PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1432945

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1432945

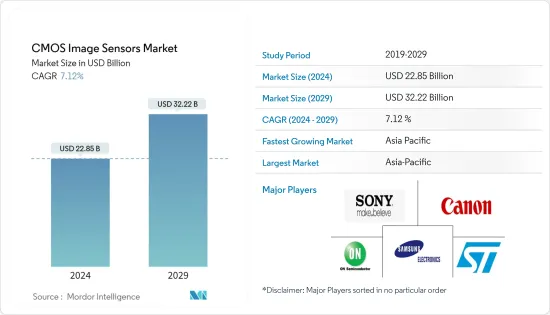

CMOS Image Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The CMOS Image Sensors Market size is estimated at USD 22.85 billion in 2024, and is expected to reach USD 32.22 billion by 2029, growing at a CAGR of 7.12% during the forecast period (2024-2029).

Key Highlights

- The rising demand for high-definition image-capturing devices in various industries has spurred a significant adoption of CMOS (Complementary Metal-Oxide-Semiconductor) technology. This technology not only provides faster shutter speeds but also ensures high-quality images.

- Primarily driven by the increasing demand for smartphones, the global CMOS image sensors market has seen substantial growth. The widespread use of cameras with image sensors in smartphones has particularly benefited the consumer electronics industry. Smartphone producers are responding to the surge in popularity of cell phone photography by incorporating up to five cameras into a single device. These CMOS image sensors are omnipresent, found not only in smartphones but also in laptops and digital single-lens reflex (DSLR) cameras.

- Integration of cameras into smartphones has significantly augmented image capturing, aligning with the expanding smartphone penetration rate. These factors are poised to propel the image sensor market forward.

- Simultaneously, the demand for producing top-quality images in smartphone cameras and for CMOS technology is exponentially increasing due to innovations. Moreover, the adoption of machine vision systems and the emergence of self-driving cars and advanced driver assistance systems (ADAS) further drive the demand for CMOS sensors.

- Despite the prevalence of CCD (Charge-Coupled Device) sensors in many industrial applications due to their maturity and higher quality, the demand for CMOS sensors persists. CCD sensors excel in high-quality, high-resolution images and excellent light sensitivity, providing competition to CMOS sensors. This competition is expected to limit the market's growth.

- The electronics and semiconductor industries faced significant setbacks during the COVID-19 pandemic due to closures and disruptions in the global supply chain. Despite this, the anticipated growth of the global CMOS image sensors market remains strong, driven by increased demand from the consumer electronics and automotive sectors.

CMOS Image Sensors Market Trends

Automotive and Transportation Industry to be the Fastest Growing End User

- The demand for CMOS image sensors in the automotive and transportation sectors is rapidly expanding due to the increasing adoption of advanced driver-assistance systems (ADAS) across various categories of vehicles. The integration of high-performance protective functions into automotive systems has influenced the widespread adoption of camera sensor systems, particularly in the context of upcoming driverless autonomous vehicles worldwide. The ongoing development of autonomous and connected vehicles is paving the way for new market opportunities.

- For instance, the Federal Transit Administration (FTA) recently announced a substantial opportunity for demonstration projects, offering up to USD 6.5 million, including USD 5 million for ADAS in Transit Buses and an additional USD 1.5 million for the initial phase of Automated Transit Bus Maintenance and Yard Operations. Additionally, in April 2023, the UK announced the approval of hands-free driving technology through Ford's advanced driver-assistance system (ADAS), BlueCruise, set to lead the way on the country's motorways.

- Moreover, electric vehicles have emerged as a pivotal technology for decarbonizing road transport, given that this sector contributes over 15% of global energy-related emissions, as per IEA data. Recent years have witnessed exponential growth in EV sales, with advancements in range, broader model availability, and enhanced performance. Passenger electric cars are gaining traction, and the IEA estimates that 18% of new cars sold in 2023 will be electric, with Europe, China, and the US leading the electric vehicle markets.

- The National Safety Council projects that by 2026, approximately 71% of registered vehicles will feature rear cameras, while 60% will be equipped with rear parking sensors. This widespread adoption of ADAS is expected to fuel the market's growth significantly.

- According to the World Economic Forum, an estimated 12 million fully autonomous cars are projected to be sold annually by 2035, encompassing 25% of the global automotive market. This surge in demand for connected and electric vehicles has spurred innovation and product development in the CMOS image sensor market. Key market vendors are concentrating on product innovation to meet the escalating consumer demand.

Americas is Expected to Witness Significant Growth

- The growing adoption of CMOS image sensors across the United States is due to the strong presence of the consumer electronics market, which is fueling the usage of mobile camera modules and other portable devices at a high rate. In consumer electronics, the smartphone has become the primary camera device, dominating cameras and DSLRs. Heavy competition in the smartphone segment has driven manufacturers to provide better cameras to have the edge over the competition, resulting in high investments in technology innovations in this field.

- The US Census Bureau estimated the smartphone sales value at USD 74.7 Billion in 2022-2023. This sluggish growth is an outcome of declined shipments of smartphones in the US. Low-end smartphone sale declines were the biggest contributing factor to the downturn amid economic challenges, high inflation, and poor seasonal demand; however, this is expected to end in the upcoming years. These sales trends are expected to have a significant impact on the growth of CMOS image sensors in the consumer electronics segment, which not only includes smartphones but also PCs, laptops, and tablets.

- In addition to this, robotic cameras have become a revolutionary force in various industries, transforming the way of capturing, monitoring, and interacting with surroundings. These sophisticated devices, equipped with cutting-edge technology, offer a plethora of advantages, making them invaluable assets in applications ranging from surveillance and security to manufacturing and entertainment. Thus, CMOS sensors are more efficient in generating a digital image and consume less power than a CCD. They can be larger than a CCD, enabling high-resolution images, and their manufacture is more economical when compared to a CCD, thus driving the demand in the regional market.

- With the increase in the use of image sensor devices in biometrics, medical, and film cameras by vehicle driver assistance systems, security, and surveillance devices are expected to have a substantial market in the future. Moreover, drones are widely used in countries such as the United States to conduct surveys, and manufacturers are constantly looking for cameras that can capture images from altitude. Cameras with high megapixel resolution and small sensor sizes can be subject to image diffraction effects.

- This is impacting the demand for CMOS image sensors as they are increasingly being used in automotive applications. For instance, according to OICA, in 2022, Mexico was the leading motor vehicle manufacturer in the Latin American region, with 3,509.8 thousand vehicles, followed by Brazil (2,369.77), Argentina (536.9), and Colombia (51.46).

CMOS Image Sensors Industry Overview

The CMOS image sensor market exhibits high fragmentation, with major players such as STMicroelectronics NV, Sony Group Corporation, Samsung Electronics Co. Ltd, ON Semiconductor Corporation, and Canon Inc. These entities are leveraging strategies like partnerships and acquisitions to enrich their product portfolios and establish enduring competitive edges.

In September 2023, Sony Semiconductor Solutions Corporation unveiled the IMX735, a cutting-edge CMOS image sensor designed for automotive cameras, boasting an industry-leading pixel count of 17.42 effective megapixels. This innovative product is poised to bolster the development of automotive camera systems capable of sophisticated sensing and recognition, contributing significantly to the advancement of safe and secure automated driving.

Additionally, in January 2023, Samsung Electronics introduced its latest 200-megapixel (MP) image sensor, the ISOCELL HP2. This sensor incorporates enhanced pixel technology and increased full-well capacity, delivering stunning mobile images for premium smartphones. Packed with 200 million 0.6-micrometer (μm) pixels within a 1/1.3" optical format, a sensor size widely used in 108MP primary smartphone cameras, the ISOCELL HP2 enables consumers to experience even higher resolutions in the latest high-end smartphones without larger camera protrusions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Implementation of CMOS Image Sensors in the Consumer Electronics Segment

- 5.1.2 Emergence of 4K Pixel Technology in the Security and Surveillance Sector

- 5.2 Market Restraints

- 5.2.1 Competition from CCD Sensor

6 TECHNOLOGY SNAPSHOT

- 6.1 By Communication Type

- 6.1.1 Wired

- 6.1.2 Wireless

7 MARKET SEGMENTATION

- 7.1 By End-user Industry

- 7.1.1 Consumer Electronics

- 7.1.2 Healthcare

- 7.1.3 Industrial

- 7.1.4 Security and Surveillance

- 7.1.5 Automotive and Transportation

- 7.1.6 Aerospace and Defense

- 7.1.7 Computing

- 7.2 By Geography

- 7.2.1 North America

- 7.2.2 Europe

- 7.2.3 Asia-Pacific

- 7.2.4 Latin America

- 7.2.5 Middle East and Africa

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 STMicroelectronics NV

- 8.1.2 Sony Corporation

- 8.1.3 Samsung Electronics Co. Ltd

- 8.1.4 ON Semiconductor Corporation

- 8.1.5 Canon Inc.

- 8.1.6 SK Hynix Inc.

- 8.1.7 Omnivision Technologies Inc.

- 8.1.8 Hamamatsu Photonics KK

- 8.1.9 Panasonic Corporation

- 8.1.10 Teledyne Technologies Inc.

- 8.1.11 GalaxyCore Shanghai Limited Corporation

- 8.2 Vendor Market Share Analysis

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE TRENDS