PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444184

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444184

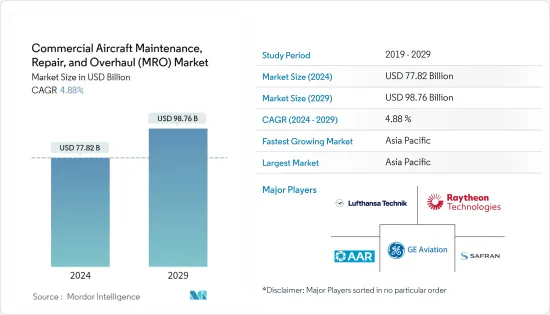

Commercial Aircraft Maintenance, Repair, and Overhaul (MRO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Commercial Aircraft Maintenance, Repair, and Overhaul Market size is estimated at USD 77.82 billion in 2024, and is expected to reach USD 98.76 billion by 2029, growing at a CAGR of 4.88% during the forecast period (2024-2029).

The ongoing COVID-19 pandemic resulted in a full-scale crisis, with the imposition of travel restrictions and suspension of flights in a global effort to contain the spread of the virus. Due to decreased passenger traffic and limited aircraft movements, the market for maintenance, repair, and overhaul was affected significantly in 2020. Nevertheless, as travel restrictions decreased in 2021 and as aircraft movements are gradually increased, the demand for aircraft maintenance is expected to witness positive growth in the coming years.

Airlines are inclined toward maintaining the optimum health of their fleet and procuring new aircraft only as a last resort, owing to the high investment required for it. With COVID-19 severely hampering the revenue sources and eroding the profit margins of airlines, more airlines are expected to resort to MRO to maintain fleet efficiency. Furthermore, several government initiatives were formulated to encourage airports to support MRO as a strategic activity. The governments are now undertaking various holistic approaches to ensure that adequate space is allocated at different airports within the country for MRO, which may enhance commercial aircraft MRO activities during the forecast period.

However, the advent of predictive maintenance flooded the MRO industry with a flurry of problems, both technological and manpower-related. As the concept of predictive maintenance powered by innovative technologies, such as digital twins, is still in its infancy, rapid improvements and growth are visualized within a short period. This implies that not all firms are equipped with the required infrastructure to harness the true potential of machine learning and other advanced emerging concepts. This also indicates the limited reach of the concept, as a few MRO organizations are keen on investing in capital to develop these skills among their personnel. However, the domain is not well-represented in industry-focused education and training curricula. Moreover, there is limited cooperation between MROs and OEMs about the repair standards for new equipment and components, making the MRO process highly complex and demanding. Such disruptive threats may endanger the growth of the market in focus during the forecast period.

Aerospace MRO Market Trends

The Engine MRO Segment is Likely to Dominate the Market During the Forecast Period

Engine MRO includes field maintenance and depot maintenance checks. Depot-level maintenance entails material maintenance, major repair, overhaul, or complete rebuilding of engines, parts, end items, assemblies, and subassemblies. It also includes the manufacturing of parts, technical assistance, and testing. Field-level maintenance comprises shop-type work and on-equipment maintenance activities at levels different than depot maintenance. Intermediate or shop-type work includes limited repair of commodity-oriented assemblies and end-items, job shop, bay, and production line operations as per requirement, software maintenance, and repair of subassemblies, such as fabrication or the manufacturing of repair parts, assemblies, and components. OEMs control approximately half of the market in the engine maintenance sector, with the other half roughly split between independent and airline overhaul shops. For new powerplant generations specifically, operators frequently outsource engine maintenance and use full MRO-support programs. For instance, in December 2021, the low-cost airline of Saudi Arabia, flynas, finalized a multi-year Rate Per Flight Hour (RPFH) agreement with CFM International for the LEAP-1A engines powering the airline's fleet of 80 Airbus A320neo aircraft. The RPFH agreement is a part of CFM's portfolio of flexible aftermarket support offerings. Throughout the term of the agreement, CFM will guarantee maintenance costs for the airline's 160 LEAP-1A engines on per engine flight hour basis. Such developments are anticipated to drive the engine MRO segment of the market during the forecast period.

Asia-Pacific is Expected to Witness the Highest Growth During the Forecast Period

The commercial aviation industry in the Asia-Pacific region is expected to grow rapidly over the next decade, in the wake of the strong demand for new narrow-body aircraft, which will enhance the need for MRO operations. The Asia-Pacific region currently operates 1/3rd of the global commercial aircraft fleet, and the fleet in the region is expected to reach over 13,000 aircraft by 2031, with China's airline fleet accounting for over 45% of the region's total. According to industry experts, with the extension of lease contracts of airlines, the average age of the aircraft fleet in the Asia-Pacific region increased to 18 to 24 years. Earlier, in pre-COVID-19 years, the average age of the fleet was 6 to 12 years. With a large fleet and growing potential for the aviation industry in the region, many major MRO players are rapidly enhancing their presence in the market. For instance, in 2020, Pratt & Whitney expanded its global Pratt & Whitney GTF engine maintenance network with two new MRO providers in China. Aircraft Maintenance and Engineering Corporation (Ameco) (a joint venture of Air China Limited and Lufthansa Airlines) and MTU Maintenance Zhuhai Co. Ltd (a joint venture of MTU Aero Engines and China Southern Airline Company Limited) became new facilities as part of the GTF MRO network to provide engine maintenance for PW1100G-JM engines for the Airbus A320neo family of aircraft. Moreover, low-cost labor markets, such as Vietnam and Thailand, are becoming increasingly attractive to OEMs and MROs for setting up new facilities to cater to the growing demand across the region. Such developments are expected to drive the growth of the market in focus in the region.

Aerospace MRO Industry Overview

The market for commercial aircraft MRO is highly fragmented, with many players with different MRO capabilities offering services both globally and regionally. GE Aviation, AAR Corp., Safran SA, Raytheon Technologies Corporation, and Lufthansa Technik AG are some of the prominent players in the commercial aircraft MRO market. Currently, the positive market outlook of the MRO market led to new players entering the market and existing players expanding their presence in new geographical locations. For instance, in February 2021, SIA Engineering Company Limited established a new Engine Services Division (ESD) to develop and provide engine services like engine maintenance, parts repair, on-wing services, storage and preservation, material management, and engine testing. The new business unit is expected to complement SIAEC's network of engine joint ventures in Singapore. Furthermore, the companies are investing in artificial intelligence, robotics, drones, big data, and blockchain technologies to support maintenance, repair, and overhaul activities. With the advent of newer generation aircraft, the TBO (Time Between Overhaul) of aircraft is increasing, which may challenge the existence of smaller players in the coming years. However, the revenue generated from regular maintenance and repair of aircraft will continue to increase with the growing fleet.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Currency Conversion Rates for USD

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

- 3.1 Market Size and Forecast, Global, 2018 - 2027

- 3.2 Market Share by MRO Type, 2021

- 3.3 Market Share by Geography, 2021

- 3.4 Structure of the Market and Key Participants

- 3.5 Expert Opinion on the Commercial Aircraft Maintenance, Repair, and Overhaul (MRO) Market

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size and Forecast by Value - USD billion, 2018 - 2027)

- 5.1 MRO Type

- 5.1.1 Airframe

- 5.1.2 Engine

- 5.1.3 Component

- 5.1.4 Line

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 France

- 5.2.2.3 Germany

- 5.2.2.4 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Rest of Latin America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 Qatar

- 5.2.5.4 Rest of Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 AAR Corp.

- 6.2.2 Delta TechOps (Delta Air Lines Inc.)

- 6.2.3 GE Aviation

- 6.2.4 Hong Kong Aircraft Engineering Co. Ltd

- 6.2.5 Lufthansa Technik AG

- 6.2.6 Raytheon Technologies Corporation

- 6.2.7 SIA Engineering Company Ltd

- 6.2.8 TAP Maintenance & Engineering

- 6.2.9 Singapore Technologies Engineering Ltd

- 6.2.10 MTU Aero Engines AG

- 6.2.11 Rolls-Royce Holding PLC

- 6.2.12 Safran SA

- 6.2.13 Air India Engineering Services Ltd

- 6.2.14 Emirates Engineering

- 6.2.15 StandardAero

- 6.2.16 AFI KLM E&M

- 6.2.17 Avia Solutions Group PLC

- 6.2.18 Garuda Indonesia (GMF AeroAsia)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS