PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1404521

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1404521

Food Processing Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

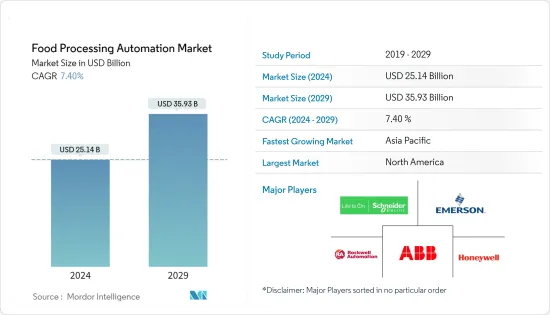

The Food Processing Automation Market size is estimated at USD 25.14 billion in 2024, and is expected to reach USD 35.93 billion by 2029, growing at a CAGR of 7.40% during the forecast period (2024-2029).

Automation has been adopted in manufacturing plants for the last 50 years, and it is increasing day by day. The food industry has become one of the fastest-growing segments of plant automation. The food industry is growing tremendously and is one of the major sectors contributing to GDP.

Key Highlights

- The demand for processed goods is increasing, with increased buying power and changing lifestyles. This has made it necessary for food manufacturers to implement automation to improve the processing rate to meet consumers' demands. Furthermore, the rapid development of computer technology, dynamic changes in consumers' preferences, and regulatory bodies have boosted the need for food quality and safety. This has resulted in the growing adoption of automated systems in the food industry.

- Automation provides direct and indirect benefits to the production line, including increased waste reduction and speed. Indirect benefits can range from increased workplace safety and precision to longer operational hours at a lower total budget; vendors operating in the market are increasingly focusing on adopting these solutions to drive efficiency and their operational capabilities.

- Food processing has improved the palatability and shelf-life of foods. Processed food items undergo at least some processing and thus include moderately and highly processed foods. Advancements in the food processing industry, innovation in processing technology, and continuous growth in the requirement for processed food are expected to support the development of food and beverage processing equipment.

- The installation and acquisition cost of a control system for an intelligent factory represents half of the total cost during its lifetime. Additionally, the frequent changes in networking and technology also result in significant cost increases, which is much more than the initial investment, further restraining the adoption. Even significantly low adoption among SMEs, especially in developing countries, like Brazil, that cannot bear the product costs, is restraining the market's growth.

- The COVID-19 pandemic and its associated lockdown limitations caused disruptions in manufacturing operations and supply chains worldwide. Under these constrained circumstances, multiple industries worldwide witnessed a massive decline in revenue and profits, resulting in an overall slowdown in investment activities, especially related to new technology adoption and expansion.

- In the post-COVID-19 scenario, with the economy returning to normalcy and vendors increasingly focusing on adopting automation and advanced digital solutions, the studied market is expected to witness upward growth during the forecast period.

Food Automation Market Trends

Beverages End-user Industry is Expected to Hold Significant Market Share

- The beverage industry has been among the leading adopters of automation and robotic solutions, enabling manufacturers to combine slow batch production with high-speed filling and other packaging operations. Automation solutions such as autonomous robots, palletizers, robotic arms, etc., also help companies efficiently manage the warehouse and reduce product damage due to human error.

- One of the most basic functions of automation in a beverage plant is the prevention of fundamental mistakes, like mismatching products with packaging, incorrect labeling, inappropriate handling, etc., which can often happen due to human error.

- With product lines diversifying with more new beverage types and flavors and regulatory and product safety requirements tightening with increasing demand for freshness and convenience, the role of automation is becoming increasingly prevalent in the beverage industry.

- The growing market demand for alcoholic and non-alcoholic beverages also encourages vendors to adopt automation solutions as they help speed up the production, packaging, and warehousing processes. Software solutions such as warehouse execution systems (WES) and process monitoring software are increasingly being integrated with autonomous hardware and production robots to help beverage manufacturers have real-time data regarding the quality and efficiency of the process. These solutions also enable them to undertake preventive maintenance based on real-time data.

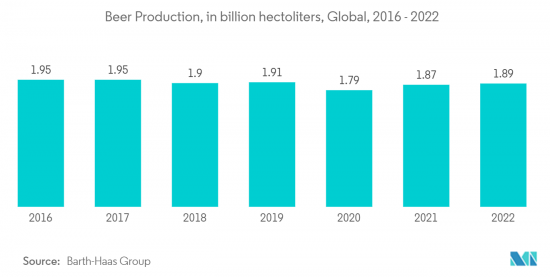

- Beverage production has witnessed steady growth over the years. The factor that is largely contributing to the demand for automation is the increasing consumption of packaged beverages. The major contributing factors behind this growth are changing consumer lifestyles, especially in emerging regions, and the rapid expansion of distribution channels and e-commerce. According to Barth-Haas Group, in 2022, the global beer production amounted to approximately 1.89 billion hectoliters.

North America is Expected to Hold Significant Market Share

- The United States is witnessing a significant growth rate owing to the region's growing food and beverage industry due to health awareness, disposable income, and increasing urbanization. As a result, many companies in the F&B industry are moving from manual processing to automation to grow output and develop new products, which may ultimately drive the market's growth.

- The growing urbanization in the country is further driving the market's growth. According to the World Bank, the United States is one of the earliest nations to industrialize, and it has had a comparatively high rate of urbanization over the past two centuries. By the midpoint of the century, almost 90% of the population is expected to live in an urban setting. Furthermore, the total population in the United States living in urban areas is anticipated to grow by 84.86% by 2030, leading to the increasing demand for food and beverages in the country.

- Moreover, according to the National Agricultural Statistics Service, the United States produced about 226.6 billion pounds of milk for human consumption in 2022, an increase from 218.3 billion pounds of milk in 2019. The increased food and beverage production in the region is anticipated to boost the growth of the studied market.

- According to BDC, the Canadian food and beverage (F&B) industry is anticipated to grow by more than 11% by the end of 2025. About 46% of Canadian food processors invest in advanced or emerging technologies.

- The increasing incidences of foodborne diseases and food poisoning cases caused by contaminated packaged food have increased the need for a more secure and safe food production process, which may be accomplished with the assistance of industrial robots. This is propelling the food automation market.

Food Automation Industry Overview

The degree of competition in the food automation market is high with the presence of major players like Schneider Electric SE, Rockwell Automation Inc., Honeywell International Inc., Emerson Electric Company, ABB Ltd, Mitsubishi Electric Corporation, Siemens AG, and Yokogawa Electric Corporation. Players in the market are adopting strategies such as partnerships, product launches, innovations, investments, and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

In February 2023, Regal Rexnord Corporation debuted its new Rexnord Curve System with 1540 Series MatTopChain for conveyor lines that require a zero tangent 180 and/or 90-degree curve. The system has the industry's tightest inner radius (420 mm) and smallest transfer (15 mm), significantly improving space utilization and package handling. Head-to-tail transfer of even small and light cases is possible with the new Rexnord Curve System, which eliminates the need for micro-pitch conveyors, transfer modules, or plates.

In December 2022, Rockwell Automation introduced FactoryTalk Vault to automate project analysis, store and protect industrial files, and streamline work processes. For manufacturing design teams, FactoryTalk VaultTM provides centralized, secure, cloud-native storage. With its contemporary version and access control, FactoryTalk Vault, with enhanced Design Tools, enables deeper examination of controller projects for more essential insights into designs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products and Services

- 4.3.5 Degree of Competition

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Emphasis on Food Safety and Rising Demand for Processed Food

- 5.2 Market Challenges

- 5.2.1 High Capital Investments

6 INDUSTRY STANDARDS AND REGULATIONS

7 MARKET SEGMENTATION

- 7.1 By Operational Technology and Software

- 7.1.1 Distributed Control System (DCS)

- 7.1.2 Manufacturing Execution Systems (MES)

- 7.1.3 Variable-frequency Drive (VFD)

- 7.1.4 Valves and Actuators

- 7.1.5 Electric Motors

- 7.1.6 Sensors and Transmitters

- 7.1.7 Industrial Robotics

- 7.1.8 Other Technologies

- 7.2 By End User

- 7.2.1 Dairy Processing

- 7.2.2 Bakery and Confectionary

- 7.2.3 Meat, Poultry, and Seafood

- 7.2.4 Fruits and Vegetables

- 7.2.5 Beverages

- 7.2.6 Other End Users

- 7.3 By Application

- 7.3.1 Packaging and Repackaging

- 7.3.2 Palletizing

- 7.3.3 Sorting and Grading

- 7.3.4 Processing

- 7.3.5 Other Applications

- 7.4 By Geography

- 7.4.1 North America

- 7.4.1.1 United States

- 7.4.1.2 Canada

- 7.4.2 Europe

- 7.4.2.1 United Kingdom

- 7.4.2.2 Germany

- 7.4.2.3 France

- 7.4.2.4 Rest of Europe

- 7.4.3 Asia-Pacific

- 7.4.3.1 China

- 7.4.3.2 India

- 7.4.3.3 Japan

- 7.4.3.4 Rest of Asia-Pacific

- 7.4.4 Latin America

- 7.4.5 Middle East and Africa

- 7.4.1 North America

8 VENDOR MARKET SHARE ANALYSIS

- 8.1 Vendor Market Share Analysis (Excl. Industrial Robots)

- 8.2 Vendor Market Share Analysis for Industrial Robots

9 COMPETITIVE LANDSCAPE

- 9.1 Company Profiles

- 9.1.1 Schneider Electric SE

- 9.1.2 Rockwell Automation Inc.

- 9.1.3 Honeywell International Inc.

- 9.1.4 Emerson Electric Company

- 9.1.5 ABB Limited

- 9.1.6 Mitsubishi Electric Corporation

- 9.1.7 Siemens AG

- 9.1.8 Yokogawa Electric Corporation

- 9.1.9 Yaskawa Electric Corporation

- 9.1.10 GEA Group AG

- 9.1.11 Rexnord Corporation (Regal Rexnord Corporation)

10 INVESTMENT ANALYSIS AND OUTLOOK