PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1403748

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1403748

Sugar Substitutes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

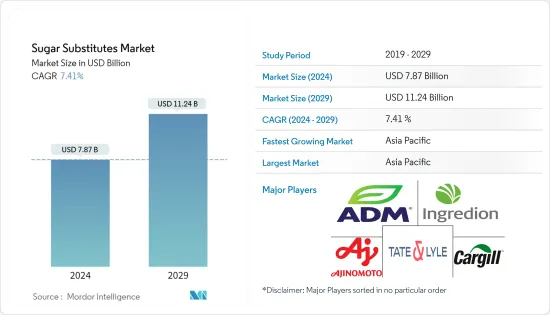

The Sugar Substitutes Market size is estimated at USD 7.87 billion in 2024, and is expected to reach USD 11.24 billion by 2029, growing at a CAGR of 7.41% during the forecast period (2024-2029).

Key Highlights

- The increasing health consciousness among consumers in the country, coupled with the high demand for ready-to-eat food and beverages and increased spending on food, are driving the growth of the market studied. Also, in recent years, there has been a significant rise in the demand for healthy alternatives to refined sugar.

- For instance, in 2022, according to the International Food Information Council (IFIC), 31% of Gen Z, 30% of millennials, and 23% of Gen X consumers are inclined towards no/low-calorie sweeteners. This can be attributed to increasing awareness among individuals about the negative health impact of sugar.

- Consistently consuming excess sugar can lead to tooth decay and cavities, obesity, type 2 diabetes, heart disease, high blood pressure, and many other detrimental health conditions. It can even contribute to nutrient deficiencies due to providing calories but limiting nutrients. In other words, added sugars are empty calories offering little to no nutritional benefit. Therefore, consumers are seeking healthy sugar substitutes, such as stevia, aspartame, sorbitol, maltitol, neotame, acesulfame, and D-tagatose, as they are low in calories.

- Prominent manufacturers in the market are certifying their product offerings by renowned organizations to gain consumer trust and confidence. They are also focusing on innovating and introducing high-intensity sweeteners.

- For instance, in 2022, Sweegen expanded its extensive sweetener portfolio with the zero-calorie, high-intensity sweetener Brazzein. The product was developed in collaboration with long-term innovation partner Conagen, which has scaled it to commercial production. Such innovations will likely positively influence the demand for sugar substitutes during the study period.

Sugar Substitutes Market Trends

Health Consciousness Among Individuals Drives the Market

- Excess sugar intake can lead to several health problems, including tooth decay, obesity, diabetes, heart disease, and high blood pressure. Therefore, the increasing awareness of these adverse health impacts and the rising health consciousness encourage individuals to limit their intake of added sugars. According to a survey by the International Food Information Council (IFIC), 61 percent of United States adults were reportedly trying to limit sugars in their diet in 2023.

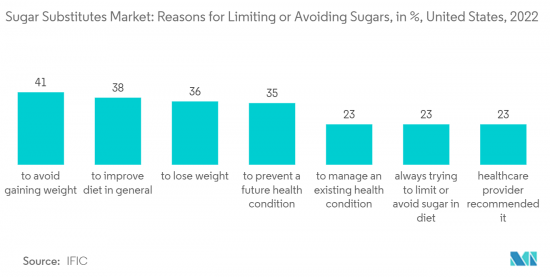

- Another study conducted in 2022 to understand the reasons behind limiting or avoiding sugars reveals that avoiding gaining weight was the most frequently mentioned explanation amongst approximately 41 percent of respondents. About 38 percent of respondents said they limit their sugar intake to improve their diet, 36 percent to lose weight, 35 percent to prevent a future health condition, and 23 percent to manage an existing health condition.

- As diabetes and obesity become more prevalent, consumers strive to live a healthier lifestyle. They are looking for natural sweeteners with zero calories to keep their blood glucose levels in check. Therefore, it is expected that the demand for stevia will grow as it is aligned with the requirements of the consumers.

- Moreover, health-conscious consumers are avoiding highly refined foods and beverages with added sugars and sweeteners and opting for low-sugar products as they are perceived to be a healthy food option. The statistics by IFIC show that nearly 37 percent of respondents in the United States said that the term "low in sugar" best defines healthy food to them. Therefore, food and beverage manufacturers are shifting to sugar substitutes as they don't contain calories or sugar.

Asia-Pacific Holds a Major Market Share

- Asia-Pacific currently accounts for the majority of the share of the global sugar substitute market. The primary factors behind this significant growth include the expanding population, the increasing number of health-conscious individuals, and the rising prevalence of chronic medical conditions.

- The rising trend of natural and organic products has boosted the demand for natural sweeteners in the region. Furthermore, sugar substitutes, such as monk fruit sweetener, stevia, and yacon syrup, are comparatively sustainable and have gained immense popularity in the region. Moreover, increased consumer awareness about the adverse health impact of white sugar, along with changing dietary patterns, is driving the market. Also, major players are indulging in partnerships and acquisitions to launch innovative and sustainable products.

- For instance, in January 2021, Tate & Lyle and Codexis expanded their collaboration to improve the production of two of its newest sweeteners, Dolcia Prima Allulose and Tasteva M Stevia Sweetener. Besides this, regulatory bodies in several countries authorized the use of sugar substitutes in consumer products. This, in turn, drives the demand for alternative sweeteners among food and beverage companies to introduce low-caloric products to capitalize on customers' needs and drive their overall sales.

Sugar Substitutes Industry Overview

The global market for sugar substitutes is highly competitive, with the presence of prominent regional and domestic players in different countries. Emphasis is given to mergers, expansions, acquisitions, and partnerships as key strategies for building a solid consumer base. Along with this, the leading companies are also focusing on product developments to boost their brand presence among consumers.

Some major players in the market include Cargill Incorporated, Tate & Lyle PLC, Ajinomoto Co., Inc., Ingredion Incorporated, and ADM. The prime factors determining the market players' position in the concerned market are the continuous launch of new products with advanced technology and high quality. Thus, brands differentiate their products in sweetness, quality, and innovation to gain a competitive advantage.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Consumer Inclination Toward Clean-label Sugar Substitute

- 4.1.2 Demand For Sugar Substitutes From Diabetic and Obese Population

- 4.2 Market Restraints

- 4.2.1 Availability of Low-cost Sweeteners

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Acesulfame Potassium

- 5.1.2 Advantame

- 5.1.3 Aspartame

- 5.1.4 Neotame

- 5.1.5 Saccharin

- 5.1.6 Sucralose

- 5.1.7 Stevia

- 5.1.8 Other Types

- 5.2 Application

- 5.2.1 Food

- 5.2.1.1 Baked Foods and Cereals

- 5.2.1.2 Confectionery

- 5.2.1.3 Dairy and Dairy Alternatives

- 5.2.1.4 Sauces, Condiments, and Dressings

- 5.2.1.5 Othe r Food Applications

- 5.2.2 Beverage

- 5.2.3 Pharmaceuticals

- 5.2.1 Food

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Spain

- 5.3.2.2 United Kingdom

- 5.3.2.3 Germany

- 5.3.2.4 France

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Active Companies

- 6.2 Most Adopted Strategies

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Tate & Lyle PLC

- 6.4.2 Ingredion Inc.

- 6.4.3 Ajinomoto Co., Inc

- 6.4.4 Cargill Inc

- 6.4.5 Morita Kagaku Kogyo Co. Ltd

- 6.4.6 JK Sucralose Inc.

- 6.4.7 Manus Bio Inc.

- 6.4.8 Archer Daniels Midland Company

- 6.4.9 Xianghua GL Stevia Co

- 6.4.10 GLG Life Tech Corp.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS