PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1719513

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1719513

Global Multirole Helicopter Simulation Market 2025-2035

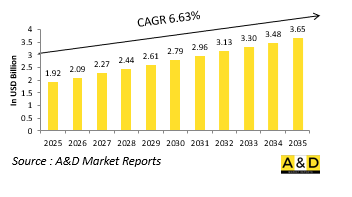

The global Multirole Helicopter Simulation market is estimated at USD 1.92 billion in 2025, projected to grow to USD 3.65 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 6.63% over the forecast period 2025-2035.

Introduction to Global Multirole Helicopter Simulation market:

Multirole helicopter simulation has become an essential component of modern defense and aviation training. As armed forces and civil operators seek to improve mission readiness, safety, and cost-efficiency, simulation platforms offer a highly realistic and risk-free environment to train pilots and crew members for a variety of complex missions. These simulations replicate the operational versatility of multirole helicopters, which are used in a wide range of roles such as transport, reconnaissance, search and rescue, maritime operations, and combat support. The global landscape for these systems reflects growing recognition of simulation's value in both initial training and mission rehearsal. As helicopters become more technologically advanced and mission profiles more complex, simulation serves not only as a training aid but as a tool for adapting to evolving operational demands. Industry stakeholders, including defense agencies, aerospace manufacturers, and training organizations, are increasingly investing in this area to support long-term capability development. The global market for multirole helicopter simulation continues to evolve, shaped by strategic priorities, innovation in training methodologies, and the need to reduce real-world operational risk while maintaining a high standard of preparedness.

Technology Impact in Multirole Helicopter Simulation Market:

Technological advancements are profoundly transforming the field of multirole helicopter simulation. With the integration of immersive technologies such as high-fidelity visual systems, advanced physics engines, and artificial intelligence-driven behavior modeling, simulators now offer levels of realism that closely replicate actual flight conditions. These innovations enable pilots to experience authentic scenarios, including adverse weather, complex terrains, and dynamic mission environments, enhancing both skill acquisition and decision-making capabilities. Interoperability has also become a critical feature, allowing simulators to connect with other training systems for joint and combined mission exercises. Virtual and augmented reality are further pushing the boundaries of what can be simulated, offering portable and scalable training solutions that can supplement or replace full-flight simulators in certain contexts. The inclusion of machine learning enables adaptive training systems that tailor scenarios to individual performance, accelerating learning curves. Moreover, cybersecurity enhancements ensure that simulation platforms remain protected from interference, a growing concern as more systems become networked. Overall, technology is not only enhancing training effectiveness but also enabling more flexible, cost-efficient deployment of simulation capabilities in both centralized training centers and forward-operating environments.

Key Drivers in Multirole Helicopter Simulation Market:

Several key factors are propelling the growth and importance of multirole helicopter simulation globally. First and foremost is the operational necessity for mission-ready aircrews who can perform under a wide range of conditions and mission types. As multirole helicopters are deployed in increasingly diverse scenarios, training systems must keep pace with these evolving demands. Safety considerations are another critical driver. Simulation allows crews to practice emergency procedures, combat scenarios, and complex maneuvers without putting lives or equipment at risk. Budget constraints also play a role, as simulation offers a cost-effective alternative to in-air training, significantly reducing wear on equipment and overall operational expense. Environmental and logistical limitations further underscore the value of simulation, allowing training to continue uninterrupted by weather, location constraints, or equipment availability. Additionally, the fast pace of technological change in rotorcraft platforms demands constant retraining and system familiarization, which simulation provides efficiently. Strategic priorities among defense organizations to modernize training capabilities and align with evolving mission profiles also drive adoption. Lastly, the need for multinational interoperability and coordinated training exercises supports the development of simulation systems capable of integrating across allied forces and joint service environments.

Regional Trends in Multirole Helicopter Simulation Market:

Regional dynamics play a significant role in shaping the multirole helicopter simulation landscape. In North America, a mature defense training infrastructure supports extensive use of advanced simulators, with a strong emphasis on integration with broader joint force training systems. Defense modernization programs continue to prioritize simulation to maintain strategic readiness. In Europe, increased geopolitical tensions and a focus on joint operations within NATO are driving demand for highly interoperable and standardized simulation platforms. The emphasis is on cross-border training capabilities and mission rehearsal for hybrid warfare scenarios. In the Asia-Pacific region, rising defense budgets and ongoing territorial disputes are prompting several nations to enhance rotary-wing capabilities, including simulation training to support expanding helicopter fleets. Regional investments are also aimed at developing domestic training and simulation industries to reduce reliance on foreign systems. In the Middle East, security threats and the use of helicopters in both military and humanitarian roles have led to increased interest in simulation as a way to build skill and resilience without expending limited aircraft resources. Across Latin America and Africa, simulation adoption is slower but gaining momentum as part of broader defense and aviation modernization strategies, often supported through international partnerships and training programs.

Key Multirole Helicopter Simulation Program:

To preserve its leadership in assault-utility rotorcraft, the U.S. Army is positioning the launch of the Future Long-Range Assault Aircraft (FLRAA) as a central element of its Future Vertical Lift (FVL) initiative. This program aims to develop a next-generation fleet of advanced aircraft that will equip the military with the capabilities needed to deter threats, engage in combat, and achieve victory in future conflicts. FLRAA is set to replace the iconic UH-60 Black Hawk, which has long served as the backbone of the tactical utility helicopter fleet across the U.S. Army, Air Force, Navy, Coast Guard, and several allied nations. Since its introduction in 1979, the Black Hawk has been a critical asset in operations across Afghanistan, Iraq, and other global theaters. Over more than four decades, the helicopter has undergone numerous upgrades-spearheaded by Sikorsky and key partners like Honeywell-to ensure it remains effective and relevant in modern combat environments, despite its origins during the Cold War.

Table of Contents

Global multirole helicopter simulation market in defense- Table of Contents

Global multirole helicopter simulation market in defense Report Definition

Global multirole helicopter simulation market in defense Segmentation

By Region

By Technology

By Type of simulation

By Component

Global multirole helicopter simulation market in defense Analysis for next 10 Years

The 10-year Global multirole helicopter simulation market in defense analysis would give a detailed overview of Global multirole helicopter simulation market in defense growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Global multirole helicopter simulation market in defense

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global multirole helicopter simulation market in defense Forecast

The 10-year Global multirole helicopter simulation market in defense forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Global multirole helicopter simulation market in defense Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Global multirole helicopter simulation market in defense

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Global multirole helicopter simulation market in defense

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Global multirole helicopter simulation market in defense

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Technology, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Type of Simulation, 2025-2035

- Table 20: Scenario Analysis, Scenario 1, By Component, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Technology, 2025-2035

- Table 23: Scenario Analysis, Scenario 2, By Type of Simulation, 2025-2035

- Table 24: Scenario Analysis, Scenario 2, By Component, 2025-2035

List of Figures

- Figure 1: Global Multirole Helicopter Simulation Market Forecast, 2025-2035

- Figure 2: Global Multirole Helicopter Simulation Market Forecast, By Region, 2025-2035

- Figure 3: Global Multirole Helicopter Simulation Market Forecast, By Technology, 2025-2035

- Figure 4: Global Multirole Helicopter Simulation Market Forecast, By Type of Simulation, 2025-2035

- Figure 5: Global Multirole Helicopter Simulation Market Forecast, By Component, 2025-2035

- Figure 6: North America, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 7: Europe, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 8: Middle East, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 9: APAC, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 10: South America, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 11: United States, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 12: United States, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 13: Canada, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 14: Canada, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 15: Italy, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 16: Italy, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 17: France, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 18: France, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 19: Germany, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 20: Germany, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 21: Netherlands, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 22: Netherlands, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 23: Belgium, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 24: Belgium, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 25: Spain, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 26: Spain, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 27: Sweden, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 28: Sweden, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 29: Brazil, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 30: Brazil, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 31: Australia, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 32: Australia, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 33: India, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 34: India, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 35: China, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 36: China, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 37: Saudi Arabia, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 38: Saudi Arabia, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 39: South Korea, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 40: South Korea, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 41: Japan, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 42: Japan, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 43: Malaysia, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 44: Malaysia, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 45: Singapore, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 46: Singapore, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 47: United Kingdom, Multirole Helicopter Simulation Market, Technology Maturation, 2025-2035

- Figure 48: United Kingdom, Multirole Helicopter Simulation Market, Market Forecast, 2025-2035

- Figure 49: Opportunity Analysis, Multirole Helicopter Simulation Market, By Region (Cumulative Market), 2025-2035

- Figure 50: Opportunity Analysis, Multirole Helicopter Simulation Market, By Region (CAGR), 2025-2035

- Figure 51: Opportunity Analysis, Multirole Helicopter Simulation Market, By Technology (Cumulative Market), 2025-2035

- Figure 52: Opportunity Analysis, Multirole Helicopter Simulation Market, By Technology (CAGR), 2025-2035

- Figure 53: Opportunity Analysis, Multirole Helicopter Simulation Market, By Type of Simulation (Cumulative Market), 2025-2035

- Figure 54: Opportunity Analysis, Multirole Helicopter Simulation Market, By Type of Simulation (CAGR), 2025-2035

- Figure 55: Opportunity Analysis, Multirole Helicopter Simulation Market, By Component (Cumulative Market), 2025-2035

- Figure 56: Opportunity Analysis, Multirole Helicopter Simulation Market, By Component (CAGR), 2025-2035

- Figure 57: Scenario Analysis, Multirole Helicopter Simulation Market, Cumulative Market, 2025-2035

- Figure 58: Scenario Analysis, Multirole Helicopter Simulation Market, Global Market, 2025-2035

- Figure 59: Scenario 1, Multirole Helicopter Simulation Market, Total Market, 2025-2035

- Figure 60: Scenario 1, Multirole Helicopter Simulation Market, By Region, 2025-2035

- Figure 61: Scenario 1, Multirole Helicopter Simulation Market, By Technology, 2025-2035

- Figure 62: Scenario 1, Multirole Helicopter Simulation Market, By Type of Simulation, 2025-2035

- Figure 63: Scenario 1, Multirole Helicopter Simulation Market, By Component, 2025-2035

- Figure 64: Scenario 2, Multirole Helicopter Simulation Market, Total Market, 2025-2035

- Figure 65: Scenario 2, Multirole Helicopter Simulation Market, By Region, 2025-2035

- Figure 66: Scenario 2, Multirole Helicopter Simulation Market, By Technology, 2025-2035

- Figure 67: Scenario 2, Multirole Helicopter Simulation Market, By Type of Simulation, 2025-2035

- Figure 68: Scenario 2, Multirole Helicopter Simulation Market, By Component, 2025-2035

- Figure 69: Company Benchmark, Multirole Helicopter Simulation Market, 2025-2035