicle ECU market share in 2024 and is advancing at a 13.28% CAGR through 2030. China's smart-city pilots, South Korea's semiconductor footprint, and Japan's ADAS leadership drive bulk demand. National roadmaps fund Level 3/4 highways and mandate OTA cyber-updates, lifting controller specification baselines.

North America follows, shaped by NHTSA exemptions and California's staged permitting model that requires detailed data logging and fail-safe proof points. These frameworks elevate controller memory budgets and encryption standards, stimulating domestic semiconductor collaborations.

Europe remains pivotal as the General Safety Regulation and Regulation No. 155 hard-wire cybersecurity and functional safety into every model. Suppliers emphasize ISO 21434 compliance and redundant lane-keeping algorithms to meet NCAP 2026 scoring. Emerging regions in Latin America, the Middle East, and Africa are aligning with UN-ECE templates yet progressing more slowly due to cost sensitivity and infrastructure gaps.

- Robert Bosch GmbH

- Continental AG

- Aptiv PLC

- Denso Corporation

- ZF Friedrichshafen AG

- Valeo SA

- Magna International Inc.

- NVIDIA Corporation

- Mobileye Global Inc.

- Renesas Electronics Corporation

- NXP Semiconductors

- Texas Instruments Inc.

- Infineon Technologies AG

- Veoneer AB

- Hitachi Astemo Ltd.

- Hyundai Mobis Co., Ltd.

- Mitsubishi Electric Corporation

- Panasonic Automotive Systems

- Intel Corporation

- Autoliv Inc.

- Lear Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in ADAS Regulatory Safety Mandates

- 4.2.2 Advances in Semiconductor Computing Enabling Centralized ECUs

- 4.2.3 Electrification of Powertrains Boosting Domain Controllers

- 4.2.4 Growth in Connected-Vehicle OTA Requiring Scalable Compute

- 4.2.5 Software-Defined Vehicle Architectures Increasing Custom ECU Demand

- 4.2.6 Emergence of Zonal Controllers Reducing BOM Costs

- 4.3 Market Restraints

- 4.3.1 Thermal and Power Management Limits for High-Compute ECUs

- 4.3.2 Cyber-Security and Functional-Safety Compliance Cost Burden

- 4.3.3 Semiconductor Supply-Chain Geopolitics Causing Shortages

- 4.3.4 High Upfront R&D Investment for AI-Based Autonomous ECUs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By ECU Type

- 5.1.1 Advanced Driver Assistance Systems (ADAS)

- 5.1.2 Autonomous Driving Systems

- 5.2 By Level of Automation

- 5.2.1 Level 1 (Driver Assistance)

- 5.2.2 Level 2 (Partial Automation)

- 5.2.3 Level 3 (Conditional Automation)

- 5.2.4 Level 4 (High Automation)

- 5.2.5 Level 5 (Full Automation)

- 5.3 By Control Architecture

- 5.3.1 Centralized ECU

- 5.3.2 Distributed ECU

- 5.3.3 Hybrid ECU

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Medium and Heavy Commercial Vehicles

- 5.5 By Propulsion Type

- 5.5.1 Internal Combustion Engine

- 5.5.2 Battery Electric Vehicle (BEV)

- 5.5.3 Hybrid Electric Vehicle (HEV)

- 5.5.4 Plug-In Hybrid Electric Vehicle (PHEV)

- 5.5.5 Fuel Cell Electric Vehicle (FCEV)

- 5.6 By Distribution Channel

- 5.6.1 OEM (Original Equipment Manufacturer)

- 5.6.2 Aftermarket

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 Spain

- 5.7.3.4 Italy

- 5.7.3.5 France

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 India

- 5.7.4.2 China

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 Turkey

- 5.7.5.4 Egypt

- 5.7.5.5 South Africa

- 5.7.5.6 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 Aptiv PLC

- 6.4.4 Denso Corporation

- 6.4.5 ZF Friedrichshafen AG

- 6.4.6 Valeo SA

- 6.4.7 Magna International Inc.

- 6.4.8 NVIDIA Corporation

- 6.4.9 Mobileye Global Inc.

- 6.4.10 Renesas Electronics Corporation

- 6.4.11 NXP Semiconductors

- 6.4.12 Texas Instruments Inc.

- 6.4.13 Infineon Technologies AG

- 6.4.14 Veoneer AB

- 6.4.15 Hitachi Astemo Ltd.

- 6.4.16 Hyundai Mobis Co., Ltd.

- 6.4.17 Mitsubishi Electric Corporation

- 6.4.18 Panasonic Automotive Systems

- 6.4.19 Intel Corporation

- 6.4.20 Autoliv Inc.

- 6.4.21 Lear Corporation

7 Market Opportunities & Future Outlook