PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1329351

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1329351

Oats Market Size & Share Analysis - Growth Trends & Forecasts (2023 - 2028)

The Oats Market size is expected to grow from USD 4.39 billion in 2023 to USD 5.40 billion by 2028, at a CAGR of 4.22% during the forecast period (2023-2028).

Key Highlights

- The changing lifestyle of consumers, including the decision to opt for light and healthy meals, is driving the demand for oats. The high nutritive content of oats is the major driver of the market. Additionally, an increase in preference for healthy meals and demand for convenience food is also driving the oats market. Also, its added functional properties enhance its usage by consumers, and it is witnessed to be consumed majorly as a breakfast food.

- Moreover, the working population's fast-paced lifestyle has catalyzed the demand for oats as breakfast cereals. Oats are gaining popularity as an alternative to sugar or fat that can retain moisture, enhance fiber, and stabilize food texture. The growing trend for low-calorie, low-fat, and less-sugar food products among consumers is increasing the demand for oats as a fat or sugar replacer ingredient.

- The rising health concerns, rapidly changing lifestyle, and change in consumption pattern is increasing consumers' demand for low-fat or low-calorie food to maintain a healthy lifestyle and reduce the risk of various health problems such as obesity, cardiovascular diseases, cancer, and others.

- The increasing gut problems coupled with the rise in demand for preventative healthcare products in countries such as China, India, and Japan are expected to result in increased demand for prebiotics products. Many people suffer from digestive problems such as pain, cramps, constipation, and bloating.

- Moreover, certain conditions, such as gastroesophageal reflux disease (GERD), irritable bowel syndrome (IBS), and diverticulitis, have been growing in recent years. This rising prevalence of digestive diseases has generated the demand for fiber or prebiotic-rich food and beverage products.

- According to the UN Department of Economic & Social Affairs (UN DESA), the share of older persons in the global population is expected to increase from 9.3 percent in 2020 to 16.3% in 2050. Thus, the increasing geriatric population worldwide has also increased the demand for healthy food.

Oats Market Trends

Surging Demand for Dietary Fiber Ingredients

- Oats are dietary fiber beneficial for a healthy gut microbiome. Higher intake of dietary fiber is linked with positive effects on health and decreased incidence of several diseases such as cardiovascular disease, colorectal cancer, and other diseases.

- Consumers are seeking positive nutrition, and thus the increasing interest of consumers in food and beverage products that are perceived to be healthier is boosting the demand for dietary fiber ingredients as it offers various health benefits such as maintaining bowel health, lowering cholesterol levels, controlling blood sugar level, aids in achieving a healthy weight, and others.

- Dietary fiber ingredients are gaining attention from consumers as they are perceived as healthful, and thus demand for fiber-rich food products is increasing. For instance, in 2021, according to the International Food Information Council (IFIC), the food and health survey showed that 56% of consumers are actively trying to consume fiber.

- Furthermore, the increasing importance of nutraceuticals, on account of rising health awareness, consumer shift toward natural ingredients, and regulatory support intended to promote the inclusion of functional ingredients are expected to fuel the demand for oats as a functional ingredient in many food products like bakery products.

- Hence, the growing demand for functional food and healthy food ingredients among manufacturers, along with the growing demand for food products with high fiber content owing to their health benefits, is fuelling the demand for dietary fiber ingredients such as oats in the market.

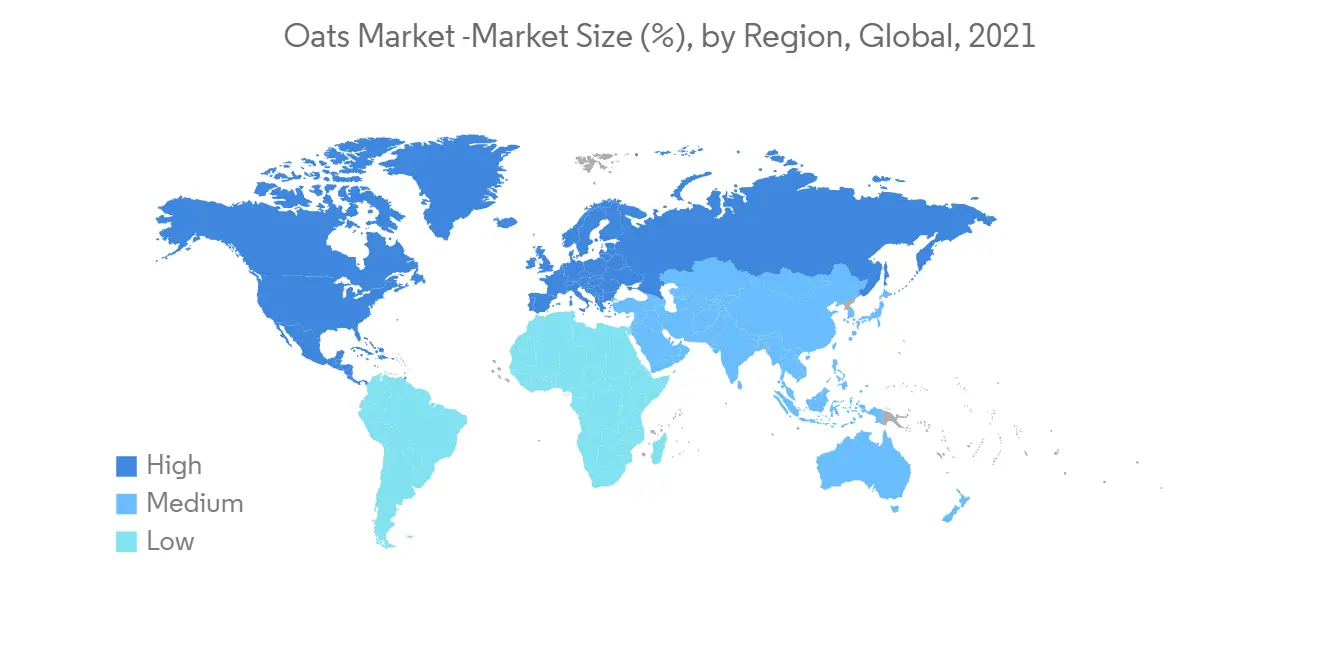

North America Holds the Major Market Share

- North America accounts for the major market share, followed by Europe. According to the Organization for Economic Co-Operation and Development (OECD) analysis, the percentage of health expenditure spent on overweight and related conditions is predicted to account for 14% in the United States from 2020 to 2050.

- An increase in demand for convenience food coupled with rising obesity and diabetes cases in the region has increased demand for healthier breakfast options such as oats. Moreover, oatmeal being one of the most prominent weight-loss food, gains an edge over other breakfast cereal products.

- Additionally, the rich fiber content in oats, known as beta-glucans, helps lower blood sugar levels and thus makes an excellent choice among diabetic patients. In 2021, North America remained the second most diabetes-prevalent region in the world.

- According to International Foundation for Gastrointestinal Disorders, around 5-10% of the population globally suffer from irritable bowel syndrome (IBS), and 25 and 45 million people are affected by IBS in the United States. Oat is a type of prebiotic that helps nourish gut microbes. Prebiotic products are gaining popularity among consumers globally owing to growing awareness about improved gut health.

- The increasing consumption of prebiotics owing to the rising awareness regarding the health benefits of prebiotics, including improved digestion, lower stress response, better hormonal balance, and a decrease in cardiovascular diseases among consumers, is driving the market's growth.

- Thus, consumers are prioritizing their gut health and have thus been opting for products like dietary supplements, nuts and seeds, whole grains, and other food and beverage products that are rich in prebiotics. Thus, manufacturers are gaining interest in functional ingredients like oats that offer the benefits of prebiotics, such as ease of constipation, helps absorb calcium and mineral, and nourish gut microbes, to manufacture functional health supplements, food and beverages products, and others.

Oats Industry Overview

The global market for oats is competitive, owing to the presence of large regional and domestic players in different countries, where domestic companies have gained preference over multinationals due to their strong market power. Emphasis is given to the merger, expansion, acquisition, and partnership of the companies, along with new product development as strategic approaches adopted by the leading companies to boost their brand presence among consumers. The global leaders in the oats market include PepsiCo, Inc., The Kelloggs Company, B&G Foods, Nestle SA, General Mills, and others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Product type

- 5.1.1 Whole Oats

- 5.1.2 Oat Groats

- 5.1.3 Steel-Cut Oats

- 5.1.4 Rolled Oats

- 5.1.5 Flour

- 5.2 Distribution Channel

- 5.2.1 Supermarket/Hypermarket

- 5.2.2 Convenience Stores/Grocery Stores

- 5.2.3 Online Retail Stores

- 5.2.4 Other Distribution Channels

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Spain

- 5.3.2.2 United Kingdom

- 5.3.2.3 Germany

- 5.3.2.4 France

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 PepsiCo, Inc.

- 6.3.2 Nestle SA

- 6.3.3 B&G Foods, Inc.

- 6.3.4 Marico Limited

- 6.3.5 Nature's Path Foods

- 6.3.6 The Kellogg Company

- 6.3.7 Bob's Red Mill Natural Foods

- 6.3.8 General Mills

- 6.3.9 Post Holdings

- 6.3.10 The Raw Factory

7 MARKET OPPORTUNITIES AND FUTURE TRENDS