Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693755

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693755

North America Biopesticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 148 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

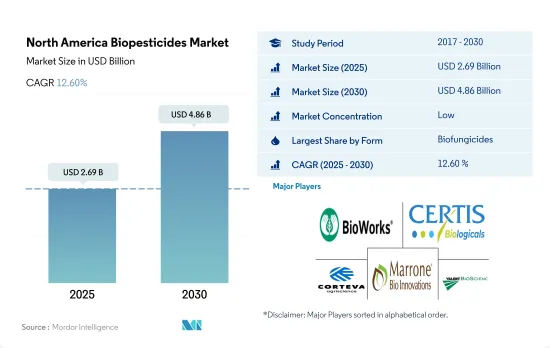

The North America Biopesticides Market size is estimated at 2.69 billion USD in 2025, and is expected to reach 4.86 billion USD by 2030, growing at a CAGR of 12.60% during the forecast period (2025-2030).

- Biofungicides are substances applied to plants to prevent diseases caused by pathogenic fungi. Biofungicides may be of microbial or botanical origin. In North America, the market for biofungicides was valued at USD 891.2 million in 2022, making them the most popular biopesticide type, with a 46.7% market share in the same year. Microbial species like Bacillus, Trichoderma, and Pseudomonas are the most available biofungicides in the market.

- The market for bioinsecticides in North America was valued at USD 565.0 million in 2022, with a share of 29.6%, making it the second most consumed biopesticide. Furthermore, the field crops with the largest area under organic agriculture accounted for 73.5% of bioinsecticide usage in 2022. Horticulture and cash crops followed with 21.4% and 5%, respectively, in the same year.

- Other biopesticides include products like nematicides, rodenticides, acaricides, and molluscicides of biological origin. These biological pesticides accounted for a share of 16.08% in 2022, occupying the third place after biofungicides and bioinsecticides.

- The market for biological herbicides was valued at USD 144.4 million in 2022, with a volume consumption of 9.9 thousand metric tons in the same year. Bioherbicides are microbes, plant extracts, or other phytotoxins used to manage weeds that compete with crops for growth by reducing weed growth or germinating weed seeds.

- The increasing awareness about the overuse of pesticides among farmers and the government initiatives to support sustainable agricultural practices and organic farming resulted in an increasing demand for biopesticides. Therefore, the market for biopesticides is anticipated to increase between 2023 and 2029.

- The North American biopesticides market is largely dominated by the United States, which accounted for 68.9% of the market value in 2022. This growth can be attributed to the country's vast organic cultivation area, which makes up 39.5% of the total organic crop area in the region. Row crops also play a significant role, which made up 50.5% of the market value in 2022.

- Canada was the second-largest biopesticides market in the region, with a market share of 23.7% in 2022. The country's organic crop farming area has been expanding, which grew from 400.0 thousand ha in 2017 to 450.0 thousand ha in 2022. This trend is expected to continue, driving growth in the agricultural plant biopesticides market.

- Mexico has the second-largest organic agricultural area in North America, with an overall organic crop area of 0.54 million ha in 2022, which is expected to increase to 0.61 million ha by 2029. This growth in organic crop areas is a key demand driver for biopesticides.

- The Rest of North America accounted for less than 1.15% of biopesticide consumption in 2022. However, the market grew by 2.9% between 2017 and 2022. It is projected to register a CAGR of 9.2% between 2023 and 2029.

- The North American biopesticides market is expected to grow faster in the United States than in other North American countries due to increased knowledge of sustainability among farmers and government measures promoting organic farming. The rising demand for organic products and sustainable agriculture practices may also drive growth in the biopesticides market in the coming years.

North America Biopesticides Market Trends

Organic produce demand grows in major countries like the United States, increasing cultivation area with government support

- The area under organic cultivation of crops in North America was recorded at 1.5 million ha in 2021, according to the data provided by FibL statistics. The area under organic cultivation in the region increased by 13.5% between 2017 and 2021. Among the North American countries, the United States is dominant, with 623.0 thousand ha of agricultural land under organic farming, with California, Maine, and New York being the major states practicing agriculture.

- The United States was followed by Mexico, with 531.1 thousand hectares of area under organic farming in 2021. Mexico is among the top 20 organic food producers in the world. Mexico is the largest exporter of organic coffee in the world, according to the Global Coffee Masters data. The country has the largest area under organic coffee production in terms of the number of organic coffee producers in the country. The major organic food-producing states in the country include Chiapas, Oaxaca, Michoacan, Chihuahua, and Guerrero, which account for 80.0% of the total organic area in the country. Organizations such as the National Association for Organic Agriculture are promoting organic agriculture in the country, which is expected to motivate more farmers to take up organic agriculture. In addition to financial assistance, the Mexican government supports research and development activities to help organic agriculture.

- Canada's area under organic crop cultivation increased from 0.4 million ha in 2017 to 0.45 million ha in 2021. Row crops occupied the maximum area with 0.42 million in 2021. The Canadian government announced a sum of USD 297,330 in 2021 as Organic Development Fund to support organic farmers. These initiatives are expected to increase the organic area in the region.

Growing demand for organic produce in domestic and international markets, rise in per capita spending on organic food

- The average per capita spending on organic food products in North America was USD 109.7 in 2021. The per capita spending in the United States is the highest among the North American countries, with average spending of USD 186.7 in 2021. The sales of organic products in the United States crossed USD 63.00 billion in 2021, according to the Organic Tarde Association, with a 2.0% increase over the previous year, with organic food sales standing at USD 57.5 billion in 2021. Organic fruits and vegetables accounted for 15.0% of the total organic product sales, with a value of USD 21.0 billion in 2021.

- Organic food sales in Canada reached a value of USD 8.10 billion in 2020, as per the data reported by the Organic Federation of Canada. It is reported that Canada is the sixth-largest market in the world for organic products, with the supply of organic products failing to keep up with the demand in the country. The average spending on organic food per person was USD 142.6 in 2021. Increasing government support to retailers is expected to increase the availability, accessibility, and affordability of organic products in the country. The Organic Tarde Association estimates that the organic products market in Canada is expected to register a CAGR of 6.3% between 2021 and 2026.

- In 2021, Mexico registered a market size of USD 63.0 million for organic products with a global rank of 35. According to the Organic Trade Association, it is estimated to register a CAGR of 7.2% between 2021 and 2026. However, the per capita spending on organic products in the country is less compared to other countries in the region, accounting for a value of USD 0.49 in 2021. More players entering the market in Mexico are expected to increase the demand for organic products in the country.

North America Biopesticides Industry Overview

The North America Biopesticides Market is fragmented, with the top five companies occupying 6.36%. The major players in this market are Bioworks Inc., Certis U.S.A. LLC, Corteva Agriscience, Marrone Bio Innovations Inc. and Valent Biosciences LLC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 500015

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Biofungicides

- 5.1.2 Bioherbicides

- 5.1.3 Bioinsecticides

- 5.1.4 Other Biopesticides

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 AEF Global Biopesticides

- 6.4.2 Andermatt Group AG

- 6.4.3 BIOQUALITUM SA de CV

- 6.4.4 Bioworks Inc.

- 6.4.5 Certis U.S.A. LLC

- 6.4.6 Corteva Agriscience

- 6.4.7 Lallemand Inc.

- 6.4.8 Marrone Bio Innovations Inc.

- 6.4.9 Terramera Inc.

- 6.4.10 Valent Biosciences LLC

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.