PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1896743

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1896743

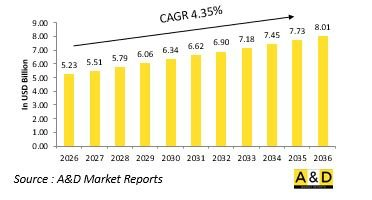

Global Defense Vetronics Market 2026-2036

The Global Defense Vetronics market is estimated at USD 5.23 billion in 2026, projected to grow to USD 8.01 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.35% over the forecast period 2026-2036.

Introduction to Defense Vetronics Market:

The defense vetronics market encompasses the electronic systems integrated into military vehicles to enhance their performance, situational awareness, and operational efficiency. Vetronics-short for vehicle electronics-serves as the digital backbone of armored vehicles, tanks, and tactical transport platforms. These systems combine navigation, communication, surveillance, power management, and command-and-control functionalities, enabling real-time information sharing and improved battlefield coordination. As modern combat becomes increasingly network-centric, vetronics play a vital role in connecting vehicles to wider defense communication grids, ensuring seamless data exchange and mission adaptability. The demand for smarter, interconnected, and survivable land systems continues to grow as militaries modernize their fleets for both conventional and asymmetric warfare. Vetronics are therefore becoming essential for improving crew safety, mission accuracy, and interoperability across multi-domain defense environments.

Technology Impact in Defense Vetronics Market:

The defense vetronics market encompasses the electronic systems integrated into military vehicles to enhance their performance, situational awareness, and operational efficiency. Vetronics-short for vehicle electronics-serves as the digital backbone of armored vehicles, tanks, and tactical transport platforms. These systems combine navigation, communication, surveillance, power management, and command-and-control functionalities, enabling real-time information sharing and improved battlefield coordination. As modern combat becomes increasingly network-centric, vetronics play a vital role in connecting vehicles to wider defense communication grids, ensuring seamless data exchange and mission adaptability. The demand for smarter, interconnected, and survivable land systems continues to grow as militaries modernize their fleets for both conventional and asymmetric warfare. Vetronics are therefore becoming essential for improving crew safety, mission accuracy, and interoperability across multi-domain defense environments.

Key Drivers in Defense Vetronics Market:

The key drivers propelling the defense vetronics market include the increasing demand for connected, digitalized, and modular land platforms. As modern battlefields rely heavily on real-time data exchange, the need for integrated systems that enhance communication, navigation, and situational awareness has intensified. Defense modernization programs are focusing on upgrading legacy vehicles with advanced vetronic architectures to improve mission readiness and interoperability. The rise of electronic warfare and cyber threats has also driven the development of more secure, hardened systems capable of maintaining functionality under attack. Growing emphasis on crew safety, efficiency, and automated vehicle operation further accelerates innovation in control, display, and diagnostic technologies. Additionally, the expansion of unmanned ground vehicles and hybrid-electric propulsion systems has increased reliance on sophisticated vetronics for control and power distribution. Together, these factors underscore the strategic role of vetronics in enabling smarter, more resilient, and networked defense platforms.

Regional Trends in Defense Vetronics Market:

Regional trends in the defense vetronics market reflect varying modernization priorities and industrial capabilities. North America continues to lead with extensive integration of advanced digital systems into armored fleets and next-generation combat vehicles. Europe is investing in modular vetronics solutions to enhance interoperability across multinational forces and joint missions. The Asia-Pacific region is witnessing rapid expansion driven by indigenous defense production, focusing on cost-effective and technologically advanced vehicle electronics. The Middle East is modernizing its armored fleets with emphasis on command-and-control, communication, and threat detection systems suited for desert and urban combat conditions. Latin America and Africa are gradually adopting vetronic upgrades through partnerships with international defense suppliers, emphasizing reliability and scalability. Across all regions, defense agencies are prioritizing the development of intelligent vehicle ecosystems that enhance situational awareness, combat survivability, and strategic mobility in increasingly digital warfare environments.

Key Defense Vetronics Program:

Leonardo DRS announced it has secured a U.S. Army contract to develop prototype Vehicle Integrated Power Kits (VIPKs) aimed at providing easily accessible, on-demand electrical power in operational environments. These kits will supply scalable, exportable power directly from tactical vehicles to mission-critical systems-such as communications, electronic warfare and counter-UAS capabilities-eliminating reliance on external power sources. The prototypes will be developed using Leonardo DRS's On-Board Vehicle Power (OBVP) technology, also known as TITAN, which can generate up to 120 kW of electrical power from the vehicle's drivetrain. This capability allows for the operation of high-energy systems including mobile command and control, missile defense launchers, radar systems, directed energy weapons and expeditionary power microgrids, whether the vehicle is in motion or stationary.

Table of Contents

Defense Vetronics Market - Table of Contents

Defense Vetronics Market Report Definition

Defense Vetronics Market Segmentation

By Platform

By Region

By End User

Defense Vetronics Market Analysis for next 10 Years

The 10-year defense vetronics market analysis would give a detailed overview of defense vetronics market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Vetronics Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Vetronics Market Forecast

The 10-year defense vetronics market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Vetronics Market Trends & Forecast

The regional defense vetronics market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Vetronics Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Vetronics Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Vetronics Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By End User, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By End User, 2025-2035

List of Figures

- Figure 1: Global Defense Vetronics Forecast, 2025-2035

- Figure 2: Global Defense Vetronics Forecast, By Region, 2025-2035

- Figure 3: Global Defense Vetronics Forecast, By Platform, 2025-2035

- Figure 4: Global Defense Vetronics Forecast, By End User, 2025-2035

- Figure 5: North America, Defense Vetronics, Market Forecast, 2025-2035

- Figure 6: Europe, Defense Vetronics, Market Forecast, 2025-2035

- Figure 7: Middle East, Defense Vetronics, Market Forecast, 2025-2035

- Figure 8: APAC, Defense Vetronics, Market Forecast, 2025-2035

- Figure 9: South America, Defense Vetronics, Market Forecast, 2025-2035

- Figure 10: United States, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 11: United States, Defense Vetronics, Market Forecast, 2025-2035

- Figure 12: Canada, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 13: Canada, Defense Vetronics, Market Forecast, 2025-2035

- Figure 14: Italy, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 15: Italy, Defense Vetronics, Market Forecast, 2025-2035

- Figure 16: France, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 17: France, Defense Vetronics, Market Forecast, 2025-2035

- Figure 18: Germany, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 19: Germany, Defense Vetronics, Market Forecast, 2025-2035

- Figure 20: Netherlands, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Defense Vetronics, Market Forecast, 2025-2035

- Figure 22: Belgium, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 23: Belgium, Defense Vetronics, Market Forecast, 2025-2035

- Figure 24: Spain, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 25: Spain, Defense Vetronics, Market Forecast, 2025-2035

- Figure 26: Sweden, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 27: Sweden, Defense Vetronics, Market Forecast, 2025-2035

- Figure 28: Brazil, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 29: Brazil, Defense Vetronics, Market Forecast, 2025-2035

- Figure 30: Australia, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 31: Australia, Defense Vetronics, Market Forecast, 2025-2035

- Figure 32: India, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 33: India, Defense Vetronics, Market Forecast, 2025-2035

- Figure 34: China, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 35: China, Defense Vetronics, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Defense Vetronics, Market Forecast, 2025-2035

- Figure 38: South Korea, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 39: South Korea, Defense Vetronics, Market Forecast, 2025-2035

- Figure 40: Japan, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 41: Japan, Defense Vetronics, Market Forecast, 2025-2035

- Figure 42: Malaysia, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Defense Vetronics, Market Forecast, 2025-2035

- Figure 44: Singapore, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 45: Singapore, Defense Vetronics, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Defense Vetronics, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Defense Vetronics, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Defense Vetronics, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Defense Vetronics, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Defense Vetronics, By Platform (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Defense Vetronics, By Platform (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Defense Vetronics, By End User (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Defense Vetronics, By End User (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Defense Vetronics, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Defense Vetronics, Global Market, 2025-2035

- Figure 56: Scenario 1, Defense Vetronics, Total Market, 2025-2035

- Figure 57: Scenario 1, Defense Vetronics, By Region, 2025-2035

- Figure 58: Scenario 1, Defense Vetronics, By Platform, 2025-2035

- Figure 59: Scenario 1, Defense Vetronics, By End User, 2025-2035

- Figure 60: Scenario 2, Defense Vetronics, Total Market, 2025-2035

- Figure 61: Scenario 2, Defense Vetronics, By Region, 2025-2035

- Figure 62: Scenario 2, Defense Vetronics, By Platform, 2025-2035

- Figure 63: Scenario 2, Defense Vetronics, By End User, 2025-2035

- Figure 64: Company Benchmark, Defense Vetronics, 2025-2035