PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044060

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044060

Houston Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2032)

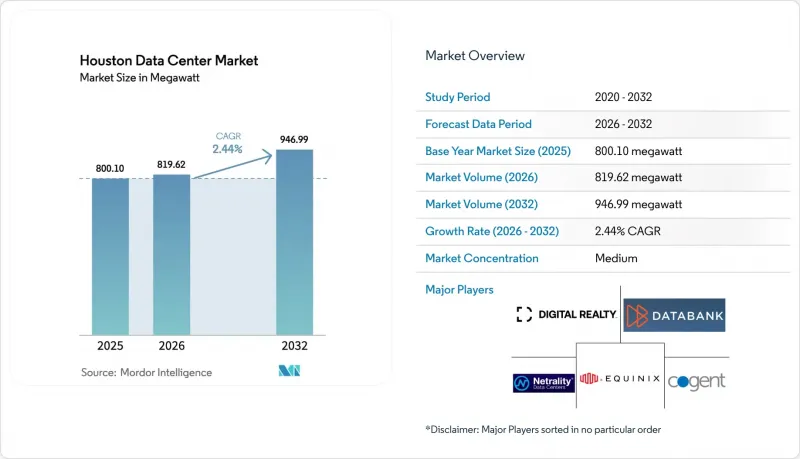

The Houston data center market size was valued at 800.10 MW in 2025 and estimated to grow from 819.62 MW in 2026 to reach 946.99 MW by 2032, at a CAGR of 2.44% during the forecast period (2026-2032).

CenterPoint Energy's interconnection queue jumped from 1 GW to 8 GW in less than one year, signaling demand that already dwarfs installed capacity and pointing to a potential 50% rise in electric load across Houston by 2031.

Mega facilities held the dominant 38.4% share of the Houston data center market in 2024, yet Massive facilities are advancing fastest at 10.2% CAGR as both hyperscale and energy-sector HPC projects consolidate into fewer, larger campuses. Market differentiation stems from the city's 3,600-plus energy organizations that require edge sites for digital-twin analytics, specialized cooling, and elevated power density, all of which separate Houston from traditional hyperscale-centric metros. Competitive intensity is heightening: hyperscale newcomers such as Google invested more than USD 1 billion statewide in 2024 alone, even as established energy-focused operators race to lock in land and power, particularly in West Houston, where land costs jumped 20-25% since 2024.

Houston Data Center Market Trends and Insights

Fast-growing Edge-Compute Demand from Oil and Gas Digital Twins

Energy operators are redesigning field architecture around real-time digital-twin analytics that require placing compute nodes close to wells, refineries, and pipelines. Texmark Chemicals' IoT deployment demonstrated that relocating analytics to the edge lets technicians pre-empt equipment failure and save tens of millions annually through optimized maintenance. ExxonMobil and Halliburton are pursuing subsea fiber and edge-HPC builds to stream sensor data back to Houston with sub-10 ms latency, reinforcing the city's role as an industrial analytics nerve center . High-density GPU clusters needed for reservoir modeling raised hardware outlays by roughly 15-20% since 2024, yet operators still prioritize these deployments because each avoided hour of downtime can exceed USD 100,000. The clustering effect of 3,600-plus energy entities allows vendors to pool edge resources, further accelerating Houston data center market growth.

Influx of Hyperscale Cloud Campuses (AWS, Google, Microsoft)

Google's USD 1 billion Texas build combined with a 375 MW solar PPA from Houston-based Engie paved the way for similar moves by Microsoft and AWS, confirming that hyperscale capital is now firmly aimed at the Houston data center market. Long equipment lead times-electrical switchgear can take up to 24 months-are forcing providers to pre-order gear, inflating cost baselines by USD 200-300 per kW. CyrusOne answered with a USD 12 billion sustainability-linked debt program earmarked for large-scale Texas sites. Hyperscale builders now pay premiums for plots that guarantee immediate power and future substation expansion, a trend expected to keep West Houston land prices climbing.

Rising Power-Grid Congestion in West Houston

ERCOT congestion charges ballooned five-fold between 2016 and 2022, reflecting transmission bottlenecks that add USD 10-15 per MWh to spot prices in West Houston CenterPoint invested USD 285 million on the Brazos Valley Connection line, but its own forecast shows a 50% load surge by 2031, indicating that line additions will trail demand. Prefabricated substation packages now cost 30% more than in 2024 due to commodity inflation, limiting rapid power roll-outs. These dynamics make power the gating factor on campus scale rather than land or fiber, constraining near-term Houston data center market growth in the west.

Other drivers and restraints analyzed in the detailed report include:

- ERCOT Renewable PPAs Unlocking Green-Powered Capacity

- Tax Incentives Under Texas JETI Act

- Hurricane and Flood-Zone Insurance Cost Premiums

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mega campuses commanded 37.95% of 2025 installed power, underscoring a pivot toward large contiguous footprints that accommodate multi-tenant hyperscale halls and energy-sector HPC cages. Massive campuses, however, surface as the volume story, advancing at 9.65% CAGR thanks to efficiencies that cut unitary OPEX by roughly 15% compared with standalone Mega builds. The Houston data center market size for Massive facilities is projected to surpass 42.3 MW by 2032, and Data Foundry's 60 MW Houston 2 campus illustrates how high-density racks (>=50 kW) coupled with 185 mph wind-rated envelopes entice petrochemical users seeking flood resilience. Land scarcity downtown pushes operators to suburban mega-sites where lower real-estate cost offsets higher transmission-upgrade spend. Medium and Small footprints serve edge hubs near refineries, but their Houston data center market share is expected to decline as digital-twin workloads consolidate into central locations that offer advanced liquid cooling.

Second-tier campuses function as testbeds for new vendors gauging Houston demand before leveling up to Massive investments. Skybox Houston I, a Large-class campus on a 20-acre private tract with 300 MVA potential, typifies the step-up model favored by energy clients anxious for bespoke security. Construction-material inflation lifted chilled-water plant costs by USD 300-400 per kW since 2024, yet operators still green-light these builds because each new 10 MW hall can absorb a single cloud anchor. Over the forecast period, Massive facilities are likely to secure the highest Houston data center market share gains as hyperscalers co-locate AI training clusters with energy-industry partners.

The Houston Data Center Market Report is Segmented by Data Center Size (Small, Medium, Large, Mega, Massive), Tier Standard (Tier I and II, Tier III, Tier IV), Absorption (Non-Utilized, Utilized), and by Hotspot. The Market Forecasts are Provided in Terms of Volume (MW).

List of Companies Covered in this Report:

- Netrality Data Centers

- Data Foundry, Inc. (Data Foundry, LLC)

- DataBank Holdings Ltd.

- Equinix Inc.

- Quasar Data Center, Ltd.

- TRG Datacenters

- Digital Realty Trust Inc.

- LOGIX Communications, L.P.

- Lumen Technologies

- Cogent Communications Holdings, Inc.

- Navisite, Inc. (Navisite LLC)

- Fibertown Data Center

- Enzu Inc.

- Crown Castle Inc.

- Serverfarm LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Study Methodology

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Fast-growing edge-compute demand from Oil and Gas digital twins

- 4.2.2 Influx of hyperscale cloud campuses (AWS, Google, Microsoft)

- 4.2.3 5G private-network roll-outs at Port Houston and airports

- 4.2.4 ERCOT renewable PPAs unlocking green-powered capacity

- 4.2.5 Tax incentives under Texas Chapter 313 replacement programs

- 4.2.6 Low-latency financial-trading corridors to Mexico and LATAM

- 4.3 Market Restraints

- 4.3.1 Rising power-grid congestion in West Houston

- 4.3.2 Hurricane and flood-zone insurance cost premiums

- 4.3.3 Talent scarcity for high-density liquid-cooling operations

- 4.3.4 Water-use restrictions during Gulf-Coast drought periods

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

5 MARKET SIZE and GROWTH FORECASTS (MW)

- 5.1 By Data Center Size

- 5.1.1 Small

- 5.1.2 Medium

- 5.1.3 Large

- 5.1.4 Mega

- 5.1.5 Massive

- 5.2 By Tier Standard

- 5.2.1 Tier I and II

- 5.2.2 Tier III

- 5.2.3 Tier IV

- 5.3 By Absorption

- 5.3.1 Non-Utilised

- 5.3.2 Utilised

- 5.3.2.1 By Colocation Type

- 5.3.2.1.1 Hyperscale

- 5.3.2.1.2 Retail

- 5.3.2.1.3 Wholesale

- 5.3.2.2 By End-User Industry

- 5.3.2.2.1 BFSI

- 5.3.2.2.2 Cloud Service Providers

- 5.3.2.2.3 E-Commerce

- 5.3.2.2.4 Government

- 5.3.2.2.5 Manufacturing

- 5.3.2.2.6 Media and Entertainment

- 5.3.2.2.7 Telecom

- 5.3.2.2.8 Other End Users

- 5.3.2.1 By Colocation Type

- 5.4 By Hotspot

- 5.4.1 Downtown CBD

- 5.4.2 West Houston (Katy)

- 5.4.3 Rest of Houston

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.2.1 Netrality Data Centers

- 6.2.2 Data Foundry, Inc. (Data Foundry, LLC)

- 6.2.3 DataBank Holdings Ltd.

- 6.2.4 Equinix Inc.

- 6.2.5 Quasar Data Center, Ltd.

- 6.2.6 TRG Datacenters

- 6.2.7 Digital Realty Trust Inc.

- 6.2.8 LOGIX Communications, L.P.

- 6.2.9 Lumen Technologies

- 6.2.10 Cogent Communications Holdings, Inc.

- 6.2.11 Navisite, Inc. (Navisite LLC)

- 6.2.12 Fibertown Data Center

- 6.2.13 Enzu Inc.

- 6.2.14 Crown Castle Inc.

- 6.2.15 Serverfarm LLC

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment