PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444643

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444643

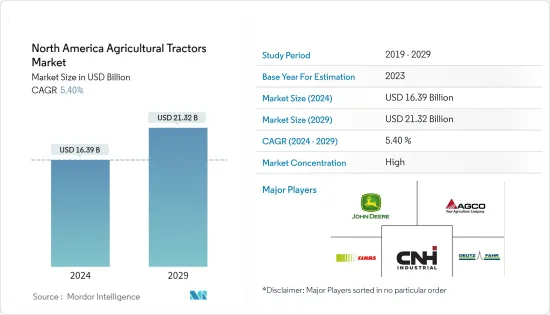

North America Agricultural Tractors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The North America Agricultural Tractors Market size is estimated at USD 16.39 billion in 2024, and is expected to reach USD 21.32 billion by 2029, growing at a CAGR of 5.40% during the forecast period (2024-2029).

Key Highlights

- With changing industry trends and the development of more sophisticated agricultural machinery, farming methods have taken a giant leap forward. Farm mechanization increased productivity, improved the quality of the product, and reduced the hazards of operations. However, with developing technology in the future, driverless tractors, which use GPS maps and electronic sensors, may come into play. The United States and Canada are the major markets in the region due to large farm sizes and the adoption of high mechanization.

- Farm mechanization saves time and labor, cuts down crop production costs in the long run, reduces post-harvest losses, and boosts crop output and farm income. Larger farms and awareness among farmers lead to the quick adoption of modern technologies in developed countries compared to developing nations. This factor makes North America the largest market for tractor technologies.

- The increasing benefits of tractors and food security concerns across the world are paving the way for the agricultural tractor market. The increasing focus on research, innovations, and partnerships to develop advanced technologies by key market players leads to the market's growth in the region.

North America Agricultural Tractors Market Trends

Increasing Adoption of Farm Mechanization and Shortage of Labor

With the development of more sophisticated agricultural machinery, farming methods have changed. Increased farm consolidation, a large production base, and greater government support through subsidies drive the adoption of agricultural tractor machinery.

Farmers in most markets in North America are increasingly adopting advanced technology, such as precision farming systems and GPS-controlled agricultural machinery. The North American market is driven by the sales of higher engine-power tractors, with tractors of power more than 40 HP contributing a major market share. Alongside, major players, like Deere & Company, AGCO Corp., and CNH Industrial NV, are focusing on manufacturing agricultural tractors with advanced technology, which drives the market during the forecast period.

The United States has been witnessing an acute shortage of farm laborers. A survey by the California Farm Bureau revealed that more than 40% of the farmers faced a consistent labor shortage in various farm operations in the state in the past five years. It led to an increased adoption rate of modern technologies such as tractors to ensure better management of farm resources. According to the World Bank's database, the employment in agriculture out of the total employment fell drastically and reached 1.36% in 2019.

Increasing Cost of Labor Paves Way for Agricultural Tractors

Farming has traditionally been a highly-labor intensive method in agriculture. However, the continually rising real wage of farm labor positively impacted the demand for tractors in the region, as farmers are increasingly adopting agricultural mechanization, including tractors, as a substitute for manual labor. According to the USDA reports, the annual average gross hourly wage for field and livestock workers was USD 16.62 in 2022. This was a 7% increase over last year's annual average of USD 15.56 per hour, further increasing the demand for tractors in the country.

According to the Canadian Agriculture Human Resource Council, Canada's farm labor deficit is expected to double by 2029 to 123,000 workers, or one in three jobs, as shortages continue to hit the sector's bottom line. The rapid shrinkage of farm labor has boosted the tractor market, thus driving the demand for tractors in the region.

According to the International Labor Organization, around 25% of human resources engaged in agriculture were skilled in the United States, which has decreased over the years. As technologically assisted agriculture needs skilled laborers that are in an acute shortage, farmers are adopting technologies such as tractors that can be productive, considering the current challenge.

North America Agricultural Tractors Industry Overview

The North American agricultural tractor machinery market is consolidated, with few players dominating the market. CNH Industrial NV, Deere & Company, AGCO Corp., Same Deutz-Fahr Deutschland GmbH, and Claas KGaA mbH are some of the major players operating in the market. The companies focus on strengthening their base by offering enhanced product features, competitive pricing, enhanced quality, increased scale of operation, and technological innovation. Along with innovations and expansions, investments in R&D and developing novel product portfolios will likely be crucial strategies in the coming years. These companies are making strategic partnerships with domestic companies to expand their distribution networks and launch new innovative tractors that cater to the needs of the farmers in this region.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Below 40 HP

- 5.1.2 40-100 HP

- 5.1.3 Above 100 HP

- 5.1.4 4 WD Farm Tractors

- 5.2 Geography

- 5.2.1 United States

- 5.2.2 Canada

- 5.2.3 Mexico

- 5.2.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Deere and Company

- 6.3.2 AGCO Corp.

- 6.3.3 Claas KGaA mbH

- 6.3.4 CNH Industrial NV

- 6.3.5 Same Deutz-Fahr Deutschland GmbH

- 6.3.6 Kubota Corporation

- 6.3.7 Mahindra & Mahindra Ltd

- 6.3.8 Escorts Limited

- 6.3.9 Tractors and Farm Equipment Ltd

- 6.3.10 Kverneland Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS