PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1406183

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1406183

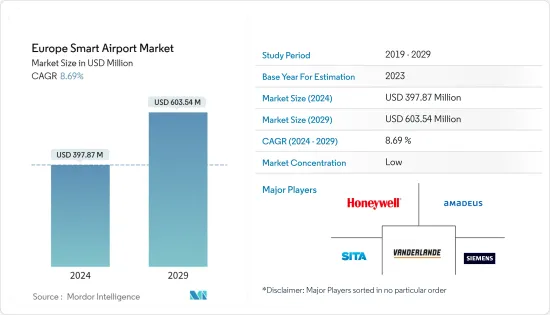

Europe Smart Airport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

The Europe Smart Airport Market size is estimated at USD 397.87 million in 2024, and is expected to reach USD 603.54 million by 2029, growing at a CAGR of 8.69% during the forecast period (2024-2029).

The European region has witnessed gradual air passenger traffic growth in recent years. To cater to the increasing passenger traffic, airport operators in this region have been investing in the modernization of airports. The modernization includes integrating new technologies to enhance operational efficiencies and increase passenger handling capacities. Such investments will generate demand for smart airport solutions in the coming years.

Moreover, technologies such as artificial intelligence (AI), the Internet of Things (IoT), and predictive analysis are being integrated into airports for a wide range of applications to increase automation and revolutionize airport process flow architecture. The integration of advanced technology solutions in the airports is expected to bolster the growth of the European smart airports market during the forecast period.

Furthermore, constructing new airports in the European region will bolster the market's growth shortly.

Europe Smart Airport Market Trends

Passenger, Cargo and Baggage Control Segment Will Showcase Remarkable Growth During the Forecast Period

The passenger, cargo, and baggage control segment is anticipated to grow significantly in the European smart airport market during the forecast period. The change is attributed to the increase in air passenger traffic at various airports in the European region. Moreover, the increased baggage and cargo handled by multiple regional airports will lead to several European airports modernizing themselves using smart technologies to ensure smoother airport operations, thereby driving market growth during the forecast period.

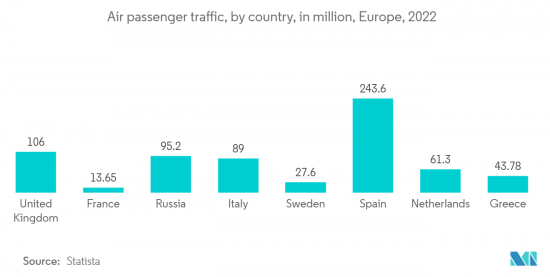

According to the air passenger transport data published by Eurostat, in 2022, there were 820 million passengers carried in the EU, an increase of 119.3 % compared to 2020. Moreover, the biggest recovery in the number of commercial air flights occurred in the second half of 2022. On the other hand, according to data published by Airport Council International (ACI) Europe, passenger traffic across the European airport network nearly doubled (+98%) in 2022 compared to 2021 and reached 1.92 billion passengers. On the other hand, these numbers were still less than the 2019 volume, with just 27% of Europe's airports having fully recovered their 2019 passenger traffic level.

Furthermore, there has been significant growth in the European region in passenger, cargo, and baggage control. The substantial increase in the air traffic passenger in the area has also led to immense growth in the number of passenger baggage being handled by the airports, and this has led to many airports within the region to undergo construction to expand airport capacity to cater to growing air traffic passengers or install several smart technologies for faster baggage processing/handling. For instance, in August 2021, Stansted Airport in the United Kingdom announced that they had completed an upgrade to the baggage handling system worth USD 85.37 million. The airport announced they had installed 2.4 km of conveyor belts, tracks, and 180 automated carts to improve efficiency.

Thus, the increased usage of smart technologies in airports within the European region for passenger, cargo, and baggage control will lead to a positive outlook and significant market growth during the forecast period.

United Kingdom Dominates the Market During the Forecast Period

The United Kingdom stands as a major hub and a key connecting point between the eastern continents and the western continents. Owing to the country's extremely beneficial geographic location for airlines, the United Kingdom witnesses a huge number of passengers converging to change air routes between Asia, the Middle East, and Central Europe, traveling to North and South American countries. According to the data published by the United Kingdom Civil Aviation Authority, air travel in the country witnessed significant growth in 2022, with over 224 million passengers traveling to and from the airports of the United Kingdom and reaching 75 percent of 2019 levels. Moreover, these numbers are a considerable increase from 2021 numbers of 65.4 million passengers who traveled through the airports within the country.

London Heathrow Airport, Gatwick Airport, Stansted Airport, Luton Airport, and Southend Airport are some of the major airports operating various airlines across the United Kingdom. London Heathrow is the major airport connecting major international airlines that operate the trans-Atlantic route from the United Kingdom and toward the North and South American continents. In June 2023, Heathrow airport announced its plans to construct a third runway following the rebound of international air traffic. In addition, the project and its associated new west terminal will help to facilitate an additional 260,000 flights annually from the airport.

Moreover, the increased passenger influx also brings in the need for high-speed internet connectivity for the passengers that wait the long layovers for international or trans-Atlantic air routes. As a result, various airports across the United Kingdom have been upgrading their services to cater to passengers. For instance, in June 2021, London Luton Airport announced that they have unveiled a range of new digital services to improve the passenger experience further. The new services that were unveiled will now include the introduction of unlimited 10mb/s Wi-Fi across the terminal building, the creation of LLA Market Place, which enables passengers to pre-order food and drink contact-free, and an airport's first offer of portable mobile chargers that can be rented for the duration of a trip.

Thus, the increase in the number of air traffic passengers coupled with the rise in the number of airport construction the significant growth in services for the passengers within the region, and the growing development of smart airports within the country will lead to a positive outlook and also lead to significant market growth of smart airports within the United Kingdom during the forecast period.

Europe Smart Airport Industry Overview

The Europe Smart Airport Market is fragmented, with various players engaged in product differentiation to gain significant market share. The most prominent European smart airport market players are SITA, Vanderlande Industries B.V., Amadeus IT Group S.A., Siemens AG, and Honeywell International Inc.

The European smart airports market is highly competitive with many technology providers supporting various stakeholders. The technology providers are integrating advanced technologies like AI, machine learning, and robotics. They are partnering with multiple airport operators, airlines, and airport service providers to improve passenger handling and the efficiency of operations. In addition, the development and introduction of new smart airport solutions by manufacturers within the region are anticipated to support the companies' growth prospects during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Security Systems

- 5.1.2 Communication Systems

- 5.1.3 Air/Ground Traffic Control

- 5.1.4 Passenger, Cargo and Baggage Control

- 5.1.5 Ground Handling Systems

- 5.2 Geography

- 5.2.1 Europe

- 5.2.1.1 United Kingdom

- 5.2.1.2 France

- 5.2.1.3 Germany

- 5.2.1.4 Spain

- 5.2.1.5 Russia

- 5.2.1.6 Rest of Europe

- 5.2.1 Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 SITA

- 6.2.2 International Business Machines Corporation

- 6.2.3 Vanderlande Industries B.V.

- 6.2.4 Amadeus IT Group S.A

- 6.2.5 Siemens AG

- 6.2.6 THALES

- 6.2.7 BEUMER Group GmbH & Co. KG

- 6.2.8 Indra Sistemas, S.A.

- 6.2.9 Honeywell International Inc.

- 6.2.10 Leonardo S.p.A.

- 6.2.11 Leidos Holdings, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS