PUBLISHER: MTN Consulting, LLC | PRODUCT CODE: 1168240

PUBLISHER: MTN Consulting, LLC | PRODUCT CODE: 1168240

Telco Climate Goals Require Vendor Support: Supply Chain Accounts for Over Half of Typical Telco's Carbon Footprint, Tackling This is Only Way to Support a More Aggressive Path Towards a Net Zero Future

This brief report addresses the role of the supply chain in telco efforts to reduce their overall measured carbon footprint across Scopes 1 (direct energy), 2 (electricity purchases), and 3 (upstream and downstream value chain).

VISUALS

With each passing year, the outlook for climate change worsens and its impact becomes more tangible. Costs are now clearly visible as society pays more to cope with extreme heat and cold, protect against flooding, clean up after abnormal weather events, relocate populations, reinforce structures, and many other measures. Yet national governments continue to struggle to find common ground, and private, voluntary action to cope with climate change is often more about lip service than real action. The network operator sector is no exception. While there are some standouts, most operators are embarrassingly conservative in their approach to carbon footprint reductions. That's especially true for the telco sector. It's easy to focus on reducing energy consumption, as it has a direct impact on the bottom line, but investing in renewable energy is harder to support. More important, most telcos are just beginning to focus on their indirect (Scope 3) emissions, the bulk of which relate to their supply chain. The tipping point has arrived, though. Telcos need to become leaders in aggressively reducing their carbon footprints, and that will have a direct impact on how they engage with vendors. A small number of telcos already quantify the environmental performance of their suppliers within the procurement process; that will grow, and standards will become more stringent. Organizations like the Joint Audit Cooperation (JAC) will push this along. Vendors need to get ready.

COVERAGE

Companies mentioned:

|

|

Table of Contents

- Summary

- Telcos dominate power consumption within network operator business

- Scope 3 emissions overview

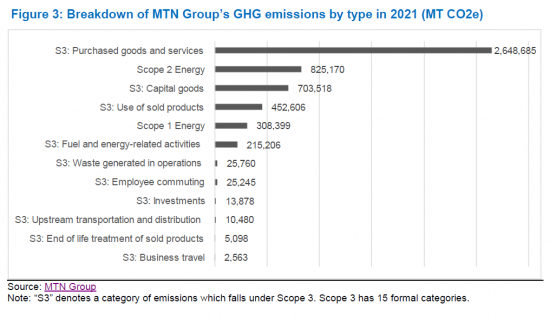

- Scope 3 examples: Swisscom and MTN Group

- Supply chain accounts for 50-80% of total emissions for many telcos

- Telcos' current climate goals and the relationship to procurement

- Implications for procurement

List of Figures and Tables

- Figure 1: Overview of GHG Protocol scopes and emissions across the value chain

- Figure 2: Breakdown of Swisscom's GHG emissions by type in 2021 (MT CO2e)

- Figure 3: Breakdown of MTN Group's GHG emissions by type in 2021 (MT CO2e)

- Figure 4: Purchased goods and services plus capital goods - total contribution to carbon footprint

- Table 1: Climate goals and procurement practices for select telcos