PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044251

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044251

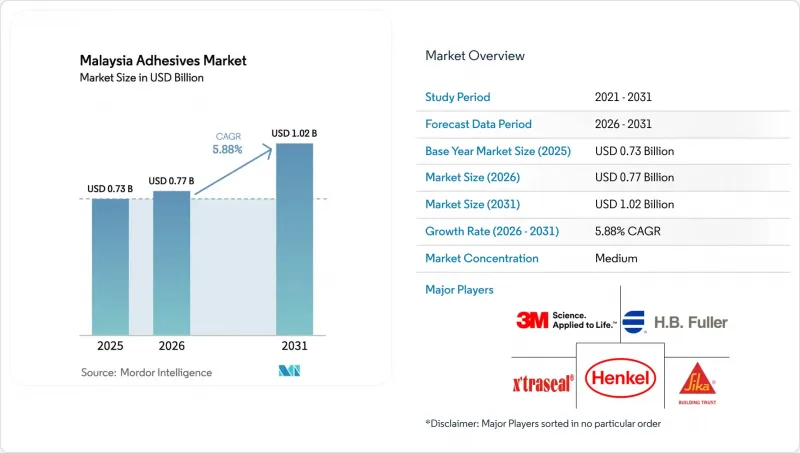

Malaysia Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Malaysia Adhesives market size is expected to grow from USD 0.73 billion in 2025 to USD 0.77 billion in 2026 and is forecast to reach USD 1.02 billion by 2031 at 5.88% CAGR over 2026-2031. Rising infrastructure spending, accelerated electric-vehicle (EV) assembly, and stringent low-VOC rules keep demand for advanced bonding technologies on an upward track. The National Construction Policy 2030 channels government tenders toward certified, BIM-specified products, a shift already pulling higher-performance, fast-curing adhesives into prefabrication lines. Penang's battery-separator hub strengthens local sourcing of specialty chemistries for cell assembly, while bonded-warehouse e-commerce hubs in Klang Valley and Johor lift volumes for carton-sealing and label adhesives. Raw-material tariffs and skilled-labor shortages remain headwinds, yet recent multinationals' investments in regional technical centers shorten lead times, deepen local formulation support, and help the Malaysia Adhesives market absorb supply shocks.

Malaysia Adhesives Market Trends and Insights

National Construction Policy 2030 Accelerates Prefabrication and Infrastructure Maintenance Demand

Malaysia's National Construction Policy 2030 mandates at least 50% digitalization of project lifecycles and compulsory BIM adoption for public works, creating detailed adhesive specifications for factory-controlled prefabrication lines. Greater traceability under QLASSIC and SHASSIC ratings rewards suppliers holding low-VOC or MyHIJAU labels. Repair and maintenance budgets, set to comprise up to 50% of future infrastructure outlays, add recurring demand for facade and bridge-repair bonding agents. The policy's balance-of-payments clause encourages local sourcing, giving domestic producers a pricing advantage over imports. Collectively, these elements add an estimated 1.2 percentage-points to long-term growth potential in the Malaysia Adhesives market.

Penang's Battery-Separator Hub Unlocks Specialty Opportunities

INV New Material's USD 750 million separator plant, operational since June 2025 at 1.3 billion m2 annual capacity, anchors Southeast Asia's largest separator supply and requires heat-resistant, electrochemically stable adhesives for pouch cell assembly. Phase-two expansion in 2027 lifts capacity to 2 billion m2, tying suppliers into a high-growth EV chain expected to support 15% of global separator demand. Multinationals such as Henkel have responded by upgrading regional labs to provide PFAS-alternative benchmarking and thermal-interface material development. Close collaboration with Universiti Sains Malaysia on joint research and development further embeds a science-driven ecosystem that will sustain 0.8 percentage-points of incremental CAGR for the Malaysia Adhesives market.

Woodworking Labor Scarcity Constrains Volumes

Furniture exporters in Muar and Gemas report order cancellations as lead times doubled to 120 days by late 2024, curbing adhesive offtake for panel lamination and edge-banding. Automation retrofits partially offset manpower gaps, yet small and medium enterprises struggle with capital costs, shaving 0.7 percentage-points from potential CAGR growth in the Malaysia Adhesives market.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Logistics Expansion Drives Packaging Adhesive Volumes

- Halal Certification Creates Premium Channels for Bio-Based Adhesives

- Aerospace Adhesive Uptake Hindered by Certification Lags

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-borne systems accounted for 43.28% of Malaysia Adhesives market share in 2025, driven by stricter indoor-air regulations and easier equipment cleanup. Investments in low-VOC vinyl-acetate-ethylene (VAE) dispersions and acrylic emulsions support continued leadership. Hot-melt lines, fueled by hygiene-product assembly and high-speed packaging, are slated to record a 6.34% CAGR to 2031, gradually raising their slice of the Malaysia Adhesives market. Formulators such as AICA Adtek and Wilron commission new extrusion capacity that can deliver stick or pillow formats optimized for automated dispensing.

Fast-tack performance, zero solvent emissions, and immediate handling strength make hot-melt chemistries attractive for EV battery-pack side-seam sealing and e-commerce carton closure. Yet capital requirements for melt tanks and temperature-controlled lines still limit adoption among smaller woodworking firms that default to water-borne PVAs. Regional subsidies for energy-efficient packaging equipment could hasten technology displacement and reshape Malaysia Adhesives market dynamics.

The Malaysia Adhesives Market Report is Segmented by Technology (Water-Borne, Solvent-Borne, Reactive, Hot Melt, and UV Cured Adhesives), Resin (Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, Silicone, and Other Resins), and End-User Industry (Building and Construction, Packaging, Automotive, Aerospace, Woodworking and Joinery, Footwear, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Aica Kogyo Co..Ltd.

- Arkema

- Avery Dennison Corporation

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Mohm Chemical SDN. BHD.

- Sika AG

- Syarikat Chemibond Enterprise Sdn Bhd

- VITAL TECHNICAL SDN BHD

- TMSB

- Dow

- Evergreen Adhesive and Chemical Sdn Bhd

- Jowat SE

- Kimberly-Clark Worldwide, Inc.

- Toyochem Specialty Chemical Sdn Bhd

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Malaysia's National Construction Policy 2030 boosts demand

- 4.2.2 Growing EV-battery assembly operations in Penang

- 4.2.3 Bonded-warehouse e-commerce boom increases packaging adhesives

- 4.2.4 Halal-certified bio-adhesives gaining export premiums

- 4.2.5 Local content rules in public housing spur wood-based panels

- 4.3 Market Restraints

- 4.3.1 Skilled-labour shortage in woodworking and furniture clusters

- 4.3.2 Slow ASTM/ISO harmonisation delays aerospace uptake

- 4.3.3 Import duties on specialty isocyanates

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Water-borne

- 5.1.2 Solvent-borne

- 5.1.3 Reactive

- 5.1.4 Hot Melt

- 5.1.5 UV Cured Adhesives

- 5.2 By Resin

- 5.2.1 Polyurethane

- 5.2.2 Epoxy

- 5.2.3 Acrylic

- 5.2.4 Cyanoacrylate

- 5.2.5 VAE/EVA

- 5.2.6 Silicone

- 5.2.7 Other Resins

- 5.3 By End-user Industry

- 5.3.1 Building and Construction

- 5.3.2 Packaging

- 5.3.3 Automotive

- 5.3.4 Aerospace

- 5.3.5 Woodworking and Joinery

- 5.3.6 Footwear

- 5.3.7 Healthcare

- 5.3.8 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Aica Kogyo Co..Ltd.

- 6.4.3 Arkema

- 6.4.4 Avery Dennison Corporation

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Mohm Chemical SDN. BHD.

- 6.4.8 Sika AG

- 6.4.9 Syarikat Chemibond Enterprise Sdn Bhd

- 6.4.10 VITAL TECHNICAL SDN BHD

- 6.4.11 TMSB

- 6.4.12 Dow

- 6.4.13 Evergreen Adhesive and Chemical Sdn Bhd

- 6.4.14 Jowat SE

- 6.4.15 Kimberly-Clark Worldwide, Inc.

- 6.4.16 Toyochem Specialty Chemical Sdn Bhd

- 6.4.17 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment