PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1811813

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1811813

Global Special Purpose Land Vehicles Market 2025 - 2035

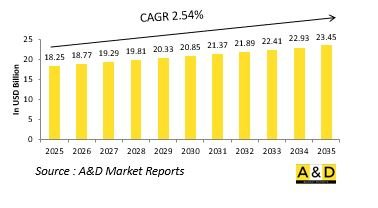

The Global Special Purpose Land Vehicles market is estimated at USD 18.25 billion in 2025, projected to grow to USD 23.45 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 2.54% over the forecast period 2025-2035.

Introduction to Special Purpose Land Vehicles Market:

Defense special purpose land vehicles form a vital segment of the global defense industry, built to serve missions that standard military platforms cannot address effectively. These vehicles are engineered with specific functions in mind, ranging from tactical mobility and reconnaissance to command, engineering support, and recovery operations. Their primary strength lies in their ability to adapt to diverse terrains and mission requirements, making them essential in both combat and support roles. Unlike conventional armored or transport vehicles, they are tailored with specialized systems, equipment, and structural modifications that enhance their suitability for complex environments. The market is shaped by the evolving nature of warfare and security needs. Modern conflicts demand not only protection and firepower but also rapid adaptability, logistical efficiency, and mission-specific performance. As a result, the design and procurement of such vehicles emphasize modularity, survivability, and integration with broader operational networks. They serve as the ground-level backbone that supports troops, ensures supply chains, and enables force mobility in challenging scenarios. Whether deployed for active combat, humanitarian assistance, or infrastructure repair in conflict zones, defense special purpose land vehicles play a crucial role in ensuring that armed forces remain capable, resilient, and operationally versatile.

Technology Impact in Special Purpose Land Vehicles Market:

The role of technology in shaping defense special mission aircraft has become increasingly pronounced, driving both capability enhancement and mission effectiveness. Advanced technologies are transforming these platforms into highly networked assets that operate at the intersection of intelligence gathering, surveillance, electronic warfare, and communication support. The integration of modern sensor suites provides the ability to detect, track, and analyze activity across multiple domains with unprecedented accuracy. These improvements allow forces to maintain situational awareness even in complex and contested environments. Digitalization is a central theme, enabling real-time information sharing and interoperability with ground, naval, and space assets. Aircraft now act as flying command centers, transmitting critical intelligence instantly to decision-makers and frontline units. Emerging technologies such as artificial intelligence and machine learning are further optimizing mission planning and execution by offering predictive insights and automating aspects of threat detection. Materials science and propulsion innovations have also played a role, allowing for extended endurance and improved efficiency. In addition, electronic warfare and cybersecurity measures are ensuring that these aircraft remain effective in highly competitive theaters where adversaries may attempt to disrupt communications or sensor performance. Collectively, these advancements highlight technology's decisive impact on the evolution of special mission aircraft.

Key Drivers in Special Purpose Land Vehicles Market:

The demand for defense special purpose land vehicles is shaped by a combination of security imperatives, operational requirements, and technological opportunities. A key factor driving growth is the changing nature of threats, where forces must be prepared for both conventional battles and irregular warfare scenarios. Special purpose vehicles provide the tailored capabilities needed to address this diversity, offering enhanced protection, mobility, and mission-specific equipment that cannot be achieved with standard military platforms. Another driver lies in the need for resilience and force protection. Modern conflicts often involve asymmetric tactics, such as ambushes and improvised explosive devices, which necessitate vehicles equipped with advanced armor, defensive systems, and high survivability standards. Militaries also recognize the importance of speed and maneuverability, requiring vehicles capable of operating in urban landscapes, remote areas, and rugged terrains without compromising safety. Economic and logistical considerations further shape demand. Modular and multi-role vehicles are appealing because they reduce lifecycle costs and maximize fleet utility by supporting multiple missions. Beyond combat, the growing role of armed forces in humanitarian aid, peacekeeping, and infrastructure restoration has strengthened the case for versatile vehicles. This blend of defense necessity and civil utility positions the market as strategically significant.

Regional Trends in Special Purpose Land Vehicles Market:

Regional demand for defense special purpose land vehicles reflects distinct operational environments, strategic priorities, and industrial capacities. Nations with expansive and often contested borders prioritize reconnaissance and patrol vehicles that ensure persistent monitoring and quick reaction capability. Countries with difficult terrain, such as mountains, deserts, or dense forests, seek platforms optimized for off-road endurance, logistics, and engineering tasks. These geographical factors heavily influence procurement choices, leading to diverse requirements across regions. In technologically advanced regions, emphasis is placed on modernization and the integration of digital systems. These militaries prioritize vehicles with modular configurations, advanced protection measures, and network-enabled capabilities to ensure interoperability with allied forces. By contrast, emerging economies often favor cost-efficient, multipurpose platforms that provide solid performance while remaining adaptable to various missions. This pragmatic approach allows them to balance budgetary constraints with operational effectiveness. Additionally, non-combat missions have influenced regional strategies. Areas prone to natural disasters invest in vehicles that can be deployed for relief and reconstruction, while countries engaged in peacekeeping focus on mobility and protection for stability operations. Domestic industrial capacity also plays a role, with some nations emphasizing indigenous development while others pursue partnerships or imports. This variety ensures that regional markets evolve in line with local priorities and global trends.

Key Special Purpose Land Vehicles Program:

The Finnish Defence Forces Logistics Command (FDFLOGCOM) has completed the acquisition of 29 Patria XA-300 (6X6) armoured personnel carriers for €36.5 million ($40.5 million), concluding the final phase of an expanded procurement agreement. These vehicles will strengthen the Finnish Army's operational capability, providing modern mobility assets expected to remain in service through the 2060s. This order represents the concluding tranche of a 2023 agreement that included an option for up to 70 additional units. With this procurement, the total fleet of Patria XA-300s moves closer to the full scope of the original contract, which initially covered 91 vehicles with an option for 70 more.

Table of Contents

Special Purpose Land Vehicles Market Report Definition

Special Purpose Land Vehicles Market Segmentation

By Application

By Region

By Type

Special Purpose Land Vehicles Market Analysis for next 10 Years

The 10-year special purpose land vehicles market analysis would give a detailed overview of special purpose land vehicles market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Special Purpose Land Vehicles Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Special Purpose Land Vehicles Market Forecast

The 10-year special purpose land vehicles market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Special Purpose Land Vehicles Market Trends & Forecast

The regional special purpose land vehicles market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Special Purpose Land Vehicles Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Special Purpose Land Vehicles Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Special Purpose Land Vehicles Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Type, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Application, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Type, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Application, 2025-2035

List of Figures

- Figure 1: Global Special Purpose Land Market Forecast, 2025-2035

- Figure 2: Global Special Purpose Land Market Forecast, By Region, 2025-2035

- Figure 3: Global Special Purpose Land Market Forecast, By Type, 2025-2035

- Figure 4: Global Special Purpose Land Market Forecast, By Application, 2025-2035

- Figure 5: North America, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 6: Europe, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 8: APAC, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 9: South America, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 10: United States, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 11: United States, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 12: Canada, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 14: Italy, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 16: France, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 17: France, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 18: Germany, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 24: Spain, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 30: Australia, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 32: India, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 33: India, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 34: China, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 35: China, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 40: Japan, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Special Purpose Land Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Special Purpose Land Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Special Purpose Land Market, By Type (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Special Purpose Land Market, By Type (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Special Purpose Land Market, By Application (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Special Purpose Land Market, By Application (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Special Purpose Land Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Special Purpose Land Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Special Purpose Land Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Special Purpose Land Market, By Region, 2025-2035

- Figure 58: Scenario 1, Special Purpose Land Market, By Type, 2025-2035

- Figure 59: Scenario 1, Special Purpose Land Market, By Application, 2025-2035

- Figure 60: Scenario 2, Special Purpose Land Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Special Purpose Land Market, By Region, 2025-2035

- Figure 62: Scenario 2, Special Purpose Land Market, By Type, 2025-2035

- Figure 63: Scenario 2, Special Purpose Land Market, By Application, 2025-2035

- Figure 64: Company Benchmark, Special Purpose Land Market, 2025-2035