PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044254

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044254

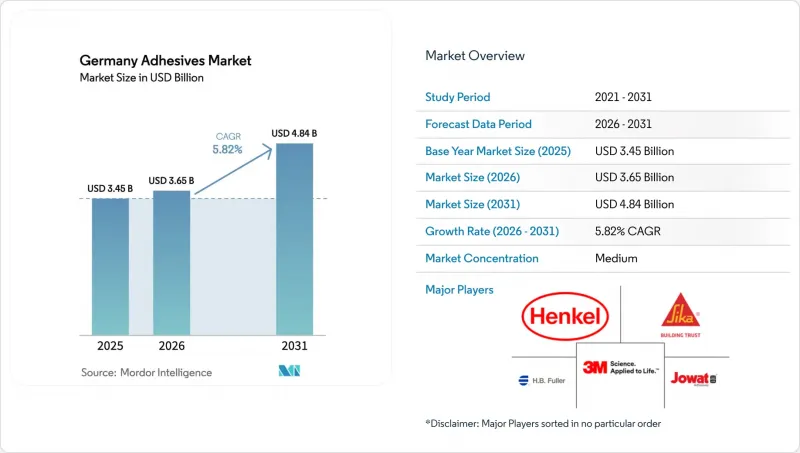

Germany Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Germany Adhesives Market size is projected to grow from USD 3.45 billion in 2025 to USD 3.65 billion in 2026, and reach USD 4.84 billion by 2031, growing at a CAGR of 5.82% from 2026 to 2031. Growth stems from renovation-led construction demand, rising electric-vehicle output, and packaging reforms that oblige converters to switch to low-VOC and debondable chemistries. Domestic formulators sharpen export focus because energy prices remain two to three times U.S. levels and cumulative regulation costs approach 13% of value-added, eroding home-market margins. Water-borne technology maintains a lead on the back of EU mid-2026 VOC caps, while hot melts gain traction as automation and bio-based initiatives accelerate. Meanwhile, global players consolidate specialty niches through large acquisitions, leaving small and medium-sized enterprises (SMEs) to defend regional pockets through customization and service intensity.

Germany Adhesives Market Trends and Insights

Construction-Sector Renovation Boom

Energy-efficiency retrofits dominate demand as pre-1990 structures require multilayer insulation, window sealing, and facade cladding to meet the federal 55% emissions-reduction target by 2030. Construction adhesives volume rose 15.4% in 2024 while wood and paper end-markets shrank, reflecting higher adhesive intensity per square meter in renovation projects. Formulations such as VINNAPAS VAE powders enable lower-clinker CEM II tile systems without sacrificing freeze-thaw durability. Project execution risk remains as skilled-labor shortages delay installations and lift costs, particularly for precision facade bonding.

Shift Toward Flexible and Recyclable Packaging

The amended Packaging Act (VerpackDG) forces 90% recyclability of plastic packs by 2029, incentivizing mono-material films and debondable adhesives to avoid extended producer responsibility penalties. Water-borne and hot-melt systems are preferred for polyethylene and polypropylene structures because they remove solvent emissions and allow mechanical recycling. Henkel's wash-off labels, launched in April 2025, preserve PET flake quality during bottle-to-bottle loops and require only six months of customer validation, accelerating market uptake.

Stringent VOC and REACH Regulations on Solvents

The EU slashed allowable VOC content to 30 g/L for interior products in 2026 and imposed workplace formaldehyde exposure limits of 0.3 ppm, forcing SMEs to spend EUR 2-5 million on reformulation and equipment upgrades. Dual inventories during the transition squeeze working capital, while water-borne chemistries still face performance gaps in aerospace and high-temperature automotive bonding.

Other drivers and restraints analyzed in the detailed report include:

- Thermal-Conductive Adhesives for EV Battery Cells

- Bio-Based Adhesives Backed by German Bioeconomy Strategy

- Specialty-Polymer Supply-Chain Disruptions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-borne systems captured 41.15% of Germany adhesives market share in 2025 on the strength of EU VOC limits that cap interior emissions at 30 g/L, steering woodworking, packaging, and construction users toward low-solvent options. Their dominance in Germany adhesives market size reflects mature production infrastructure and improved VAE copolymer performance, including less than or equal to 1 g/L VOC content and up to 50% bio input. Yet hot melts post the fastest 6.67% CAGR to 2031 as packaging lines demand instant tack, and BioRUHM's bio-reactive grades broaden application reach beyond cartons into automotive wood-metal structures.

Solvent-borne volumes continue to shrink but retain critical roles where water uptake, slow cure, or high-temperature stability preclude aqueous systems, particularly in aerospace interiors. Reactive chemistries - epoxies, polyurethanes, cyanoacrylates - anchor aerospace composites, medical devices, and electronics, commanding premium margins because of high lap-shear strength and precise cure profiles. UV-cure and hybrid reactive hot melts blend instant handling with final cross-linking, a convergence likely to redefine category boundaries and sharpen Germany adhesives market competitiveness.

The Germany Adhesives Market Report is Segmented by Technology (Water-Borne, Solvent-Borne, Reactive, Hot Melt, and UV Cured), Resin (Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, Silicone, and Other Resins), and End-User Industry (Building and Construction, Packaging, Automotive, Aerospace, Woodworking and Joinery, Footwear, Healthcare, and Other End-User Industries). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- Avery Dennison Corporation

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- Dow

- Dymax

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hexion Inc.

- ITW Performance Polymers

- Jowat SE

- Klebchemie M.G. Becker GmbH & Co. KG

- Lohmann GmbH & Co. KG

- Permabond

- Rampf Holding GmbH & Co. KG

- Sika AG

- Wacker Chemie AG

- Wevo-Chemie GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction-sector renovation boom

- 4.2.2 Shift toward flexible and recyclable packaging

- 4.2.3 Healthcare and medical-device bonding growth

- 4.2.4 Bio-based adhesives backed by German Bioeconomy Strategy

- 4.2.5 Thermal-conductive adhesives for EV battery cells

- 4.3 Market Restraints

- 4.3.1 Stringent VOC and REACH regulations on solvents

- 4.3.2 Specialty-polymer supply-chain disruptions

- 4.3.3 Skilled-labor gap in precision adhesive application

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Water-borne

- 5.1.2 Solvent-borne

- 5.1.3 Reactive

- 5.1.4 Hot Melt

- 5.1.5 UV Cured Adhesives

- 5.2 By Resin

- 5.2.1 Polyurethane

- 5.2.2 Epoxy

- 5.2.3 Acrylic

- 5.2.4 Cyanoacrylate

- 5.2.5 VAE/EVA

- 5.2.6 Silicone

- 5.2.7 Other Resins

- 5.3 By End-User Industry

- 5.3.1 Building and Construction

- 5.3.2 Packaging

- 5.3.3 Automotive

- 5.3.4 Aerospace

- 5.3.5 Woodworking and Joinery

- 5.3.6 Footwear

- 5.3.7 Healthcare

- 5.3.8 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison Corporation

- 6.4.4 DELO Industrie Klebstoffe GmbH & Co. KGaA

- 6.4.5 Dow

- 6.4.6 Dymax

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Hexion Inc.

- 6.4.10 ITW Performance Polymers

- 6.4.11 Jowat SE

- 6.4.12 Klebchemie M.G. Becker GmbH & Co. KG

- 6.4.13 Lohmann GmbH & Co. KG

- 6.4.14 Permabond

- 6.4.15 Rampf Holding GmbH & Co. KG

- 6.4.16 Sika AG

- 6.4.17 Wacker Chemie AG

- 6.4.18 Wevo-Chemie GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment