PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1406205

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1406205

Middle-East And Africa Armored Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

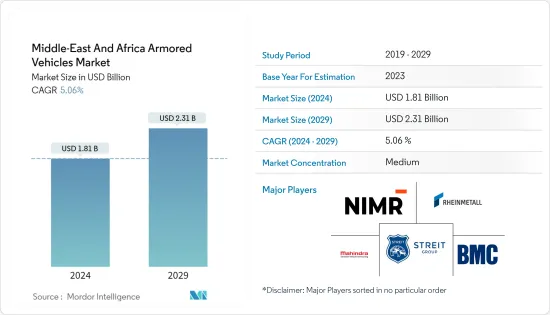

The Middle-East And Africa Armored Vehicles Market size is estimated at USD 1.81 billion in 2024, and is expected to reach USD 2.31 billion by 2029, growing at a CAGR of 5.06% during the forecast period (2024-2029).

An increase in the number of geopolitical and military conflicts in the Middle East and rising security concerns due to terrorist activities leads to growing spending on the defense sector from the Middle Eastern countries. Middle Eastern countries like Saudi Arabia, UAE, and Israel increased their defense expenditure and focus on improving defense capabilities due to rising security threats. Rising procurement of advanced weapons and armored vehicles and the development of next-generation fighting vehicles drive the growth of the market.

The total defense spending of the countries in the Middle East was USD 184 billion in 2022. According to the Stockholm International Peace Research Institute (SIPRI) report published in 2022, Saudi Arabia was the fifth largest defense spender in the world with a defense budget of USD 75 billion. Furthermore, the governments in the region are supporting the local manufacturing of armored vehicles. On the other hand, the occurrence of regular maintenance and electrical failures in armored vehicles and the absence of major armored vehicles OEMs in the region hinders the growth of the market.

Middle East and Africa Armored Vehicles Market Trends

Armored Personnel Carrier (APC) Segment will Showcase Remarkable Growth During the Forecast Period

The armored personnel carrier (APC) segment is anticipated to show significant growth in the Middle East and Africa armored vehicles market during the forecast period. The growth is attributed to the increasing spending on procurement of advanced APCs and rising expenditure on military modernization programs from the Middle Eastern countries. An armored personnel carrier is deployed for carrying soldiers in combat situations, and it can also be armed as a command-post vehicle and used for the evacuation of troops. In the Middle East &Africa, countries are upgrading their fleet of armed vehicles with new and advanced APC, with enhanced protection and situational awareness equipment. For instance, Merkava and Armored Vehicles Directorate of Israel Ministry of Defense (IMOD) developed Eitan, a new multi-purpose 8x8 wheeled armored personnel carrier (APC) that will replace the aging M113 APCs in service with the Israel Defense Forces (IDF).

Also, the EDT Enigma AMFVis is the latest armored personnel carrier manufactured by Emirates Defense Technology to fulfill different battlefield roles for the UAE army. With the growing demand for combat capabilities of APCs, almost all APCs are being equipped with self-defense automatic weapons and remote weapon stations mounted on armored vehicles. The increasing investments in the development of new APCs with better protection and lethality against enemy forces are expected to accelerate the growth of the segment during the forecast period.

Saudi Arabia Dominates the Market During the Forecast Period

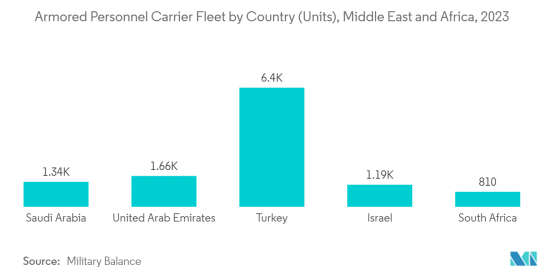

Saudi Arabia held the highest shares in the Middle East and Africa armored vehicles market and continued its domination during the forecast period. The growth is due to increasing focus on enhancing defense capabilities and growing procurement contracts for armored vehicles with OEMs. Saudi Arabia was the largest defense spender in the Middle East.

Over the past few years, the military equipment procurement of the country has increased at a rapid pace due to growing security concerns in the Middle East and rising terrorism in the region. The country also plans to modernize all units of the Saudi Arabian armed forces with new and advanced military equipment to continue developing capabilities. For instance, in February 2021, Saudi Arabian Military Industries (SAMI) entered a partnership with UAE-based Nimr to transfer armored vehicle production and technology to the kingdom. Under the contract, the original equipment manufacturer (OEMs) of JAIS 4x4 MRAP vehicles will likely work together to produce the armored vehicles locally in Saudi Arabia.

Furthermore, the Saudi Arabian Government (SAG) announced that the country will invest over USD 20 billion in its military sector in the next decade. Such robust plans of the government to rapidly increase the fleet of armored vehicles are anticipated to propel the growth of the market in the coming years.

Middle East and Africa Armored Vehicles Industry Overview

The Middle East and Africa armored vehicles market is semi-consolidated in nature due to the presence of few players holding significant shares in the market. Some of the prominent players in the market are Mahindra Emirates Vehicle Armouring FZ-LLC, NIMR Automotive (EDGE Group PJSC), Streit Group, BMC Otomotiv Sanayi ve Ticaret AS., and Rheinmetall AG.

The international armored vehicle manufacturers are making plans to expand their presence in the Middle East and Africa with new product innovations. For instance, Oshkosh Defence is undertaking strategic steps to boost its sales in the region. The company's future growth strategy is centered around the potential sales of its latest J-LTV (joint light tactical vehicle) in the region. Additionally, the domestic players in the market are increasing their product portfolio to enhance their position in the market. For instance, in September 2022, Mahindra Emirates Vehicle Armouring, Jordan, and UAE launched their Mahindra MAXIMUS 4X4 Armoured Personal Carrier for Paramilitary/ Police/Troops having B6 and B7 level bulletproof capabilities. Such factors are anticipated to help the companies increase their presence and attain profits from the region in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Main Battle Tank (MBT)

- 5.1.2 Armored Personnel Carrier (APC)

- 5.1.3 Infantry Fighting Vehicle (IFV)

- 5.1.4 Other Types

- 5.2 Country

- 5.2.1 Saudi Arabia

- 5.2.2 United Arab Emirates

- 5.2.3 Turkey

- 5.2.4 Israel

- 5.2.5 South Africa

- 5.2.6 Rest of Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Mahindra Emirates Vehicle Armouring FZ-LLC

- 6.1.2 NIMR Automotive (EDGE Group PJSC)

- 6.1.3 Streit Group

- 6.1.4 Rheinmetall AG

- 6.1.5 IAI

- 6.1.6 Oshkosh Corporation

- 6.1.7 BMC Otomotiv Ticaret ve Sanayi A.S.

- 6.1.8 BAE Systems PLC

- 6.1.9 Koc Holding A.S

- 6.1.10 Denel SOC Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS