PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1403809

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1403809

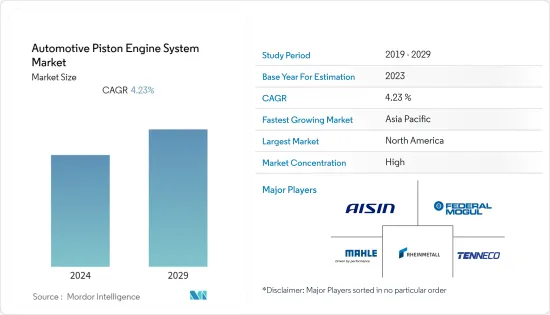

Automotive Piston Engine System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

The automotive piston engine system market is valued at USD 4.26 billion in the current year. It is anticipated to reach a net valuation of USD 5.24 billion within the next five years, registering a CAGR of 4.23% over the forecast period.

Innovations and prototypes of engines from major automakers and original equipment manufacturers (OEMs), coupled with consumer preferences for high-performance and fuel-efficient automobiles, are some of the major factors propelling the market growth. Engine downsizing trends are on the rise, with automakers developing smaller engines with better fuel injection systems. Further, the rapid transformation of the automotive industry in integrating lightweight components in their vehicle models is propelling the growth of the automotive piston engine system market. It is owing to the enhancement in technology and commitment by several parts and component manufacturers to develop advanced pistons, which assist in improving vehicle efficiency.

With the increasing focus of the government to promote the usage of electric vehicles to combat carbon emissions, the sales trends of fuel-operated vehicles are significantly being affected. It poses a major challenge for the automotive piston engine system market, as the integration of pistons in electric vehicles is optional. On the other hand, the production of piston systems is gaining traction in the aftermarket channels, owing to the growth in vehicle parc. Consumers availing of used cars are constantly in need of upgrading their vehicle's parts and components. These positively impact the demand for the automotive piston engine systems market.

With China, India, and Japan growing as global automotive manufacturer hubs, the Asia-Pacific region is expected to continue as a major market for automotive piston systems due to the increase in manufacturing of alternative fuel vehicles such as liquefied petroleum gas (LPG), compressed natural gas (CNG), and diesel engines. Further, the market is anticipated to witness the development of various lightweight piston components to improve the efficiency of vehicles and better fuel consumption capability.

Automotive Piston Engine System Market Trends

Passenger Car Segment is Anticipated to Dominate the Market

Increasing preference of consumers to avail alternative fuel vehicles, such as LPG CNG operated cars, is anticipated the growth of the piston engine system market. Various auto manufacturers are constantly spending hefty sums in developing new-age vehicles, which require lightweight piston components to be utilized in the vehicles. Coupled with that, the growing demand for used cars in several regions and increasing vehicle parc, owing to consumers' preference towards availing private transportation medium, is positively impacting the demand for automotive piston engine system market. The increasing age of vehicles requires constant upgradation, and therefore, changing piston systems in the aftermarket for fuel-operated vehicles is expected to drive this segment of the market.

On the other hand, the rise in sales of electric vehicles is hindering the growth of the automotive piston system market. The spike in sales is the result of an increase in regulatory norms by various organizations and governments to control emission levels and to propagate zero-emission vehicles. As a result, automakers are continually working and focusing on increasing their expenditure on the R&D of electric vehicles, which may aid OEMs in marketing electric vehicles in the future.

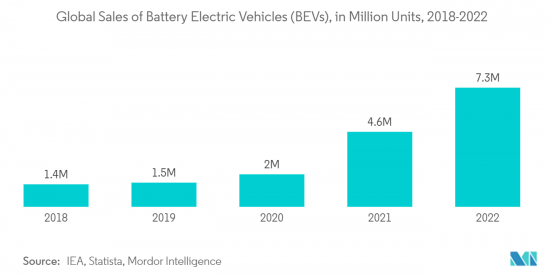

The global electric vehicles (including battery electric vehicles, fuel cell electric vehicles, and plug-in hybrid vehicles) market observed a tremendous increase in the number of sales registered every year since 2018. This increase was registered in almost all segments of vehicles, which include passenger vehicles and commercial vehicles. For instance-

- In 2022, global sales of battery electric vehicles (BEVs) touched 7.3 million units, compared to 4.6 million units in 2021, representing a 58.7% Y-o-Y growth between 2021 and 2022.

With the increased inclination toward electric vehicles, governments of different countries offering subsidies, and the growing need for automation and reduced emissions, the electrification of the automotive industry will serve as a major restraint for the market during the forecast period.

Asia-Pacific to Dominate the Market during the forecast period

Asia-Pacific region is projected to be the leading region for the automotive piston engine system market during the forecast period. It is mainly due to the heavy reliance on internal combustion engines, especially in the commercial vehicles sector. For instance,

- In 2022, India witnessed sales of 933 thousand units of commercial vehicles, compared to 677 thousand units in 2021, recording a Y-o-Y growth of 37.8% between 2021 and 2022.

- Similarly, new sales of commercial vehicles in Indonesia touched 264 thousand units in 2022, compared to 227 thousand units in 2021, representing a 16.3% Y-o-Y between 2021 and 2022.

Although electric commercial vehicles in the Asia-Pacific region gained traction in recent years, the market of ICE commercial vehicles remained strong as of 2022. However, with the increasing penetration of ICE commercial vehicles in the Asia-Pacific market, the automotive piston engine system market might witness falling growth in the coming years.

The increasing urbanization rate, growing vehicle parc, and the rising per capita disposable income of consumers are driving the automotive market in the Asia-Pacific region. As more consumers migrate to urban for better employment and financial opportunities, the preference towards availing private transportation medium shoots up, which positively impacts the passenger car market in the region. It, in turn, positively impacts the position engine system market in this region.

Despite the ramping penetration of electric vehicles at a faster rate, there remains a massive potential in the aftermarket for piston manufacturers to cater to consumers who avail of fuel-operated used cars. With the immense market for conventional IC engines in the regions, despite the growing inclination toward electric vehicles, the growth potential for automotive piston engine systems is expected to be high in Asia-Pacific during the forecast period.

Automotive Piston Engine System Industry Overview

The automobile piston engine system market is consolidated and highly competitive, with only a few companies dominating the market. Some of the major companies operating in the market are Aisin Seiki, Federal-Mogul Holding LLC, Mahle GmbH, Tenneco Inc, Rheinmetall Automotive AG, Hitachi Automotive Systems, and Riken Corporation, among others. These players actively engage in forming long-term partnerships with auto manufacturers to enhance their brand portfolio by offering various piston components for gasoline or diesel vehicles.

- In January 2023, Rheinmetall officially transferred its large-bore pistons production to Koncentra Verkstads AB (KVAB) of Gothenburg, Sweden. In October 2022, Rheinmetall announced the sale, which reflected the Dusseldorf tech group's strategic reorientation towards an improved focus on developing small-bore pistons.

- In August 2022, Nippon Piston Ring and Riken Corporation announced a Memorandum of Understanding (MoU) agreement to establish a joint holding company formed by mutual stock transfer. It is to consolidate the two companies on equal terms. As per the agreement, the trading name of the new joint company will be NPR-Riken Corporation. The company aims to facilitate the development of advanced position solutions for the automotive industry.

The market is anticipated to witness the launch of various advanced lightweight piston components in the coming years as these players try to gain a competitive edge with the diversification of their product portfolio.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Growing Demand for Lightweight Pistons

- 4.2 Market Restraints

- 4.2.1 Increasing Adoption of Electric Vehicles Deters the Growth of the Market

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD)

- 5.1 By Raw Material Type

- 5.1.1 Cast Iron

- 5.1.2 Aluminum Alloy

- 5.1.3 Other Raw Materials (Steel, etc.)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commerical Vehicles

- 5.3 By Fuel Type

- 5.3.1 Gasoline

- 5.3.2 Diesel

- 5.4 By Component Type

- 5.4.1 Piston

- 5.4.2 Piston Ring

- 5.4.3 Piston Pin

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 South America

- 5.5.4.2 Middle-East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Aisin Seiki

- 6.2.2 Capricorn Automotive

- 6.2.3 Federal Mogul Holding LLC

- 6.2.4 Mahle GmbH

- 6.2.5 Rheinmetall

- 6.2.6 Hitachi Automotive Systems

- 6.2.7 Shriram Pistons & Rings Ltd

- 6.2.8 Magna International

- 6.2.9 Tenneco Inc

- 6.2.10 Riken Corporation

- 6.2.11 PT Astra Otoparts Tbk

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Opportunity in the Aftermarket owing to the Growth in Used Gasoline/Diesel Cars