PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1811811

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1811811

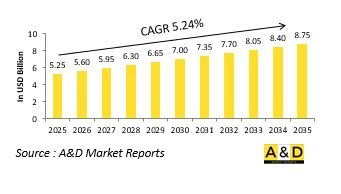

Global SONAR Systems Market 2025 - 2035

The Global SONAR Systems market is estimated at USD 5.25 billion in 2025, projected to grow to USD 8.75 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 5.24% over the forecast period 2025-2035.

Introduction to SONAR Systems Market:

Defense SONAR (Sound Navigation and Ranging) systems are vital tools for maritime situational awareness, playing a central role in underwater surveillance, navigation, and threat detection. These systems function by emitting sound pulses and interpreting the returning echoes to identify, locate, and track objects beneath the surface. In the defense sector, SONAR is used extensively for anti-submarine warfare, mine detection, and the protection of strategic naval assets. The strategic importance of underwater dominance has made SONAR systems indispensable for modern navies, especially as underwater threats become more sophisticated and harder to detect through conventional means. Defense SONAR systems are deployed on a variety of platforms, including submarines, surface vessels, unmanned underwater vehicles, and fixed ocean installations. They are often integrated with broader naval command and control frameworks to enhance maritime domain awareness. As underwater warfare tactics evolve, so too does the requirement for more sensitive, adaptable, and stealth-resistant detection technologies. Around the world, military planners are increasingly recognizing the need for robust underwater monitoring solutions, making defense SONAR systems a critical component of naval readiness. This global emphasis on underwater security reflects the strategic imperative to monitor littoral zones, secure chokepoints, and protect Surveillance Radar lines and national maritime interests.

Technology Impact in SONAR Systems Market:

Advancements in technology have significantly transformed the capabilities of defense SONAR systems, leading to enhanced detection accuracy, greater operational range, and improved threat classification. Digital signal processing has allowed modern SONAR systems to filter background noise, distinguish between objects with similar acoustic profiles, and provide clearer imagery of the underwater environment. The integration of artificial intelligence and machine learning enables real-time interpretation of acoustic data, allowing operators to quickly identify and categorize underwater threats. Improvements in materials science have contributed to the development of more compact and lightweight transducers, making it easier to deploy SONAR on a broader range of platforms, including unmanned systems. Low-frequency active SONAR systems have expanded detection range capabilities, while high-frequency systems offer detailed resolution for mine and obstacle detection. Additionally, the use of synthetic aperture SONAR has enabled the creation of high-resolution seabed maps, supporting navigation and mission planning in complex environments. Networking technologies have also made it possible for SONAR data to be shared across multiple vessels and command centers, creating a more unified and informed maritime picture. These innovations have collectively elevated SONAR from a tactical tool to a strategic asset in defense planning, enabling navies to respond more effectively to evolving underwater threats.

Key Drivers in SONAR Systems Market:

Several strategic and operational factors are driving the increased focus on defense SONAR systems across global military forces. Rising underwater threats, including the proliferation of advanced submarines and naval mines, are pushing defense agencies to invest in more capable detection and tracking technologies. Territorial disputes and maritime boundary enforcement needs are also prompting countries to bolster their underwater surveillance capabilities. The expansion of undersea infrastructure such as pipelines and communication cables has made it essential to monitor subsea activity more closely, further elevating the importance of SONAR systems. Naval modernization programs are incorporating advanced sensor suites as standard features on new platforms, positioning SONAR as a key enabler of future maritime operations. There is also growing demand for systems that can operate in littoral environments where acoustic conditions are more challenging. The increasing use of unmanned and autonomous systems in naval missions is influencing the development of compact, energy-efficient SONAR units designed for remote or extended deployments. In addition, interoperability between allied navies is encouraging the adoption of standardized acoustic technologies. All these factors contribute to making defense SONAR systems a critical area of investment for maintaining underwater situational awareness and ensuring maritime dominance in both peacetime and conflict scenarios.

Regional Trends in SONAR Systems Market:

Regional trends in defense SONAR system development and deployment reflect the specific security concerns, maritime geography, and strategic objectives of different areas. In North America, particularly within the United States, there is a strong emphasis on enhancing undersea warfare capabilities through investment in multi-frequency SONAR systems, to support both open-ocean operations and complex littoral missions. European nations are focusing on modernizing legacy fleets with quieter, more energy-efficient SONAR solutions that can seamlessly integrate with NATO's collective maritime defense infrastructure. The emphasis in this region often lies in balancing performance with compliance to environmental standards, particularly in sensitive marine ecosystems. In the Asia-Pacific, growing maritime tensions and rapid naval expansion are driving countries to develop indigenous SONAR technologies suited for archipelagic and deep-sea environments. Regional powers are also emphasizing the use of SONAR in conjunction with unmanned platforms to extend surveillance coverage. The Middle East is increasingly interested in protecting key maritime trade routes and offshore infrastructure, leading to an uptick in fixed and mobile SONAR installations for both defensive and monitoring purposes. Meanwhile, countries in Africa and Latin America are gradually adopting portable and scalable SONAR systems, often through international cooperation, to improve maritime domain awareness in coastal and exclusive economic zones.

Key Defense SONAR Systems Program:

Lockheed Martin Corporation's (LMT) Rotary and Mission Systems division has secured a contract modification from the Naval Sea Systems Command, Washington, D.C., to deliver engineering design, development, and production support for Sound Navigation and Ranging (Sonar) systems. The contract, valued at $197.5 million, is scheduled for completion by September 2026, with most of the work to be carried out in Manassas, VA, and Clearwater, FL. Growing geopolitical tensions in recent years have driven governments worldwide to boost defense investments, particularly in sonar technologies, to meet the rising need for advanced seabed mapping, improved underwater surveillance, and deployment of next-generation sonar-equipped vessels.

Table of Contents

SONAR Systems Market Report Definition

SONAR Systems Market Segmentation

By Platform

By Region

By Application

SONAR Systems Market Analysis for next 10 Years

The 10-year SONAR systems market analysis would give a detailed overview of SONAR systems market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of SONAR Systems Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global SONAR Systems Market Forecast

The 10-year SONAR systems market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional SONAR Systems Market Trends & Forecast

The regional SONAR systems market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of SONAR Systems Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for SONAR Systems Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on SONAR Systems Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Application, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Application, 2025-2035

List of Figures

- Figure 1: Global SONAR Systems Market Forecast, 2025-2035

- Figure 2: Global SONAR Systems Market Forecast, By Region, 2025-2035

- Figure 3: Global SONAR Systems Market Forecast, By Platform, 2025-2035

- Figure 4: Global SONAR Systems Market Forecast, By Application, 2025-2035

- Figure 5: North America, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 6: Europe, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 7: Middle East, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 8: APAC, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 9: South America, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 10: United States, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 11: United States, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 12: Canada, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 13: Canada, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 14: Italy, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 15: Italy, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 16: France, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 17: France, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 18: Germany, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 19: Germany, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 22: Belgium, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 24: Spain, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 25: Spain, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 26: Sweden, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 28: Brazil, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 30: Australia, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 31: Australia, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 32: India, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 33: India, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 34: China, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 35: China, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 38: South Korea, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 40: Japan, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 41: Japan, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 44: Singapore, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, SONAR Systems Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, SONAR Systems Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, SONAR Systems Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, SONAR Systems Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, SONAR Systems Market, By Platform (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, SONAR Systems Market, By Platform (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, SONAR Systems Market, By Application (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, SONAR Systems Market, By Application (CAGR), 2025-2035

- Figure 54: Scenario Analysis, SONAR Systems Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, SONAR Systems Market, Global Market, 2025-2035

- Figure 56: Scenario 1, SONAR Systems Market, Total Market, 2025-2035

- Figure 57: Scenario 1, SONAR Systems Market, By Region, 2025-2035

- Figure 58: Scenario 1, SONAR Systems Market, By Platform, 2025-2035

- Figure 59: Scenario 1, SONAR Systems Market, By Application, 2025-2035

- Figure 60: Scenario 2, SONAR Systems Market, Total Market, 2025-2035

- Figure 61: Scenario 2, SONAR Systems Market, By Region, 2025-2035

- Figure 62: Scenario 2, SONAR Systems Market, By Platform, 2025-2035

- Figure 63: Scenario 2, SONAR Systems Market, By Application, 2025-2035

- Figure 64: Company Benchmark, SONAR Systems Market, 2025-2035