PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 2027683

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 2027683

Global Defense Gyroscope Market

Global Defense Gyroscope Market

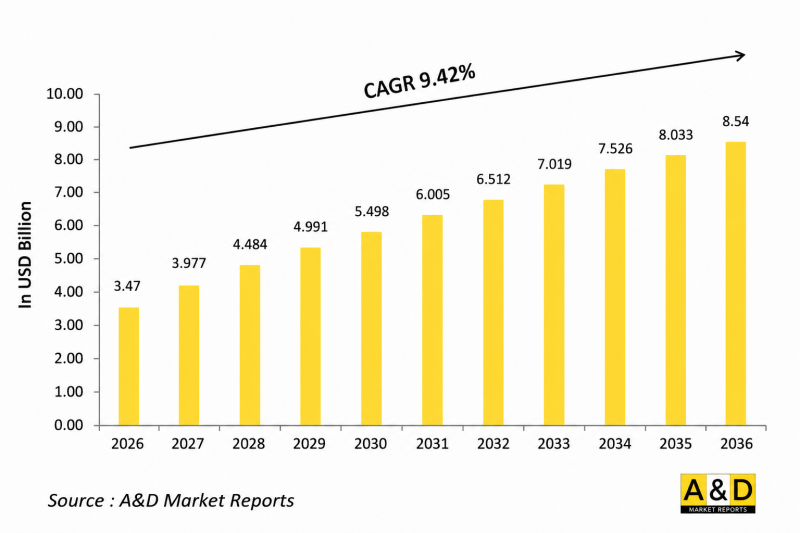

The Global Defense Gyroscope Market is estimated at USD 3.47 billion in 2026, projected to grow to USD 8.54 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 9.42% over the forecast period 2026-2036.

1. Introduction

The Global Defense Gyroscope Market represents a critical segment within military navigation and control systems, enabling accurate orientation, stabilization, and motion sensing across air, land, naval, and space platforms. Gyroscopes are fundamental components of inertial navigation systems used in fighter aircraft, submarines, missiles, and autonomous defense systems. Their ability to function independently of external signals makes them indispensable in GPS-denied or electronically contested environments.

Modern defense strategies increasingly rely on precision-guided operations and autonomous systems, both of which require highly reliable inertial sensing. As a result, gyroscopes have evolved from traditional mechanical designs to advanced solid-state and optical technologies. These systems support mission-critical applications such as targeting, surveillance, stabilization, and navigation.

The market is also shaped by growing defense modernization programs, rising geopolitical tensions, and the need for improved situational awareness. As militaries invest in next-generation platforms and digital warfare capabilities, gyroscopes continue to play a foundational role in enabling precision, resilience, and operational superiority across modern battlefields.

2. Technology Impact in Global Defense Gyroscope Market

Technological advancements are transforming the Global Defense Gyroscope Market by enhancing accuracy, reducing size, and improving system integration. The transition from conventional mechanical gyroscopes to Micro-Electro-Mechanical Systems (MEMS), fiber-optic gyroscopes, and ring laser gyroscopes has significantly improved performance across various defense applications. MEMS gyroscopes, in particular, enable compact, cost-effective solutions suitable for unmanned systems and portable military devices.

Fiber-optic and ring laser gyroscopes provide higher precision and stability, making them ideal for strategic applications such as submarine navigation and missile guidance. Emerging technologies such as quantum gyroscopes and cold-atom interferometry are further pushing the boundaries of accuracy, especially in environments where satellite navigation is unavailable.

Integration with artificial intelligence and sensor fusion technologies is another major development. These advancements allow gyroscopes to work seamlessly with accelerometers, GPS, and other sensors to provide enhanced situational awareness and real-time decision-making. Additionally, system-on-chip designs are enabling complete inertial measurement units with reduced power consumption and improved reliability.

3. Key Drivers in Global Defense Gyroscope Market

The Global Defense Gyroscope Market is primarily driven by the increasing need for precision navigation and guidance systems in modern military operations. As defense forces adopt advanced weapon systems, including precision-guided munitions and autonomous vehicles, the demand for highly accurate gyroscopic sensors continues to rise. These systems are essential for ensuring mission success in complex and dynamic combat environments.

Another major driver is the growing deployment of unmanned and autonomous platforms across all domains. Drones, unmanned ground vehicles, and autonomous naval systems require compact and reliable inertial navigation solutions, making gyroscopes indispensable components. The expansion of these platforms is significantly accelerating market growth.

Rising global defense modernization initiatives also play a crucial role. Governments are investing heavily in upgrading military capabilities, focusing on advanced avionics, navigation systems, and electronic warfare resilience. Gyroscopes are central to these upgrades, particularly in systems operating in GPS-denied environments.

Additionally, technological advancements such as miniaturization, improved durability, and enhanced resistance to harsh conditions are further boosting adoption. The integration of gyroscopes with AI-driven analytics and multi-sensor systems enhances operational efficiency and situational awareness, creating strong long-term demand across defense sectors.

4. Regional Trends in Global Defense Gyroscope Market

Regional dynamics in the Global Defense Gyroscope Market are shaped by defense spending patterns, technological capabilities, and geopolitical priorities. North America remains a dominant region due to its advanced defense infrastructure, strong industrial base, and continuous investment in next-generation military technologies. The presence of major defense contractors and extensive research initiatives further strengthens the region's leadership.

Europe is characterized by collaborative defense programs and a strong focus on high-performance aerospace systems. Countries in this region emphasize innovation and joint development initiatives, particularly in navigation and avionics technologies. These collaborations support the development of advanced gyroscopic systems for multinational defense projects.

The Asia-Pacific region is witnessing rapid growth driven by increasing defense budgets and the push for indigenous manufacturing capabilities. Countries such as India, China, Japan, and South Korea are investing in advanced military technologies, including autonomous systems and precision navigation solutions. This trend is creating significant opportunities for gyroscope manufacturers.

Meanwhile, regions such as the Middle East and Latin America are gradually expanding their defense capabilities, focusing on modernization and strategic procurement. These regions are increasingly adopting advanced navigation technologies to enhance operational readiness and national security.

5. Key Global Defense Gyroscope Market Program

Key programs within the Global Defense Gyroscope Market are closely linked to broader military modernization and advanced weapons development initiatives. One of the most significant areas of deployment is missile guidance systems, where high-precision gyroscopes are essential for trajectory control and targeting accuracy. These programs demand extremely reliable and high-performance inertial sensors.

Naval programs also play a crucial role, particularly in submarine navigation systems that require long-duration accuracy without external references. Fiber-optic gyroscopes are widely used in such applications due to their stability and resistance to environmental disturbances.

In the aerospace sector, gyroscopes are integral to aircraft navigation, flight control systems, and stabilization mechanisms. Modern fighter jets and transport aircraft rely on advanced inertial measurement units to maintain operational efficiency in contested environments.

Unmanned system programs are another major focus area. Military investments in drones and autonomous platforms are driving the adoption of compact, lightweight gyroscopes that support real-time navigation and control. Additionally, emerging programs in space defense and satellite navigation are expanding the application scope of gyroscopic technologies, highlighting their strategic importance in future warfare systems.

Table of Contents

Defense Gyroscope Market - Table of Contents

Defense Gyroscope Market Report Definition

Defense Gyroscope Market Segmentation

By Type

By Region

By Platform

Defense Gyroscope Market Analysis for next 10 Years

The 10-year Defense Gyroscope Market analysis would give a detailed overview of Defense Gyroscope Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Gyroscope Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Gyroscope Market Forecast

The 10-year Defense Gyroscope Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Gyroscope Market Trends & Forecast

The regional Defense Gyroscope Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Gyroscope Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Gyroscope Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Gyroscope Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, Apac

- Table 12: Restraints, Impact Analysis, Apac

- Table 13: Challenges, Impact Analysis, Apac

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Type, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Type, 2026-2036

List of Figures

- Figure 1: Global Defense Gyroscope Market Forecast, 2026-2036

- Figure 2: Global Defense Gyroscope Market Forecast, By Region, 2026-2036

- Figure 3: Global Defense Gyroscope Market Forecast, By Platform 2026-2036

- Figure 4: Global Defense Gyroscope Market Forecast, By Type, 2026-2036

- Figure 5: North America, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 6: Europe, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 7: Middle East, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 8: Apac, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 9: South America, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 10: United States, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 11: United States, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 12: Canada, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 13: Canada, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 14: Italy, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 15: Italy, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 16: France, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 17: France, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 18: Germany, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 19: Germany, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 21: Netherlands, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 23: Belgium, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 24: Spain, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 25: Spain, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 27: Sweden, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 28: Brazil, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 29: Brazil, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 30: Australia, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 31: Australia, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 32: India, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 33: India, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 34: China, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 35: China, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 39: South Korea, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 40: Japan, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 41: Japan, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 43: Malaysia, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 45: Singapore, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Gyroscope Market , Region Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Gyroscope Market , Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Gyroscope Market , By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Gyroscope Market , By Region (Cagr), 2026-2036

- Figure 50: Opportunity Analysis, Defense Gyroscope Market , By Platform Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Gyroscope Market , By Platform(Cagr), 2026-2036

- Figure 52: Opportunity Analysis, Defense Gyroscope Market , By Type(Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Gyroscope Market , By Type(Cagr), 2026-2036

- Figure 54: Scenario Analysis, Defense Gyroscope Market , Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Gyroscope Market , Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Gyroscope Market , Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Gyroscope Market , By Region, 2026-2036

- Figure 58: Scenario 1, Defense Gyroscope Market , By Platform 2026-2036

- Figure 59: Scenario 1, Defense Gyroscope Market , By Type, 2026-2036

- Figure 60: Scenario 2, Defense Gyroscope Market , Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Gyroscope Market , By Region, 2026-2036

- Figure 62: Scenario 2, Defense Gyroscope Market , By Platform 2026-2036

- Figure 63: Scenario 2, Defense Gyroscope Market , By Type, 2026-2036

- Figure 64: Company Benchmark, Defense Gyroscope Market , 2026-2036