PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1331351

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1331351

Latin America Agricultural Machinery Market Size & Share Analysis - Growth Trends & Forecasts (2023 - 2028)

The Latin America Agricultural Machinery Market size is estimated at USD 8.70 billion in 2023, and is expected to reach USD 11.70 billion by 2028, growing at a CAGR of 6.10% during the forecast period (2023-2028).

Key Highlights

- Farmers in farmers in Mexico, Argentina, and Brazil are accepting mechanization in their farms. With the increasing demand for food and the need to produce more efficiently, the use of agricultural machinery is becoming more prevalent in many parts of the world.

- The support of government subsidy programs is also a significant factor in the rising adoption of mechanization in agriculture. By providing financial assistance to farmers who wish to purchase agricultural machinery, these programs make it more accessible for farmers to acquire the tools they need to improve their productivity and efficiency..

- The area under harvest in the region is increasing, and farmers have been able to generate more income as compared to the previous years. Thus, they have higher dispensable incomes to invest in machinery and other agricultural inputs. The Central and South American agricultural machinery market is dominated by local market players that are introducing new technologies to attract the attention of farmers.

- Farm mechanization in Brazil's agriculture sector has been slower than in other countries. However, the use of tractors and large machinery is gradually increasing, particularly in the South and Southeast regions as well as the western frontier. The availability of tractors and other large machinery in the Northeast region of Brazil is limited, and this has led to continued reliance on manual labor, even for sugarcane plantations.

- The United States is one of the largest exporters of agricultural machinery to the Latin American region. However, recently, imports from the Central and South American region declined because of the regulation on import taxes. Trade disagreement between the United States and Mexico led to declining demand from the country. China and Canada are the two other major exporters of agricultural machinery to the region.

Latin America Agricultural Machinery Market Trends

Increase in Area Harvested in Latin America

- According to the Organisation for Economic Co-operation and Development (OECD) and the Food and Agriculture Organization (FAO) (OECD-FAO) report 2022, cropland use is projected to grow by 3%, while crop area harvested will grow by 5A% due to the rising prevalence of double cropping system. Of these 7.7 million hectares harvested by 2030, maize and soybean cultivation will increase by almost 53% and 23%, respectively. By 2030, the area will continue to be the world's top producer of soybeans, accounting for more than 54% of worldwide production.

- Average yields are expected to rise over the next ten years by around 10% for most major commodities and will account for a substantial share of production growth. There has been a significant increase in agricultural land under cultivation in Argentina, Brazil, and Mexico. The Pampas region has more than two-thirds of the Argentine agricultural land, and the average size of the cultivated landholding in the region was 533 hectares in 2021. Farmers generally own 10-15% of the land, and the rest of the land is leased on a yearly basis.

- Family farms have around 84% share in the Brazilian agriculture sector, while the other 16% comprises non-family farms. Smaller farms dominate more than 90% of the agricultural land in Mexico. Hence, the average farm size in Mexico can be estimated at around 25 hectares, owing to the rise in the number of smallholder farms under 5 hectares and large farms greater than 100 hectares.

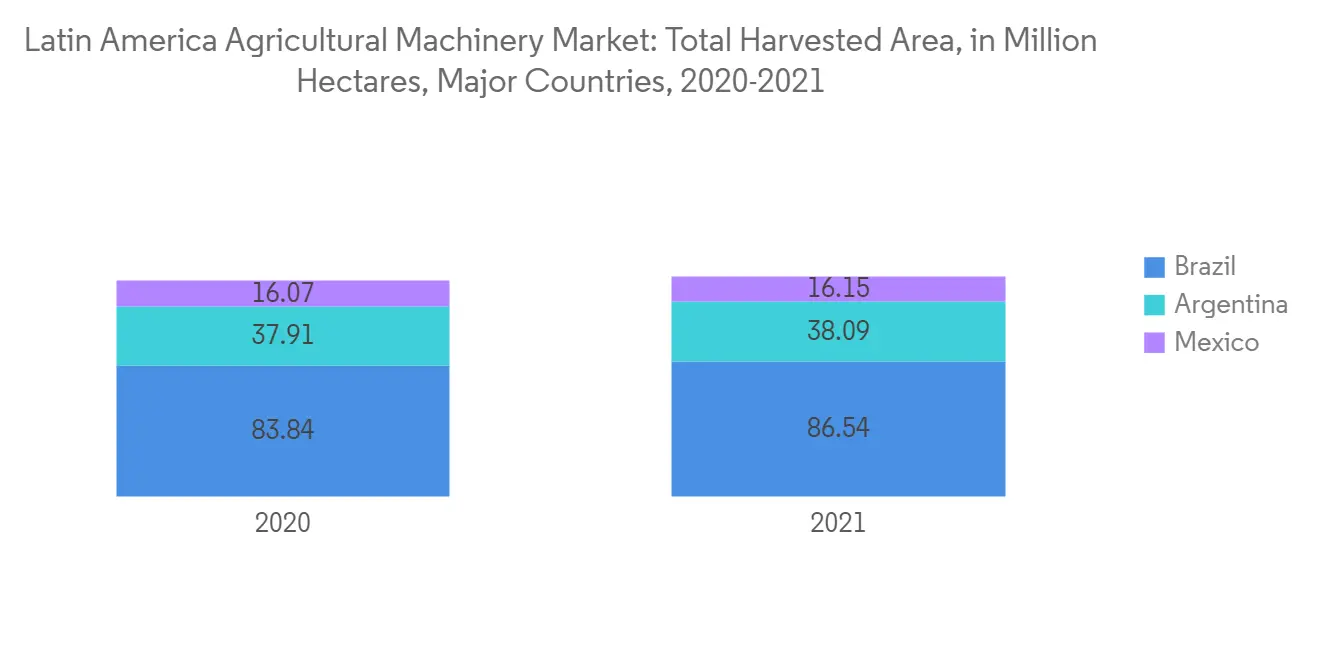

- According to FAO, in 2021, the area harvested for Brazil, Argentina, and Mexico was observed at 86.54 hectares, 38.09 hectares, and 16.15 hectares, respectively. This increase in the area harvested shows that there would be more requirements for agricultural machinery in the region and drives the market during the forecast period.

Brazilian Tractors Dominate the Market

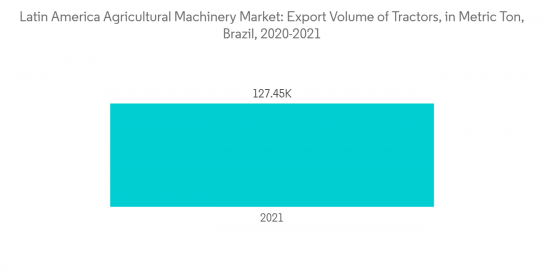

- The use of tractors brought about an important change in agricultural mechanization in the country. The introduction of tractors as a power source provides the possibility of covering large agricultural areas in short periods. Due to the significant increase in row crops and horticultural crops, there is increasing usage of tractors. Pedestrian-controlled tractor exported by Brazil to other countries in the region was observed at USD 0.23 in 2020 and recorded at USD 1.86 million in 2021.

- The international vendors that started investing in Latin America also brought their expertise to the field of agriculture equipment. These players use their global presence and capabilities to invest in research and development to innovate traditional farming activities. Innovative agriculture technologies and products help farmers to increase yield from the same acreage of land.

- Furthermore, the Brazilian government released Crop Plan for the 2022-2023 season. This bill allows small farmers to get credit to buy agricultural machinery, including tractors, at a 5% annual interest rate. Therefore, the advancements in farm technology and mechanization of the production systems of major crops such as soybean are anticipated to increase the market's growth in the forecast period.

Latin America Agricultural Machinery Industry Overview

The agricultural tractors market in the Latin American region is highly consolidated, with very few players capturing most of the market share. The key players in the market include Deere and Company, AGCO Corporation, CNH Industrial NV, Mahindra and Mahindra Ltd, and Kubota Corporation. The main strategy adopted by the key players is to invest in R&D to encourage innovation and maintain a strong market base. The advent of advanced technologies, like artificial intelligence (AI) and robotics, and the growing number of government initiatives have driven the increase in demand for agricultural machinery.

New product launches, partnerships, and acquisitions are the major strategies adopted by the leading companies in the market in the country. Along with innovations and expansions, developing novel product portfolios will likely be the crucial strategy in the coming years. These companies are making strategic partnerships by partnering with domestic companies to expand their distribution network and launch new innovative tractors that cater to the needs of the farmers in this region.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Tractors

- 5.1.1.1 Engine Power

- 5.1.1.1.1 Less than 40 HP

- 5.1.1.1.2 41 to 60 HP

- 5.1.1.1.3 61 to 100 HP

- 5.1.1.1.4 101 to 150 HP

- 5.1.1.1.5 More than 150 HP

- 5.1.2 Equipment

- 5.1.2.1 Plows

- 5.1.2.2 Harrows

- 5.1.2.3 Rotovators and Cultivators

- 5.1.2.4 Other Equipment

- 5.1.3 Irrigation Machinery

- 5.1.3.1 Sprinkler Irrigation

- 5.1.3.2 Drip Irrigation

- 5.1.3.3 Other Irrigation Machinery

- 5.1.4 Harvesting Machinery

- 5.1.4.1 Combine Harvesters

- 5.1.4.2 Forage Harvesters

- 5.1.4.3 Other Harvesting Machinery

- 5.1.5 Haying and Forage Machinery

- 5.1.5.1 Mowers and Conditioners

- 5.1.5.2 Balers

- 5.1.5.3 Other Haying and Forage Machinery

- 5.1.1 Tractors

- 5.2 Geography

- 5.2.1 Brazil

- 5.2.2 Argentina

- 5.2.3 Mexico

- 5.2.4 Peru

- 5.2.5 Chile

- 5.2.6 Rest of Latin America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 AGCO Corporation

- 6.3.2 CNH Industrial NV

- 6.3.3 Deere & Company

- 6.3.4 Kubota Corporation

- 6.3.5 Mahindra and Mahindra Ltd

- 6.3.6 CLAAS KGaA mbH

- 6.3.7 Kuhn Group

- 6.3.8 Yanmar Co. Ltd

- 6.3.9 Agrale SA

- 6.3.10 Aquafim Culiacan

- 6.3.11 EnorossiMexicana SA de C

- 6.3.12 Jumil Mexico Implementos Agricolas

7 MARKET OPPORTUNITIES AND FUTURE TRENDS