Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692494

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692494

Video Encoder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 157 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

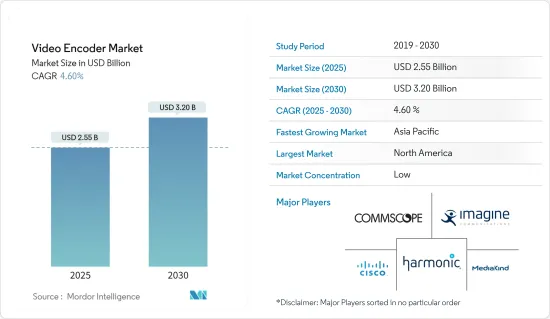

The Video Encoder Market size is estimated at USD 2.55 billion in 2025, and is expected to reach USD 3.20 billion by 2030, at a CAGR of 4.6% during the forecast period (2025-2030).

Key Highlights

- The video encoder market is witnessing strong growth, driven by the rising demand for high-quality video streaming and broadcasting across various platforms. Video encoders convert video signals into digital formats suitable for transmission over the Internet or other networks. This market's expansion is fueled by the increasing consumption of online video content, the proliferation of over-the-top (OTT) services, and the surge in live-streaming activities. The widespread adoption of social media platforms, where video content is a key engagement tool, further propels the demand for advanced video encoding solutions.

- Technological advancements are pivotal in shaping the video encoder market. Innovations in compression algorithms, such as H.265 (HEVC) and the emerging AV1 codec, enhance compression rates while maintaining video quality, facilitating efficient data transmission and storage. These advancements support the increasing demand for 4K and 8K video resolutions, which require significantly more bandwidth and storage capacity.

- Additionally, the development of hardware encoders that integrate artificial intelligence (AI) and machine learning (ML) represents a significant trend. These integrations improve real-time video processing capabilities and optimize network resources.

- Moreover, major players such as Cisco Systems Inc., Harmonic Inc., and Axis Communications AB (Canon Inc.) lead the pack in the video encoder market. Alongside these industry stalwarts, newer firms are making waves with innovative solutions. These players are actively pursuing strategies like mergers, acquisitions, partnerships, and product launches to bolster their market positions. Notably, many are forging strategic ties with OTT service providers and broadcasters, seeking to tap into synergies and broaden their customer reach.

- The video encoder market exhibits a highly promising outlook with significant growth opportunities. The ongoing evolution of video standards, the global deployment of 5G networks, and the increasing demand for immersive experiences, such as virtual reality (VR) and augmented reality (AR), are set to drive further innovations and applications. Companies prioritizing research and development and swiftly adapting to technological shifts will be well-positioned to capitalize on emerging trends and maintain their competitive advantage.

- While the video encoder market boasts numerous growth drivers, a notable hurdle emerges in the form of the steep initial costs associated with hardware video encoders. These devices, pivotal for transforming raw video into digital formats for broadcasting and streaming, often demand a significant upfront investment. This financial outlay can pose a formidable obstacle, especially for smaller enterprises and startups. The resulting high costs may dissuade potential customers from embracing new technologies or modernizing their existing setups, constraining market expansion and stifling innovation. Moreover, these expenses can directly impact a company's overall return on investment, underscoring the importance for manufacturers to explore cost-cutting measures or offer flexible financing options to spur wider adoption.

Video Encoder Market Trends

Increasing Popularity of Video Streaming Platforms is Expected to Drive the Market Growth

- The rising popularity of video streaming services such as Netflix, Amazon Prime, and YouTube has heightened the appetite for high-quality, low-latency streaming. Consequently, this trend drives the demand for advanced video encoders. These encoders are tasked with compressing videos efficiently, maintaining quality, and guaranteeing seamless viewing, especially at resolutions as demanding as 4K and 8K. According to Inplayer, among OTT users, 18.4% fall in the 25 - 29 age bracket, with 11.5% in the 30 - 36 range. Notably, approximately 15% of OTT users are under 17 years old.

- The rise of user-generated and professional content has led to a boom in video production for streaming. Consequently, there is a growing demand for efficient video encoding solutions. These solutions are crucial for increasing content volume, ensuring swift uploads, and seamless streaming experiences. This trend serves as a significant driver of the video encoder market.

- Moreover, the surge in live streaming across events, gaming, sports, and social media has heightened the need for real-time video encoding solutions, driving the video encoder market. Encoders that can process live content swiftly, ensuring minimal delays, are pivotal for delivering a smooth and engaging viewer experience.

- Also, the surge in smartphone, tablet, and smart TV usage for video streaming has underscored the necessity for adaptive video encoding. Encoders, pivotal for tailoring videos to diverse screen sizes and network speeds, are driving the video encoder market.

Asia-Pacific is Expected to Hold the Largest Market Share

- The advent of terrestrial digital television broadcasting in China has improved existing services and paved the way for new applications. The DTT broadcast standard enables wide-area fixed reception on HDTV and multiple SDTV programs. New services also include mobile, wearable, and high-speed applications.

- The Chinese government is also working to improve people's viewing experience, and China encouraged major cities to start offering free terrestrial HDTV broadcast content. This helps drive growth in the digital terrestrial market and the HDTV industry as a whole, including high-definition flat panels, chipsets, transmitters, software, and content creation.

- Investments by OTT services like Netflix, Amazon, and Disney+ Hotstar in original and acquired content will enable subscription video-on-demand to make up 93% of the total OTT revenue, increasing to 30.7% by 2024, amounting to USD 2.7 billion in India. By January 2024, YouTube emerged as the leading video platform in India, attracting 462 million users, significantly outpacing the United States in viewership.

- South Korean organizations are developing video encoder solutions to drive the broadcasting and streaming market. For example, KT Corp. is driving the pay TV services industry in South Korea regarding subscriptions and supervision, owing to its monopoly in the DTH segment and strong position in the IPTV segment, where it has the greatest share.

- In recent years, technological advances have led to the rapid spread of devices such as cameras, displays, and tablets that can record and display 4K video in higher resolution than high-definition televisions (HDTVs). With the proliferation of these devices, expectations are rising for next-generation video encoding for delivering HD video over broadcast and network delivery in Japan. 4K TVs are becoming increasingly popular in the home, and many models are available from major TV manufacturers.

Video Encoder Industry Overview

The video encoder market is highly competitive, with major players like Harmonic Inc., CommScope Holding Company Inc., and MediaKind continuously enhancing their capabilities to maintain a competitive edge. These companies strategically focus on product innovations, mergers, acquisitions, and partnerships to diversify their product portfolios and expand their global footprint.

- In January 2024, Arcturus, a key player in volumetric video technology, unveiled an update for its HoloSuite toolset. This update introduces a novel approach, enabling the seamless delivery of lightweight, scalable volumetric video to game engines. Arcturus empowers not just virtual production teams but also game developers. Users can now enrich their digital landscapes with more volumetric characters without compromising on data quality.

- In November 2023, MainConcept, a video and audio codec technology specialist, announced the release of the latest version of its real-time encoding application for OTT and TV broadcasting workflows. The new version, Live Encoder 3.4, supports VVC/H.266 and MPEG-5 LCEVC codecs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 91670

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Analysis of Video Codecs and Their Evolution

- 4.3 List of VVC-approved and Incorporated Companies

- 4.4 List of Companies Contributing to the VVC Standard

- 4.5 Impact of COVID-19 on the Market

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Popularity of Video Streaming Platforms

- 5.1.2 Easy Integration of Hardware Encoders with Video Cameras

- 5.1.3 Cloud Video Encoding Technology to Drive the Demand

- 5.2 Market Challenges

- 5.2.1 High Initial Cost of Hardware Video Encoder

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Pay TV

- 6.1.1.1 Cable Video Encoder

- 6.1.1.2 Satellite Video Encoder

- 6.1.1.3 IPTV Video Encoder

- 6.1.2 Broadcast and Digital Terrestrial Television (DTT)

- 6.1.2.1 Contribution Video Encoder

- 6.1.2.2 Backhaul and Distribution Video Encoder

- 6.1.2.3 DTT Video Encoder

- 6.1.3 Security and Surveillance

- 6.1.1 Pay TV

- 6.2 By Geography

- 6.2.1 Americas

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.1.3 Brazil

- 6.2.1.4 Mexico

- 6.2.1.5 Rest of the Americas

- 6.2.2 Europe

- 6.2.2.1 Germany

- 6.2.2.2 United Kingdom

- 6.2.2.3 France

- 6.2.2.4 Russia

- 6.2.2.5 Poland

- 6.2.2.6 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 South Korea

- 6.2.3.4 Japan

- 6.2.3.5 Rest of Asia-Pacific

- 6.2.4 Middle East and Africa

- 6.2.4.1 Turkey

- 6.2.4.2 Israel

- 6.2.4.3 United Arab Emirates

- 6.2.4.4 Saudi Arabia

- 6.2.4.5 South Africa

- 6.2.4.6 Rest of Middle East and Africa

- 6.2.1 Americas

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Harmonic Inc.

- 7.1.2 Commscope Holding Company Inc.

- 7.1.3 MediaKind

- 7.1.4 Cisco Systems Inc.

- 7.1.5 Imagine Communications

- 7.1.6 Z3 Technology

- 7.1.7 ATEME

- 7.1.8 Adtec Digital

- 7.1.9 Telairity (VITEC)

- 7.1.10 Axis Communications AB (Canon Inc.)

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.