PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1403970

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1403970

Patient Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

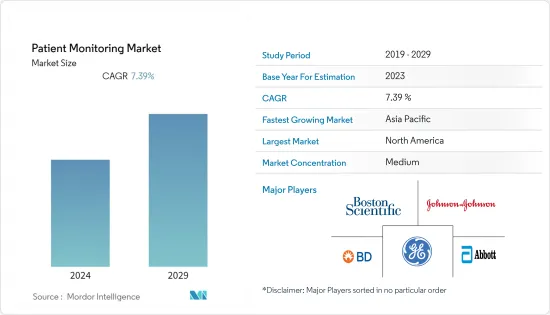

The Global Patient Monitoring Market size is expected to grow from USD 43.8 billion in 2024 to USD 62.6 billion by 2029, registering a CAGR of 7.39% during the forecast period (2024-2029).

The patient monitoring market was valued at USD 37,115.97 million in the base year and is expected to register a CAGR of 8.97% over the forecast period.

The outbreak of the pandemic impacted the patient monitoring market. During the pandemic, the demand for patient monitoring devices such as neuromonitoring, respiratory, and cardiac devices drastically increased due to the need for constant monitoring of COVID-19 patients. For instance, according to the NCBI study published in October 2022, wearable respiratory sensors were widely used during the pandemic as they can monitor biomechanical signals, such as the abnormities in respiratory rate and cough frequency caused by COVID-19, as well as biochemical signals, such as viral biomarkers from exhaled breaths. Thus, the market witnessed healthy growth during the pandemic and is expected to maintain an upward trend over the forecast period.

The growth of the patient monitoring market is attributed to the rising burden of chronic diseases due to lifestyle changes, growth in the geriatric population, growing preference for home and remote monitoring, and the ease of use of portable devices. For instance, according to the June 2022 update of the Centers for Disease Control and Prevention (CDC), one or more chronic diseases, such as diabetes, cancer, heart disease, and stroke, affect six out of ten Americans. These and other chronic illnesses are the main contributors to health care costs and the significant causes of death and disability in the United States. Similarly, according to the data published by the NCBI in April 2022, an estimated 6.5 million Americans aged 65 and older were living with Alzheimer's dementia in 2022. The number is expected to grow to 13.8 million by 2060. Thus, such a high burden of chronic diseases is expected to increase the demand for patient monitoring devices as these diseases require constant monitoring, in which patient monitoring devices come into play. In addition, constant monitoring reduces readmission rates, prevents avoidable hospitalizations, decreases the number of unnecessary trips to the doctor's office, and reduces travel-related expenses. With the proper implementation, patient monitoring technologies can expand access to quality healthcare and save time and money. Thus, considerable market growth is expected over the forecast period due to such factors.

Additionally, initiatives such as expansion and product launches are other factors responsible for the market's growth. For instance, in September 2021, the Indian subsidiary of Medtronic partnered with Stasis Health to expand access to Statis Monitor, a connected care bedside multi-parameter monitoring system across India. Similarly, in July 2021, Terumo Corporation launched Japan's Dexcom G6 continuous glucose monitoring system. Dexcom, Inc., based in the United States, manufactures the product, and Terumo holds the exclusive distribution agreement in Japan. Such developments are likely to bolster the growth of the patient monitoring market over the forecast period.

However, resistance from healthcare industry professionals toward adopting patient monitoring systems and the high cost of technology will likely hinder the market growth over the forecast period.

Patient Monitoring Market Trends

The Cardiology Segment is Expected to Witness Considerable Market Growth Over the Forecast Period

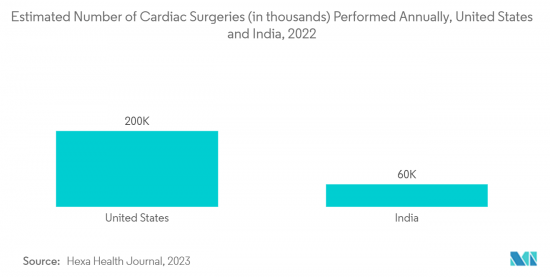

In cardiology, patient monitoring devices are used to diagnose and monitor various disorders or abnormalities of the heart and the overall cardiovascular system. The major factor driving the segment's growth is the rising number of cases and deaths due to cardiovascular diseases and the increasing number of cardiac surgeries. For instance, according to the CDC update in January 2023, around 6.2 million adults in the United States have heart failure yearly. Similarly, according to the journal published by HexaHealth in October 2022, around 2,00,000 surgeries were performed in the United States and 60,000 in India annually. Post-surgery continuous patient monitoring is essential to track any possibility of complications and the recovery rate in which cardiac patient monitoring comes into play. Thus, increasing cardiac surgeries is also expected to surge the segment growth.

Furthermore, product launches and favorable initiatives by the market players in the cardiac monitoring space are also likely to fuel the growth of this segment. For instance, in June 2022, GE Healthcare launched its wireless patient monitoring system, Portrait Mobile. The product helps capture respiration rate, oxygen saturation, and pulse rate for general ward and post-surgery patients continuously, allowing clinicians to act early and avert serious adverse events. Similarly, in January 2021, Boston Scientific Corporation acquired PreventiceSolutions, Inc., a privately held company offering remote and wearable cardiac monitors for adults and pediatric patients. The acquisition will establish a strong footprint for Boston Scientific Corporation in the implantable cardiac monitor market. It is an implantable diagnostic device for detecting arrhythmias. Therefore, owing to the above factors, the segment is anticipated to grow considerably over the forecast period.

North America Region Holds a Considerable Market Share Over the Forecast Period

The North American patient monitoring market is expected to witness considerable growth and is estimated to show a similar trend over the forecast period. The increasing geriatric population, rising incidences of chronic diseases, growing demand for wireless and portable systems, and sophisticated reimbursement structures aimed at cutting out-of-pocket expenditure levels are the major factors attributed to its large market share. For instance, according to a report published by the Public Health Agency of Canada in December 2021, the crude incidence rate per 100,000 persons aged 65 years and more for ischemic heart disease was 2,306.9 in men and 1,537 for women and chronic obstructive pulmonary disease was 1,750.6 in men and 1,411.4 in women. In addition, according to the report published by the Canadian Chronic Disease Surveillance System in November 2022, the overall number of adults aged 65 years and older who were to be living with chronic conditions were expected to be about 6.3 million in the coming years. Thus, owing to such instances, considerable market growth is expected over the forecast period.

In the North America, the United States is expected to witness significant growth over the forecast period. The product launches by the key players and product approvals in the country are the major drivers for the market. For instance, in July 2021, Abbott introduced Jot Dx, an insertable cardiac monitor. It is designed to reduce data burden and diagnose abnormal heart rhythms. Similarly, in July 2022, Switzerland-based medical technology company Sleepiz received the U.S. FDA clearance for Sleepiz One+ contactless respiration and heart rate measuring device and was launched in the United States. Sleepiz One+ is one of the first respiratory monitoring devices that non-contactly monitors and records patient data during sleep. Sleepiz technology enables a new perspective on patient health, as doctors no longer rely on random check-up measurements but instead have access to continuous data. Thus, owing to the launch of innovative products and the rising prevalence of chronic diseases in the North American region, the market is expected to witness a high growth rate over the forecast period.

Patient Monitoring Industry Overview

The patient monitoring market is moderately competitive and consists of several major players. The companies are implementing certain strategic initiatives, such as mergers, new product launches, acquisitions, and partnerships, that help strengthen their market position. The key players in the market are Abbott Laboratories, Baxter International Inc., Boston Scientific Corporation, Becton, Dickinson and Company, General Electric Company (GE Healthcare), and Johnson & Johnson, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of Chronic Diseases due to Lifestyle Changes

- 4.2.2 Growing Preference for Home and Remote Monitoring

- 4.3 Market Restraints

- 4.3.1 Resistance from Healthcare Industry Professionals Toward the Adoption of Patient Monitoring Systems

- 4.3.2 High Cost of Technology

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Type of Device

- 5.1.1 Hemodynamic Monitoring Devices

- 5.1.2 Neuromonitoring Devices

- 5.1.3 Cardiac Monitoring Devices

- 5.1.4 Multi-parameter Monitors

- 5.1.5 Respiratory Monitoring Devices

- 5.1.6 Other Types of Devices

- 5.2 By Application

- 5.2.1 Cardiology

- 5.2.2 Neurology

- 5.2.3 Respiratory

- 5.2.4 Fetal and Neonatal

- 5.2.5 Weight Management and Fitness Monitoring

- 5.2.6 Other Applications

- 5.3 By End-User

- 5.3.1 Home Healthcare

- 5.3.2 Hospitals and Clinics

- 5.3.3 Other End-Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Baxter International Inc.

- 6.1.3 Boston Scientific Corporation

- 6.1.4 Becton, Dickinson and Company

- 6.1.5 General Electric Company (GE Healthcare)

- 6.1.6 Johnson & Johnson

- 6.1.7 Masimo Corporation

- 6.1.8 Medtronic PLC

- 6.1.9 Omron Corporation

- 6.1.10 Koninklijke Philips NV

- 6.1.11 Dragerwerk AG & Co. KGaA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS