PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 2030193

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 2030193

Global Defense Optronics Market 2026-2036

Global Defense Optronics Market

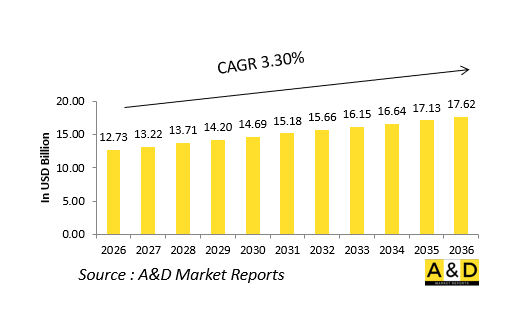

The Global Defense Optronics Market is estimated at USD 12.73 billion in 2026, projected to grow to USD 17.62 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 3.30% over the forecast period 2026-2036.

1. Introduction

The global defense optronics market represents a critical segment of modern military technology, integrating optical and electronic systems to enhance battlefield visibility, targeting precision, and situational awareness. These systems include thermal imaging devices, night vision equipment, laser rangefinders, and advanced sensor platforms that allow armed forces to operate effectively in low-visibility and complex environments. Optronics technologies convert light into electronic signals, enabling detection, identification, and tracking of targets across diverse operational conditions. Their application spans land, naval, air, and space domains, supporting missions such as surveillance, reconnaissance, navigation, and guided weapon targeting. As military operations increasingly demand round-the-clock capability and precision engagement, optronics systems have become indispensable. Continuous innovation, including integration with artificial intelligence and multispectral sensing, is transforming these systems into intelligent solutions that deliver real-time actionable insights, significantly improving decision-making and operational effectiveness.

2. Technology Impact in Defense Optronics Market

Technological advancements are fundamentally reshaping the defense optronics market by enhancing sensor performance, processing capabilities, and system integration. Modern systems increasingly combine thermal imaging, low-light sensors, and laser technologies into unified platforms, enabling comprehensive situational awareness. Artificial intelligence and machine learning algorithms are being embedded to automate target detection, classification, and tracking, reducing operator workload while improving accuracy. Sensor fusion technology enables data from multiple spectral bands to be integrated into a single visual output, offering deeper insights even in obscured environments. Miniaturization is another major trend, allowing deployment on unmanned systems and portable soldier equipment. Additionally, innovations in hyperspectral imaging and quantum sensing are pushing detection capabilities to new levels. These advancements are transforming optronics from passive observation tools into intelligent, decision-support systems that enhance battlefield efficiency and responsiveness.

3. Key Drivers in Defense Optronics Market

The growth of the defense optronics market is driven by the increasing need for advanced surveillance, targeting, and reconnaissance capabilities in modern warfare. Rising geopolitical tensions and evolving threat environments are encouraging nations to invest in technologies that enhance situational awareness and precision engagement. Modernization programs across military forces are accelerating the replacement of legacy systems with advanced optronic solutions. The proliferation of unmanned systems, including drones and autonomous platforms, is further boosting demand, as these systems rely heavily on high-performance optical sensors for navigation and targeting. Additionally, the growing emphasis on border security and counter-terrorism operations is increasing the need for reliable monitoring systems capable of operating in harsh environments. Continuous advancements in infrared and laser technologies, along with increased defense research funding, are also supporting market expansion by enabling the development of lighter, more efficient, and highly accurate systems.

4. Regional Trends in Defense Optronics Market

Regional dynamics in the defense optronics market are shaped by defense spending priorities, technological capabilities, and geopolitical conditions. North America remains a dominant region due to strong investment in advanced defense technologies and extensive research and development infrastructure. Europe is also a significant contributor, driven by modernization initiatives and collaborative defense programs among allied nations. The Asia-Pacific region is witnessing rapid growth, fueled by increasing military expenditure and the need to strengthen border security and surveillance capabilities. Countries in this region are actively investing in indigenous defense manufacturing and advanced optical technologies. Meanwhile, the Middle East and Africa are emerging as important markets due to ongoing security challenges and the need for enhanced monitoring systems. Across all regions, there is a clear trend toward integrating advanced sensor technologies with digital systems to improve operational effectiveness and strategic readiness.

5. Key Defense Optronics Market Program

Key programs in the defense optronics market focus on enhancing battlefield intelligence, surveillance, and targeting capabilities through advanced sensor integration. Governments are prioritizing initiatives that incorporate multispectral imaging, laser-guided targeting systems, and AI-enabled analytics into defense platforms. Soldier modernization programs are equipping personnel with advanced night vision and thermal imaging devices to improve combat effectiveness in low-visibility conditions. Naval and airborne platforms are being upgraded with next-generation electro-optical systems that support long-range detection and precision targeting. Additionally, defense agencies are investing in the development of compact and lightweight optronic payloads for unmanned systems, enabling enhanced reconnaissance and autonomous operations. Collaborative programs between defense organizations and private technology firms are accelerating innovation, ensuring the continuous evolution of optronics capabilities to meet emerging operational requirements.

Table of Contents

Defense Optronics Market - Table of Contents

Defense Optronics Market Report Definition

Defense Optronics Market Segmentation

By Region

By Technology

By Platform

Defense Optronics Market Analysis for next 10 Years

The 10-year Defense Optronics Market analysis would give a detailed overview of Defense Optronics Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Optronics Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Optronics Market Forecast

The 10-year Defense Optronics Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Optronics Market Trends & Forecast

The regional Defense Optronics Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Optronics Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Optronics Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Optronics Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, Apac

- Table 12: Restraints, Impact Analysis, Apac

- Table 13: Challenges, Impact Analysis, Apac

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Technology 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Technology2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Platform, 2026-2036

List of Figures

- Figure 1: Global Defense Optronics Market Forecast, 2026-2036

- Figure 2: Global Defense Optronics Market Forecast, By Region, 2026-2036

- Figure 3: Global Defense Optronics Market Forecast, By Technology 2026-2036

- Figure 4: Global Defense Optronics Market Forecast, By Platform, 2026-2036

- Figure 5: North America, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 6: Europe, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 7: Middle East, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 8: Apac, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 9: South America, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 10: United States, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 11: United States, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 12: Canada, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 13: Canada, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 14: Italy, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 15: Italy, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 16: France, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 17: France, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 18: Germany, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 19: Germany, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 21: Netherlands, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 23: Belgium, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 24: Spain, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 25: Spain, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 27: Sweden, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 28: Brazil, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 29: Brazil, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 30: Australia, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 31: Australia, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 32: India, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 33: India, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 34: China, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 35: China, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 39: South Korea, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 40: Japan, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 41: Japan, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 43: Malaysia, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 45: Singapore, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Optronics Market , Region Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Optronics Market , Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Optronics Market , By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Optronics Market , By Region (Cagr), 2026-2036

- Figure 50: Opportunity Analysis, Defense Optronics Market , By Technology Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Optronics Market , By Technology(Cagr), 2026-2036

- Figure 52: Opportunity Analysis, Defense Optronics Market , By Platform(Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Optronics Market , By Platform(Cagr), 2026-2036

- Figure 54: Scenario Analysis, Defense Optronics Market , Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Optronics Market , Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Optronics Market , Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Optronics Market , By Region, 2026-2036

- Figure 58: Scenario 1, Defense Optronics Market , By Technology 2026-2036

- Figure 59: Scenario 1, Defense Optronics Market , By Platform, 2026-2036

- Figure 60: Scenario 2, Defense Optronics Market , Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Optronics Market , By Region, 2026-2036

- Figure 62: Scenario 2, Defense Optronics Market , By Technology 2026-2036

- Figure 63: Scenario 2, Defense Optronics Market , By Platform, 2026-2036

- Figure 64: Company Benchmark, Defense Optronics Market , 2026-2036