PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1384232

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1384232

Australia Data Centre Market Size & Share Analysis - Growth Trends & Forecasts (2023 - 2028)

The Australia Data Center Market size is expected to grow from USD 5.98 billion in 2023 to USD 7.58 billion by 2028, at a CAGR of 4.86% during the forecast period (2023-2028).

The increasing demand for cloud computing among SMEs, government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data centers in the country.

Key Highlights

- Government initiatives like the Australia Government Information Management Office (AGIMO) are leading the way in optimizing data center resources with the introduction of the Australia Government Data Centre Strategy 2010-2025, and the strategy represents a transition from using government-run data centers to third-party, multi-tenant data centers.

- The data center providers are also increasingly investing or adopting an acquisition strategy to expand their capacity. For instance, Metronode's data center assets acquisition by Equinix provided the company with additional capacity to capture the benefits of scale and adds approximately 20,000 square meters of gross colocation space to Equinix's footprint in Australia.

- There has been robust development of new data centers which use renewable energies. For instance, in March 2021, 3 data centers as part of Project Koete were proposed for Western Australia and Northern Territory from the Australian company Fibre Expressway. The tier IV standard data centers with an initial capacity of 20MW each are being constructed in partnerships with wind, solar, and long-term ocean and clean hydrogen providers to satisfy 100% renewable energy access over time. Such projects propel the market's growth in Australia.

- There is a lot of concern about cybersecurity, especially when it comes to digital access and who can connect with a server and its data. Nevertheless, maintaining physical security might be quite difficult. Even in a secure environment, anyone with the necessary access can damage or utilize servers. Data centers need to be safeguarded against potential catastrophes like water leaks, fires, and cooling system failures, which are very expensive and restrict the growth of the Data Center market in the country.

- The recent COVID-19 outbreak has increased the demand for cloud computing in the country; hence, it has also expanded the scope of the data center market. The data center construction projects mostly continued as construction is classified as essential under the current Australian regime and is the vital sector to keep the country's economy running. However, the market also witnessed supply chain disruptions with the labor shortage, expecting a delay in the completion of several projects.

Australia Data Center Market Trends

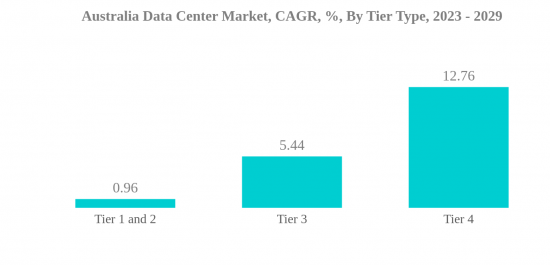

Tier 3 is the largest Tier Type

- Australia has no Tier 1 & 2 certified facilities. The Tier 3 segment of the Australian data center market reached an IT load capacity of 1,185.7 MW in 2021. It is anticipated to grow from 1,616.26 MW in 2022 to 2,615.6 MW by 2029 while recording a CAGR of 7.12%. The Tier IV data center segment reached an IT load capacity of 123 MW in 2021. The capacity is anticipated to grow from 185 MW in 2022 and reach 517 MW by 2029 while recording a CAGR of 15.81%.

- Tier 3 and 4 data centers are expected to showcase significant growth in the Australian data center market. Tier 3 data centers offer uptime of 99.98%, with N+1 redundancies, which makes them preferable for the highest number of businesses. However, providers are getting the Tier 4 certification for their new facilities. For instance, NextDC's data center in Brisbane has become the first in the country to receive a Tier 4 constructed facility certification from Uptime Institute.

Australia Data Center Industry Overview

The Australia Data Center Market is moderately consolidated, with the top five companies occupying 56.45%. The major players in this market are AirTrunk Operating Pty Ltd., Canberra Data Centers, Equinix, Inc., Global Switch Holdings Limited and Intervolve Pty Ltd. (Vintek Group) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 MARKET OUTLOOK

- 4.1 IT Load Capacity

- 4.2 Raised Floor Space

- 4.3 Colocation Revenue

- 4.4 Installed Racks

- 4.5 Rack Space Utilization

- 4.6 Submarine Cable

5 KEY INDUSTRY TRENDS

- 5.1 Smartphone Users

- 5.2 Data Traffic Per Smartphone

- 5.3 Mobile Data Speed

- 5.4 Broadband Data Speed

- 5.5 Fiber Connectivity Network

- 5.6 Regulatory Framework

- 5.7 Value Chain & Distribution Channel Analysis

6 MARKET SEGMENTATION

- 6.1 Hotspot

- 6.1.1 Melbourne

- 6.1.2 Perth

- 6.1.3 Sydney

- 6.1.4 Rest of Australia

- 6.2 Data Center Size

- 6.2.1 Large

- 6.2.2 Massive

- 6.2.3 Medium

- 6.2.4 Mega

- 6.2.5 Small

- 6.3 Tier Type

- 6.3.1 Tier 1 and 2

- 6.3.2 Tier 3

- 6.3.3 Tier 4

- 6.4 Absorption

- 6.4.1 Non-Utilized

- 6.4.2 Utilized

- 6.4.2.1 By Colocation Type

- 6.4.2.1.1 Hyperscale

- 6.4.2.1.2 Retail

- 6.4.2.1.3 Wholesale

- 6.4.2.2 By End User

- 6.4.2.2.1 BFSI

- 6.4.2.2.2 Cloud

- 6.4.2.2.3 E-Commerce

- 6.4.2.2.4 Government

- 6.4.2.2.5 Manufacturing

- 6.4.2.2.6 Media & Entertainment

- 6.4.2.2.7 Telecom

- 6.4.2.2.8 Other End User

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis

- 7.2 Company Landscape

- 7.3 Company Profiles

- 7.3.1 AirTrunk Operating Pty Ltd.

- 7.3.2 Canberra Data Centers

- 7.3.3 Digital Realty Trust, Inc.

- 7.3.4 Equinix, Inc.

- 7.3.5 Fujitsu Group

- 7.3.6 Global Switch Holdings Limited

- 7.3.7 Intervolve Pty Ltd. (Vintek Group)

- 7.3.8 Keppel DC REIT Management Pte. Ltd.

- 7.3.9 Leaseweb Global B.V.

- 7.3.10 Macquarie Telecom Group

- 7.3.11 NEXTDC Ltd

- 7.3.12 Telstra Corporation Limited

- 7.4 LIST OF COMPANIES STUDIED

8 KEY STRATEGIC QUESTIONS FOR DATA CENTER CEOS

9 APPENDIX

- 9.1 Global Overview

- 9.1.1 Overview

- 9.1.2 Porter's Five Forces Framework

- 9.1.3 Global Value Chain Analysis

- 9.1.4 Global Market Size and DROs

- 9.2 Sources & References

- 9.3 List of Tables & Figures

- 9.4 Primary Insights

- 9.5 Data Pack

- 9.6 Glossary of Terms