PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444620

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444620

Telecom Cloud - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

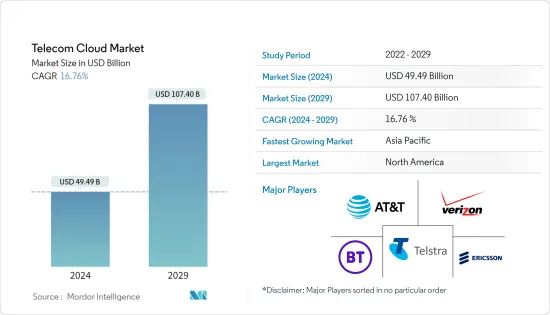

The Telecom Cloud Market size is estimated at USD 49.49 billion in 2024, and is expected to reach USD 107.40 billion by 2029, growing at a CAGR of 16.76% during the forecast period (2024-2029).

The latest trend of cloud technology has enabled telecommunication organizations to migrate to the internet, where there is no longer the need to have costly hardware for businesses to stay connected to the rest of the world.

Key Highlights

- A distributed computing network that combines cloud-native technologies, network function virtualization and software-defined networking is known as the "telecommunication cloud." Since network and computing resources are dispersed across several locations and clouds, automation and orchestration are crucial. This development is the deployment of a virtualized, programmable, and artificially intelligent network architecture. Adopting cutting-edge cloud business tactics that modify network architecture is another aspect. Some global telecom cloud trends include rising internet and mobile device adoption and the quick digital transformation of various businesses.

- The advancements in information and communications technology have brought remarkable changes in global business operations. Various government and public enterprises are dependent on critical information infrastructure services. Also, organizations are now showing more interest in cloud services to meet the growing demand from business operations.

- The increasing demand for over-the-top cloud services, lower operational and administrative costs, and growing awareness about telecom cloud among enterprises are expected to boost the market's growth.

- With the rising demand for cost-effective and user-friendly browser-based communication solutions, many notable vendors are looking to introduce vertical-specific WebRTC solutions and services in North America, which is expected to boost the market's growth. However, the risk of cyber threats poses a significant challenge to market growth, as cyber attacks on telecommunication operators can disrupt services for phone and internet consumers, cripple businesses, and shut down government operations.

- Due to the Covid-19 pandemic, the telecom industry is experiencing a transformational period of advancement to adjust to new technologies and cloud patterns. With an increasing number of people working from home, obtaining educational resources for homeschooling and streaming video entertainment is rising. Given this, the telco industry is naturally seeing spikes in voice, data, and broadband services.

Telecom Cloud Market Trends

Solution Expected To Dominate the Telecom Cloud Market

- The solution area includes options for network function virtualization, unified communication and collaboration, and content delivery networks. The growing use of the internet and mobile devices is driving the acceptance of solutions. As a result, organizations need to leverage new technology more and more to improve operational efficiency and organizational agility. Applications used by businesses include voicemail, email, IM (instant messaging), unified messaging, audio, web, and video conferencing, file sharing, whiteboarding, social networking, and more.

- The solution offerings in the market include unified communication and collaboration, a content delivery network, and other solutions. This is majorly owing to the increasing internet and mobile device penetration. With this, businesses increasingly acknowledge the need to leverage advanced technologies to improve business agility and gain operational efficiencies.

- They are deploying a broad array of communications and collaboration applications, including telephone, email, voice mail, unified messaging, instant messaging (IM) and presence, audio, web, and video conferencing, file sharing and whiteboarding, mobility, social networking, and more.

- Additionally, the exponentially rising media content and demand for rich video content among the increasing online users, along with the trend of digitization among organizations across end-user verticals, spurs the need for content delivery network solutions.

North America Holds the Major Share in the Telecom Cloud Market

- North America witnessed a huge penetration from large enterprises with technically-skilled employees, providing continuous innovative technologies. In the U.S. and Canada, there is an increase in the use of hybrid telco cloud installations, which enables the integration of best-in-class data analytics and artificial intelligence available in the public cloud sector to anticipate and meet the needs and preferences of consumers. The businesses also use the cloud to get rid of silo databases, combine customer data, offer an engaging Omni channel customer experience, and develop a 360-degree view of the customer.

- The consumerization of IT, which is also to blame for this region's dominance, may be linked to the current boom in mobility and the development of intelligent mobile gadgets. In addition, several well-known manufacturers are looking into the possibilities of providing industry-specific WebRTC solutions and services in North America in response to the growing need for browser-based communication solutions that are user-friendly and economical. Indirectly, this is anticipated to accelerate market growth.

- Further, the dominance of this region can be attributed to the recent increase in mobility and the explosion of smart mobile devices due to the consumerization of IT. Moreover, with the rising demand for cost-effective and user-friendly browser-based communication solutions, many notable vendors are looking to introduce vertical-specific WebRTC solutions and services in North America, which is indirectly expected to boost the market's growth.

- Recently, A wide range of brand-new telecommunications solutions aimed at businesses, cloud and service providers, and even homes were displayed at MWC Las Vegas this year. Here is a selection of five fresh goods and services displayed at North America's most important connectivity event.

- COVID-19 has created a new inflection point that requires every regional telecom provider to dramatically accelerate the move to the cloud as a foundation for digital transformation to build the resilience, new experiences and products, and structural cost reduction that the ongoing health, economic, and societal crisis demands.

Telecom Cloud Industry Overview

The major players include AT&T Inc., BT Group PLC, Verizon Communications Inc., Level 3 Communications Inc., Telefonaktiebolaget L.M. Ericsson, Deutsche Telekom, and NTT Communications Corporation. These players are increasingly undertaking mergers and acquisitions and product launches to develop and introduce new technologies and products in the market. Hence, the market concentration will be high.

- September 2022 - Wind River and Dell Technologies have cooperated to revolutionize telecom cloud installations. The market-first co-engineered Dell solution with Wind River will aid in accelerating the adoption of open, cloud-native network technologies.

- May 2022 - The cloud-native IMS Voice Core product, which Nokia announced the release, will aid CSPs (Communication Service Providers) in enhancing operational agility, streamlining network operations, and lowering the cost of managing their networks.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Scope

- 1.2 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Hybrid Cloud in Telecom

- 5.1.2 Lower Operational and Administration Costs

- 5.2 Market Challenges

- 5.2.1 Risk of Security Breaches

- 5.3 Impact of Covid-19 in Global Telecom Cloud Market

6 KEY TECHNOLOGY INVESTMENTS

- 6.1 Cloud Technology

- 6.2 Artificial Intelligence

- 6.3 Cyber Security

- 6.4 Digital Services

7 MARKET SEGMENTATION

- 7.1 Type

- 7.1.1 Solution

- 7.1.1.1 Unified Communication and Collaboration

- 7.1.1.2 Content Delivery Network

- 7.1.1.3 Other Solutions

- 7.1.2 Service

- 7.1.2.1 Colocation Services

- 7.1.2.2 Network Services

- 7.1.2.3 Professional Services

- 7.1.2.4 Managed Services

- 7.1.3 Other Types

- 7.1.1 Solution

- 7.2 Application

- 7.2.1 Billing and Provisioning

- 7.2.2 Traffic Management

- 7.2.3 Other Applications

- 7.3 Cloud Platform

- 7.3.1 Software-as-a-Service

- 7.3.2 Infrastructure-as-a-Service

- 7.3.3 Platform-as-a-Service

- 7.4 End User

- 7.4.1 BFSI

- 7.4.2 Retail

- 7.4.3 Manufacturing

- 7.4.4 Transportation and Distribution

- 7.4.5 Healthcare

- 7.4.6 Government

- 7.4.7 Media and Entertainment

- 7.4.8 Other End Users

- 7.5 Geography

- 7.5.1 North America

- 7.5.1.1 US

- 7.5.1.2 Canada

- 7.5.2 Europe

- 7.5.2.1 Germany

- 7.5.2.2 UK

- 7.5.2.3 France

- 7.5.2.4 Italy

- 7.5.2.5 Rest of Europe

- 7.5.3 Asia Pacific

- 7.5.3.1 India

- 7.5.3.2 China

- 7.5.3.3 Japan

- 7.5.3.4 Rest of Asia-Pacific

- 7.5.4 Rest of the World

- 7.5.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 AT&T Inc.

- 8.1.2 BT Group PLC

- 8.1.3 Verizon Communications Inc.

- 8.1.4 Telstra Corporation Ltd

- 8.1.5 Telefonaktiebolaget LM Ericsson

- 8.1.6 Deutsche Telekom

- 8.1.7 NTT Communications Corporation

- 8.1.8 CenturyLink Inc

- 8.1.9 Singapore Telecommunications Limited

- 8.1.10 China Telecommunications Corporation

- 8.1.11 Telus Corporation

- 8.1.12 Swisscom AG

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE TRENDS