PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044003

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044003

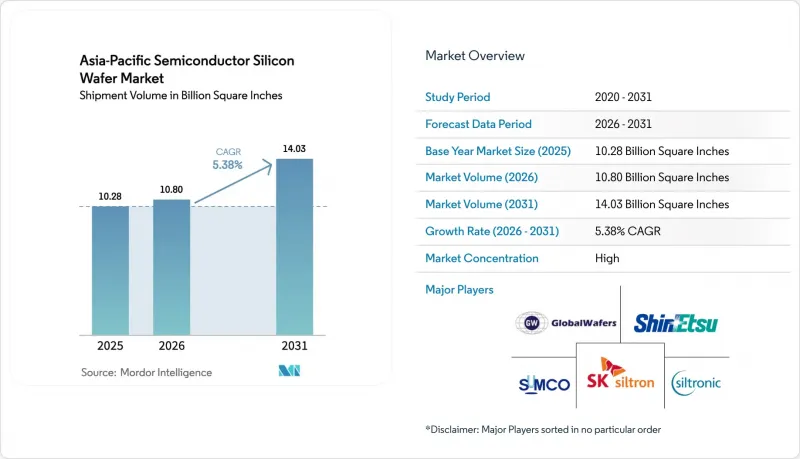

Asia-Pacific Semiconductor Silicon Wafer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Asia-Pacific Semiconductor Silicon Wafer Market size in terms of shipment volume was valued at 10.28 Billion Square Inches in 2025 and is estimated to grow from 10.80 Billion Square Inches in 2026 to reach 14.03 Billion Square Inches by 2031, at a CAGR of 5.38% during the forecast period (2026-2031).

Rising sovereign-chip programs across China, India, Japan, and South Korea are driving new fab construction, while hyperscale data centers and 5G devices keep demand for 300 mm prime-polished substrates elevated. Planned mega-clusters in Yongin, Pyeongtaek, Tainan, Gujarat, and Hokkaido have already secured multi-year wafer supply, shortening procurement cycles and tightening the merchant pool. Simultaneously, the shift toward silicon-on-insulator for radio-frequency front-end modules and the migration of power devices to silicon-carbide and gallium-nitride are reshaping the mix, freeing mature 200 mm capacity for analog and discretes. Price pressure from energy inflation remains a headwind, yet vertical integration and renewable-energy contracts are cushioning leading producers.

Asia-Pacific Semiconductor Silicon Wafer Market Trends and Insights

Soaring 5G Smartphone Penetration Boosting 300 mm Wafer Demand

A steep rise in 5G handset shipments is shifting front-end modules and application processors onto 300 mm substrates that support sub-5 nm lithography. Mainland assemblers shipped more than 280 million 5G smartphones in 2025, and India ended the same year with 180 million 5G subscribers. Foundries in Tainan, Hwaseong, and Shanghai are therefore operating at near full utilization for 4 nm and 3 nm nodes. Radio-frequency silicon-on-insulator uptake has accelerated as millimeter-wave designs mandate ultra-low loss substrates. Longer upgrade cycles for premium phones paradoxically lift total silicon content per unit, stabilizing wafer pull even when unit sales plateau.

Government Subsidies for Domestic Semiconductor Manufacturing

Fiscal incentives now dominate capital-expenditure roadmaps across the region. The Japanese cabinet earmarked JPY 2 trillion (USD 13.5 billion) for a 2 nm foundry in Hokkaido, and India's Semiconductor Mission raised its incentive pool to USD 15 billion. South Korea raised tax credits to 25% of cap-ex, encouraging an additional KRW 120 trillion (USD 91 billion) commitment in Yongin. China's third National IC Fund injected CNY 344 billion (USD 47 billion) into mature-node expansions. These subsidies lock in large wafer call-offs under long-term contracts, thereby shrinking spot-market availability and nudging prices upward despite new capacity.

Chronic Shortages of Ultrapure Polysilicon Feedstock

Polysilicon production in Xinjiang fell 18% in late 2025 following energy-rationing directives, pushing spot prices above USD 30 per kg and inflating raw-material costs by double digits for wafer producers without captive feedstock. While Tokuyama and OCI are adding 25,000 metric tons of new fluidized-bed capacity, commercial output will not arrive before 2027. Larger players such as Shin-Etsu Chemical and SUMCO protect margins through upstream integration, leaving smaller rivals saddled with 8-to-12-week lead-time extensions.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Deployment of AI Data Centers Requiring Advanced Logic Nodes

- Silicon-Carbide and GaN Transition Freeing 200 mm Capacity

- Escalating Energy Prices in East Asia Impacting Wafer-Fab Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 300 mm class accounted for 71.85% of total shipments in 2025, driven by logic and high-bandwidth memory scaling. Asia-Pacific semiconductor silicon wafer market size for 300 mm substrates is expected to expand faster than the overall baseline as gate-all-around transistors at 2 nm inflate die area and drive per-chip wafer pull. Installed base already spans 42 fabs across the region, and Shin-Etsu's Shirakawa plant alone lifted epitaxial output to 800,000 wafers per month in 2025.

Mature 200 mm lines continue to serve analog power and sensor applications, buffered by capacity freed up by silicon-carbide migration. Wafers up to 150 mm remain a sub-5% niche for gallium arsenide and indium phosphide devices. Cost-of-ownership challenges leave 450 mm pilots in a quandary, as defect densities remain thrice the threshold for break-even yields. This persistent issue highlights the significant technical and economic barriers that need to be addressed before 450 mm technology can achieve commercial viability. Consequently, this setback postpones any shake-up to the established 300 mm supply chain, which continues to dominate the semiconductor manufacturing landscape.

Logic devices accounted for 33.59% of shipments in 2025, lifted by AI, 5G basebands, and custom accelerators. Asia-Pacific semiconductor silicon wafer market share for logic is supported by record reticle counts that raise wafer consumption per chip, while heterogeneous integration adds to substrate demand. Memory followed at roughly 30%, with high-bandwidth-memory stacks driving thicker grind steps and thinner finished wafers.

Analog and discrete together absorb most of the newly liberated 200 mm supply, serving automotive powertrains and industrial automation. As lidar and time-of-flight technologies gain traction, the combined wafer pull for sensors, MEMS, and optoelectronics-each holding a high single-digit share-continues to rise. These components play a critical role in various applications, including automotive, consumer electronics, and industrial sectors, driving their steady growth. This diversification strategy helps suppliers weather the cyclical fluctuations of smartphone sales, ensuring a more stable revenue stream.

The Asia-Pacific Semiconductor Silicon Wafer Market Report is Segmented by Wafer Diameter (Up To 150 Mm, 200 Mm, 300 Mm), Semiconductor Device Type (Logic, Memory, Analog, Discrete, and More), Wafer Type (Prime Polished, Epitaxial, Silicon-On-Insulator (SOI), Specialty Silicon), End-User (PCs and Servers, Industrial, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Shipment Volume (Square Inches).

List of Companies Covered in this Report:

- Shin-Etsu Chemical Co., Ltd.

- SUMCO Corporation

- GlobalWafers Co., Ltd.

- SK Siltron Co., Ltd.

- Siltronic AG

- Wafer Works Corporation

- Okmetic Oy

- Soitec SA

- Ferrotec Holdings Corporation

- Hua Hong Semiconductor Ltd.

- ASML Holding N.V.

- LG Siltron CSS Inc.

- Poshing Technology Co., Ltd.

- Zhonghuan Semiconductor Co., Ltd.

- Mitsuboshi Diamond Industrial Co., Ltd.

- Hangzhou Silan Microelectronics Co., Ltd.

- Ningxia Xinri Hengli Silicon Materials Co., Ltd.

- Shanghai Simgui Technology Co., Ltd.

- Semiconductor Manufacturing International Corporation

- Formosa Sumco Technology Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Soaring 5G Smartphone Penetration Boosting 300 mm Wafer Demand

- 4.2.2 Government Subsidies for Domestic Semiconductor Manufacturing

- 4.2.3 Rapid Deployment of AI Data Centers Requiring Advanced Logic Nodes

- 4.2.4 Silicon Carbide and GaN Transition Freeing 200 mm Capacity

- 4.2.5 Surging Demand for Photonic Integrated Circuits in Telecom Gear

- 4.2.6 Adoption of Backside Power Delivery Networks Increasing CMP Steps

- 4.3 Market Restraints

- 4.3.1 Chronic Shortages of Ultrapure Polysilicon Feedstock

- 4.3.2 Escalating Energy Prices in East Asia Impacting Wafer Fab Costs

- 4.3.3 US Export Controls on Advanced Tools Delaying Capacity Expansions

- 4.3.4 High Defect Density in 450 mm Pilot Lines Hindering Investments

- 4.4 Industry Value-Chain Analysis

- 4.5 Technology Analysis

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Wafer Diameter

- 5.1.1 Up to 150 mm

- 5.1.2 200 mm

- 5.1.3 300 mm

- 5.2 By Semiconductor Device Type

- 5.2.1 Logic

- 5.2.2 Memory

- 5.2.3 Analog

- 5.2.4 Discrete

- 5.2.5 Other Semiconductor Device Types, Optoelectronics, Sensors, Micro

- 5.3 By Wafer Type

- 5.3.1 Prime Polished

- 5.3.2 Epitaxial

- 5.3.3 Silicon-on-Insulator, SOI

- 5.3.4 Specialty Silicon, High-Resistivity, Power, Sensor-Grade

- 5.4 By End-user

- 5.4.1 Consumer Electronics

- 5.4.2 Mobile and Smartphones

- 5.4.3 PCs and Servers

- 5.4.4 Industrial

- 5.4.5 Telecommunications

- 5.4.6 Automotive

- 5.4.7 Other End-user Applications

- 5.5 By Geography

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 South Korea

- 5.5.4 Taiwan

- 5.5.5 India

- 5.5.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Shin-Etsu Chemical Co., Ltd.

- 6.4.2 SUMCO Corporation

- 6.4.3 GlobalWafers Co., Ltd.

- 6.4.4 SK Siltron Co., Ltd.

- 6.4.5 Siltronic AG

- 6.4.6 Wafer Works Corporation

- 6.4.7 Okmetic Oy

- 6.4.8 Soitec SA

- 6.4.9 Ferrotec Holdings Corporation

- 6.4.10 Hua Hong Semiconductor Ltd.

- 6.4.11 ASML Holding N.V.

- 6.4.12 LG Siltron CSS Inc.

- 6.4.13 Poshing Technology Co., Ltd.

- 6.4.14 Zhonghuan Semiconductor Co., Ltd.

- 6.4.15 Mitsuboshi Diamond Industrial Co., Ltd.

- 6.4.16 Hangzhou Silan Microelectronics Co., Ltd.

- 6.4.17 Ningxia Xinri Hengli Silicon Materials Co., Ltd.

- 6.4.18 Shanghai Simgui Technology Co., Ltd.

- 6.4.19 Semiconductor Manufacturing International Corporation

- 6.4.20 Formosa Sumco Technology Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment