PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1896748

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1896748

Global Defense Training and Simulation Market 2026-2036

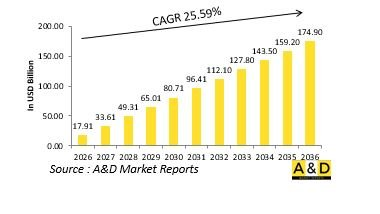

The Global Defense Training and Simulation market is estimated at USD 17.91 billion in 2026, projected to grow to USD 174.90 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 25.59% over the forecast period 2026-2036.

Introduction to Defense Training and Simulation Market

The defense training and simulation market encompasses advanced technologies and systems that replicate real-world military scenarios to prepare personnel for combat, strategic planning, and mission execution. These solutions combine virtual, constructive, and live simulation environments to enhance operational readiness and decision-making skills without the cost or risk associated with live exercises. Training and simulation systems cover a wide spectrum of defense domains, including air, land, naval, and cyber operations. They enable soldiers and commanders to rehearse complex missions, improve coordination, and assess outcomes in controlled conditions. With the increasing digitization of warfare and the emergence of sophisticated weapon systems, defense forces worldwide are investing heavily in simulated environments that can replicate high-threat, multi-domain battlefields. The growing importance of interoperability, precision warfare, and mission adaptability has made simulation-based training a vital component of defense preparedness and modernization strategies.

Technology Impact in Defense Training and Simulation Market:

Technology is profoundly reshaping the defense training and simulation market by creating highly immersive, data-driven, and adaptive training environments. Virtual and augmented reality technologies are enabling realistic, 360-degree combat simulations that replicate complex terrains and dynamic battlefield conditions. Artificial intelligence is being used to generate adaptive adversaries, analyze trainee performance, and personalize training modules in real time. The integration of cloud computing and networked simulation systems allows multiple units across different locations to train collaboratively in shared virtual spaces. Digital twins and advanced modeling tools are also enabling the simulation of entire weapon platforms or operational systems, allowing forces to train and test without risking physical assets. Moreover, advances in motion capture, haptic feedback, and high-fidelity graphics are making simulations more lifelike than ever before. These technological developments are transforming training from static exercises into intelligent, scalable ecosystems that enhance readiness and operational precision across all defense domains.

Key Drivers in Defense Training and Simulation Market:

The defense training and simulation market is primarily driven by the increasing complexity of modern warfare, which demands realistic and cost-effective methods to train personnel. The high operational and maintenance costs of advanced defense platforms have encouraged militaries to rely more on virtual environments for pilot, vehicle, and mission rehearsals. The rising emphasis on multi-domain operations-where air, land, sea, space, and cyber forces must work seamlessly-has also increased the need for integrated training systems. Budget efficiency, safety concerns, and sustainability goals further propel the adoption of simulation-based training as an alternative to resource-intensive field exercises. Defense modernization initiatives across the world highlight simulation as a key enabler for readiness and joint-force interoperability. Additionally, the emergence of unmanned and autonomous systems requires specialized training frameworks that can only be achieved through advanced simulation. Together, these factors underline simulation's role as an essential element in preparing defense personnel for evolving global threats.

Regional Trends in Defense Training and Simulation Market:

Regional trends in the defense training and simulation market reveal diverse patterns shaped by defense priorities and modernization agendas. North America leads through significant investments in high-fidelity simulation centers and AI-driven training solutions supporting air and joint-force operations. Europe emphasizes collaborative training systems that align with multinational defense frameworks, promoting interoperability among allied forces. The Asia-Pacific region is rapidly expanding its training infrastructure to enhance readiness amid rising geopolitical tensions and large-scale defense modernization. The Middle East focuses on simulation for air defense and counterterrorism training, optimizing operational efficiency in demanding environments. Latin America and Africa are increasingly incorporating simulation technologies to improve training standards through partnerships and technology transfers. Across all regions, the adoption of virtual and augmented reality platforms, networked simulation systems, and data analytics is accelerating. This global shift reflects a unified focus on enhancing combat preparedness, coordination, and decision-making through next-generation simulation-based training.

Key Defense Training and Simulation Program:

CAE announced that it has secured defence contracts worth over C$80 million in the fourth quarter of fiscal year 2016 to deliver simulation products and training services to military customers worldwide. Key awards include a contract from the NATO Support and Procurement Agency (NSPA) to carry out a major upgrade of the German Navy's Sea King MK41 helicopter simulator; a contract via Public Works and Government Services Canada (PWGSC) to provide the Canadian Coast Guard with a Bell 412/429 helicopter simulator; and a contract to upgrade the U.S. Air Force KC-135 tanker aircrew training devices. The KC-135 contract had been previously announced to trade media on February 11, though its value was not disclosed.

Table of Contents

Defense Training and Simulation Market - Table of Contents

Defense Training and Simulation Market Report Definition

Defense Training and Simulation Market Segmentation

By Region

By Component

By Application

Defense Training and Simulation Market Analysis for next 10 Years

The 10-year Defense Training and Simulation Market analysis would give a detailed overview of Defense Training and Simulation Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Training and Simulation Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Training and Simulation Market Forecast

The 10-year Defense Training and Simulation Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Training and Simulation Market Trends & Forecast

The regional Defense Training and Simulation Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Training and Simulation Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Training and Simulation Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Training and Simulation Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Component, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Application, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Component, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Application, 2025-2035

List of Figures

- Figure 1: Global Defense Training and Simulation Forecast, 2025-2035

- Figure 2: Global Defense Training and Simulation Forecast, By Region, 2025-2035

- Figure 3: Global Defense Training and Simulation Forecast, By Component, 2025-2035

- Figure 4: Global Defense Training and Simulation Forecast, By Application, 2025-2035

- Figure 5: North America, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 6: Europe, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 7: Middle East, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 8: APAC, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 9: South America, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 10: United States, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 11: United States, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 12: Canada, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 13: Canada, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 14: Italy, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 15: Italy, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 16: France, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 17: France, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 18: Germany, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 19: Germany, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 20: Netherlands, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 22: Belgium, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 23: Belgium, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 24: Spain, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 25: Spain, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 26: Sweden, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 27: Sweden, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 28: Brazil, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 29: Brazil, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 30: Australia, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 31: Australia, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 32: India, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 33: India, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 34: China, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 35: China, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 38: South Korea, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 39: South Korea, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 40: Japan, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 41: Japan, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 42: Malaysia, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 44: Singapore, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 45: Singapore, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Defense Training and Simulation, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Defense Training and Simulation, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Defense Training and Simulation, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Defense Training and Simulation, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Defense Training and Simulation, By Component (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Defense Training and Simulation, By Component (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Defense Training and Simulation, By Application (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Defense Training and Simulation, By Application (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Defense Training and Simulation, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Defense Training and Simulation, Global Market, 2025-2035

- Figure 56: Scenario 1, Defense Training and Simulation, Total Market, 2025-2035

- Figure 57: Scenario 1, Defense Training and Simulation, By Region, 2025-2035

- Figure 58: Scenario 1, Defense Training and Simulation, By Component, 2025-2035

- Figure 59: Scenario 1, Defense Training and Simulation, By Application, 2025-2035

- Figure 60: Scenario 2, Defense Training and Simulation, Total Market, 2025-2035

- Figure 61: Scenario 2, Defense Training and Simulation, By Region, 2025-2035

- Figure 62: Scenario 2, Defense Training and Simulation, By Component, 2025-2035

- Figure 63: Scenario 2, Defense Training and Simulation, By Application, 2025-2035

- Figure 64: Company Benchmark, Defense Training and Simulation, 2025-2035