PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1896741

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1896741

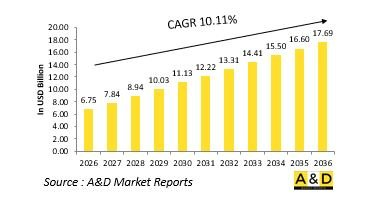

Global Fire Control Systems Market 2026-2036

The Global Fire Control Systems market is estimated at USD 6.75 billion in 2026, projected to grow to USD 17.69 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 10.11% over the forecast period 2026-2036.

Introduction to Fire Control Systems Market:

The defense fire control systems market is a crucial segment of modern military technology, enabling precise targeting, coordination, and execution of weapon engagements across land, air, and naval platforms. Fire control systems integrate sensors, radar, computing units, and control mechanisms to ensure accurate detection, tracking, and neutralization of threats. They serve as the operational core of tanks, artillery, naval guns, missiles, and aircraft-mounted weapons, transforming raw data into actionable firing solutions. As defense operations evolve toward greater automation and precision, fire control systems play an increasingly vital role in enhancing lethality, reducing human error, and improving real-time responsiveness. Global defense modernization efforts are focusing on digitalized, modular, and interoperable fire control systems that can adapt to multiple combat environments. This market continues to expand as militaries seek enhanced accuracy, faster response times, and integrated battlefield awareness.

Technology Impact in Fire Control Systems Market:

Technological innovation has significantly elevated the capability and performance of defense fire control systems. The integration of advanced sensors, electro-optical systems, and radar technologies enables improved target acquisition and tracking in complex environments. Artificial intelligence and machine learning enhance fire control algorithms, allowing predictive targeting and autonomous engagement in dynamic combat conditions. Digital signal processing and real-time data fusion combine inputs from multiple sensors to generate highly accurate firing solutions. Network-enabled fire control architectures allow seamless communication between different weapon platforms, ensuring coordinated strikes. Additionally, miniaturization and ruggedization of components enhance system reliability and mobility across platforms. Emerging technologies such as augmented reality interfaces, laser targeting, and precision-guided munitions are further redefining the accuracy and efficiency of modern fire control systems, transforming them into intelligent, adaptive components of network-centric warfare.

Key Drivers in Fire Control Systems market:

The growth of the defense fire control systems market is driven by the increasing demand for precision engagement and advanced target management capabilities in modern warfare. Rising emphasis on reducing collateral damage and enhancing first-shot accuracy fuels investment in sophisticated targeting technologies. Military modernization programs worldwide are prioritizing systems that can integrate with smart weapons, unmanned platforms, and real-time surveillance networks. The proliferation of asymmetric threats and high-speed aerial or missile targets necessitates fire control systems with advanced tracking and predictive capabilities. The shift toward multi-domain operations-integrating land, sea, air, and space assets-also requires interoperable fire control architectures. Furthermore, defense forces are investing in automation and artificial intelligence to reduce operator workload and improve decision-making speed. Collectively, these factors underscore the growing importance of intelligent fire control systems as enablers of precision and efficiency in modern defense strategies.

Regional Trends in Fire Control Systems Market:

Regional trends in the defense fire control systems market reflect varying levels of defense modernization, threat perception, and technological capability. North America remains a leader in advanced fire control technologies, driven by strong defense R&D and extensive integration across next-generation weapon platforms. Europe is focusing on collaborative development of digital and modular systems that enhance interoperability within allied forces. The Asia-Pacific region is rapidly upgrading its defense infrastructure, emphasizing indigenous production and integration of advanced fire control solutions into armored and aerial systems. The Middle East is investing heavily in precision engagement capabilities to address regional security challenges, particularly in countering missile and drone threats. Latin American and African nations are gradually adopting upgraded systems through international partnerships and technology transfers. Across all regions, the trend is toward integrated, networked, and sensor-driven fire control systems that enhance accuracy, speed, and situational awareness in complex combat environments.

Key Defense Fire Control Systems Program:

Leonardo DRS, Inc. has secured a firm fixed-price IDIQ contract valued at over $99 million to supply the U.S. Army with next-generation Mortar Fire Control Systems (MFCS). As part of the agreement, the company will manage the production and delivery of fire control systems, along with fielding services to support the Army's mortar Weapons and Fire Control programs. The MFCS enhances the Army's existing mortar fire control capabilities by integrating operations with the digital battlefield. The system combines a precise weapon pointing device, an inertial navigation and positioning system, and digital communication features within a rugged fire control computer. This enables mortar crews to exchange digital call-for-fire messages, determine weapon orientation and location, and compute ballistic solutions with improved responsiveness and accuracy.

Table of Contents

Fire Control Systems Market - Table of Contents

Fire Control Systems Market Report Definition

Fire Control Systems Market Segmentation

By Region

By Platform

By Operation

Fire Control Systems Market Analysis for next 10 Years

The 10-year Fire Control Systems Market analysis would give a detailed overview of Fire Control Systems Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Fire Control Systems Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Fire Control Systems Market Forecast

The 10-year Fire Control Systems Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Fire Control Systems Market Trends & Forecast

The regional Fire Control Systems Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Fire Control Systems Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Fire Control Systems Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Fire Control Systems Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Operation, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Operation, 2025-2035

List of Figures

- Figure 1: Global Fire Control Systems Market Forecast, 2025-2035

- Figure 2: Global Fire Control Systems Market Forecast, By Region, 2025-2035

- Figure 3: Global Fire Control Systems Market Forecast, By Platform, 2025-2035

- Figure 4: Global Fire Control Systems Market Forecast, By Operation, 2025-2035

- Figure 5: North America, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 6: Europe, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 8: APAC, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 9: South America, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 10: United States, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 11: United States, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 12: Canada, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 14: Italy, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 16: France, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 17: France, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 18: Germany, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 24: Spain, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 30: Australia, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 32: India, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 33: India, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 34: China, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 35: China, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 40: Japan, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Fire Control Systems Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Fire Control Systems Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Fire Control Systems Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Fire Control Systems Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Fire Control Systems Market, By Platform (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Fire Control Systems Market, By Platform (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Fire Control Systems Market, By Operation (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Fire Control Systems Market, By Operation (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Fire Control Systems Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Fire Control Systems Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Fire Control Systems Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Fire Control Systems Market, By Region, 2025-2035

- Figure 58: Scenario 1, Fire Control Systems Market, By Platform, 2025-2035

- Figure 59: Scenario 1, Fire Control Systems Market, By Operation, 2025-2035

- Figure 60: Scenario 2, Fire Control Systems Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Fire Control Systems Market, By Region, 2025-2035

- Figure 62: Scenario 2, Fire Control Systems Market, By Platform, 2025-2035

- Figure 63: Scenario 2, Fire Control Systems Market, By Operation, 2025-2035

- Figure 64: Company Benchmark, Fire Control Systems Market, 2025-2035