PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 2042641

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 2042641

Global Personal Air Mobility Market 2026-2036

Global Personal Air Mobility Market

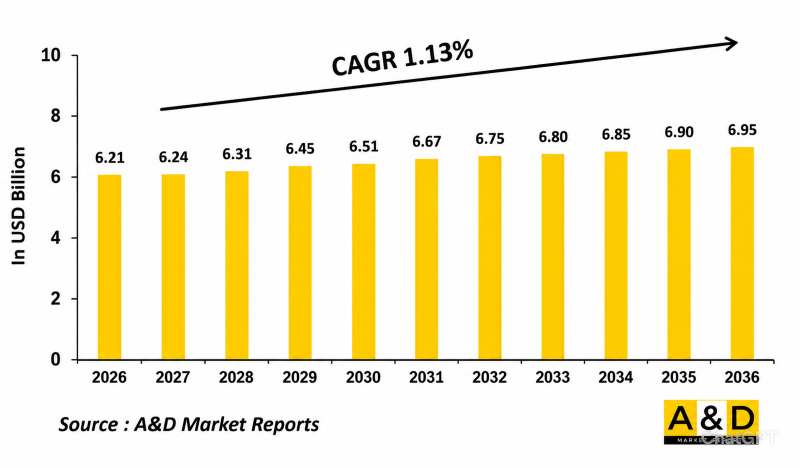

The Global Personal Air Mobility Market is estimated at USD 6.21 billion in 2026, projected to grow to USD 6.95 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 1.13% over the forecast period 2026-2036.

Introduction

The global personal air mobility market is an emerging segment of the aerospace and transportation industry focused on developing compact, efficient, and technologically advanced aircraft designed for individual and short-distance urban transportation. Personal air mobility solutions include electric vertical takeoff and landing aircraft, autonomous air taxis, compact helicopters, and lightweight flying vehicles intended to reduce urban congestion and improve transportation efficiency. These platforms are being developed for civilian mobility, emergency response, tourism, logistics, and defense-related applications. Growing urbanization, increasing traffic congestion, and advancements in electric propulsion technologies are driving interest in personal air mobility solutions worldwide. Governments, aerospace companies, and technology firms are investing heavily in next-generation air mobility ecosystems that integrate smart transportation infrastructure, autonomous navigation systems, and sustainable aviation technologies. In addition, the increasing emphasis on low-emission transportation, rapid urban mobility, and intelligent air traffic management is accelerating the development and commercialization of personal air mobility platforms across global markets. (mordorintelligence.com)

Technology Impact in the Global Personal Air Mobility Market

Technological advancement is significantly transforming the global personal air mobility market by improving flight efficiency, operational safety, autonomy, and environmental sustainability. Modern personal air mobility platforms increasingly incorporate electric propulsion systems, lightweight composite materials, artificial intelligence, and autonomous flight technologies to support safe and efficient urban transportation operations. Electric vertical takeoff and landing aircraft are gaining significant attention because they offer quieter operation, lower emissions, and reduced infrastructure requirements compared to conventional aircraft.

Artificial intelligence and machine learning technologies are enhancing autonomous navigation, obstacle detection, predictive maintenance, and real-time route optimization capabilities. Advanced battery systems, energy storage technologies, and distributed propulsion architectures are also improving flight endurance and operational reliability for electric air mobility platforms. Additionally, digital flight control systems, sensor fusion technologies, and satellite-based communication networks are supporting enhanced situational awareness and safer low-altitude airspace operations.

The integration of smart air traffic management systems and connected mobility infrastructure is further enabling coordinated urban air transportation networks. Cybersecurity and secure communication technologies are becoming increasingly important as autonomous and remotely operated aerial platforms enter commercial service. Furthermore, advancements in hybrid propulsion systems, vertical lift technologies, and automated emergency response systems continue to strengthen the commercial viability and operational flexibility of personal air mobility solutions. (marketsandmarkets.com)

Key Drivers in the Global Personal Air Mobility Market

One of the primary drivers of the global personal air mobility market is the increasing demand for efficient urban transportation solutions capable of reducing road congestion and travel time in densely populated cities. Rapid urbanization and expanding metropolitan populations are placing significant pressure on conventional transportation infrastructure, encouraging governments and private companies to explore advanced aerial mobility alternatives. (mordorintelligence.com)

Growing environmental concerns and the global transition toward sustainable transportation are also accelerating investments in electric and low-emission air mobility platforms. Electric propulsion technologies offer reduced carbon emissions, quieter operations, and improved energy efficiency, making them attractive for future urban transportation systems.

Another major growth driver is the increasing advancement of autonomous flight systems and digital aviation technologies. Aerospace companies and technology developers are investing heavily in autonomous navigation, artificial intelligence, and advanced communication systems that support safe and scalable urban air mobility operations. The rising demand for rapid emergency response, medical transportation, logistics delivery, and aerial ridesharing services is further contributing to market expansion

Government support for advanced air mobility infrastructure development, regulatory modernization initiatives, and smart city programs is also encouraging industry growth. In addition, increasing investments from aerospace manufacturers, automotive companies, and technology firms are strengthening research, development, and commercialization activities within the personal air mobility market worldwide.

Regional Trends in the Global Personal Air Mobility Market

North America remains a leading region in the global personal air mobility market due to strong aerospace innovation capabilities, advanced urban mobility initiatives, and substantial investment in electric aviation technologies. The region is heavily focused on autonomous air taxi development, urban air traffic management systems, and regulatory frameworks supporting commercial deployment of advanced air mobility platforms. (marketsandmarkets.com)

Europe is witnessing significant growth in the personal air mobility market as countries strengthen investments in sustainable transportation and smart city infrastructure. Collaborative aerospace programs, environmental sustainability policies, and urban mobility innovation initiatives are supporting the development of electric vertical takeoff and landing aircraft and autonomous air transportation systems.

The Asia-Pacific region is emerging as a rapidly expanding market driven by rising urbanization, increasing transportation congestion, and growing government support for advanced mobility technologies. Countries across the region are investing in smart transportation infrastructure, autonomous aviation systems, and electric aircraft manufacturing capabilities to strengthen urban mobility solutions.

The Middle East is also experiencing growing interest in personal air mobility technologies due to smart city development projects, tourism expansion, and investments in futuristic transportation systems. Meanwhile, Latin America and Africa are gradually exploring advanced aerial mobility solutions to improve urban connectivity, emergency response capabilities, and regional transportation efficiency.

Key Programs in the Global Personal Air Mobility Market

Several advanced air mobility and urban transportation programs are driving the growth of the global personal air mobility market. Governments, aerospace companies, and technology firms worldwide are implementing initiatives focused on developing safe, efficient, and commercially viable electric air mobility ecosystems.

Many organizations are conducting pilot programs involving autonomous air taxis, electric vertical takeoff and landing aircraft, and urban aerial ridesharing services to evaluate operational safety, airspace integration, and infrastructure requirements. Programs focused on smart vertiport development, digital air traffic management systems, and connected urban mobility networks are also supporting the commercialization of personal air mobility platforms. (mordorintelligence.com)

Emergency medical transport and logistics delivery programs are further expanding the application scope of personal air mobility technologies. In addition, military and defense-related mobility initiatives are encouraging the development of compact autonomous aerial platforms suitable for reconnaissance, rapid transport, and disaster response operations.

Research and development programs involving solid-state batteries, hydrogen propulsion systems, autonomous flight software, and advanced lightweight materials continue to shape the future of the market. Collaborative aerospace innovation projects, regulatory certification programs, and smart city transportation initiatives are also contributing significantly to long-term growth and technological advancement in the global personal air mobility market

Table of Contents

Personal Air Mobility Market - Table of Contents

Table of Contents

Personal Air Mobility Market Report Definition

Personal Air Mobility Market Segmentation

By Region

By Type

By Component

By End User

Personal Air Mobility Market Analysis for next 10 Years

The 10-year Personal Air Mobility market analysis would give a detailed overview of Personal Air Mobility market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Personal Air Mobility Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Personal Air Mobility Market Forecast

The 10-year Personal Air Mobility market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Personal Air Mobility Market Trends & Forecast

The regional Personal Air Mobility market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

REST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Market Forecast & Scenario Analysis

Europe

Middle East

APAC

South America

Country Analysis of Personal Air Mobility Market

This chapter deals with the key programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Program Mapping

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Personal Air Mobility Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Personal Air Mobility Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, Apac

- Table 12: Restraints, Impact Analysis, Apac

- Table 13: Challenges, Impact Analysis, Apac

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Component 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Type, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Component 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Type, 2026-2036

List of Figures

- Figure 1: Global Defense Personal Air Mobility Market Forecast, 2026-2036

- Figure 2: Global Defense Personal Air Mobility Market Forecast, By Region, 2026-2036

- Figure 3: Global Defense Personal Air Mobility Market Forecast, By Component 2026-2036

- Figure 4: Global Defense Personal Air Mobility Market Forecast, By Type, 2026-2036

- Figure 5: North America, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 6: Europe, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 7: Middle East, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 8: Apac, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 9: South America, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 10: United States, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 11: United States, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 12: Canada, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 13: Canada, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 14: Italy, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 15: Italy, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 16: France, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 17: France, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 18: Germany, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 19: Germany, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 21: Netherlands, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 23: Belgium, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 24: Spain, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 25: Spain, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 27: Sweden, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 28: Brazil, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 29: Brazil, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 30: Australia, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 31: Australia, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 32: India, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 33: India, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 34: China, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 35: China, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 39: South Korea, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 40: Japan, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 41: Japan, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 43: Malaysia, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 45: Singapore, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Personal Air Mobility Market , Region Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Personal Air Mobility Market , Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Personal Air Mobility Market , By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Personal Air Mobility Market , By Region (Cagr), 2026-2036

- Figure 50: Opportunity Analysis, Defense Personal Air Mobility Market , By Component Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Personal Air Mobility Market , By Component (Cagr), 2026-2036

- Figure 52: Opportunity Analysis, Defense Personal Air Mobility Market , By Type(Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Personal Air Mobility Market , By Type (Cagr), 2026-2036

- Figure 54: Scenario Analysis, Defense Personal Air Mobility Market , Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Personal Air Mobility Market , Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Personal Air Mobility Market , Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Personal Air Mobility Market , By Region, 2026-2036

- Figure 58: Scenario 1, Defense Personal Air Mobility Market , By Component 2026-2036

- Figure 59: Scenario 1, Defense Personal Air Mobility Market , By Type, 2026-2036

- Figure 60: Scenario 2, Defense Personal Air Mobility Market , Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Personal Air Mobility Market , By Region, 2026-2036

- Figure 62: Scenario 2, Defense Personal Air Mobility Market , By Component 2026-2036

- Figure 63: Scenario 2, Defense Personal Air Mobility Market , By Type, 2026-2036

- Figure 64: Company Benchmark, Defense Personal Air Mobility Market , 2026-2036