PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1951127

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1951127

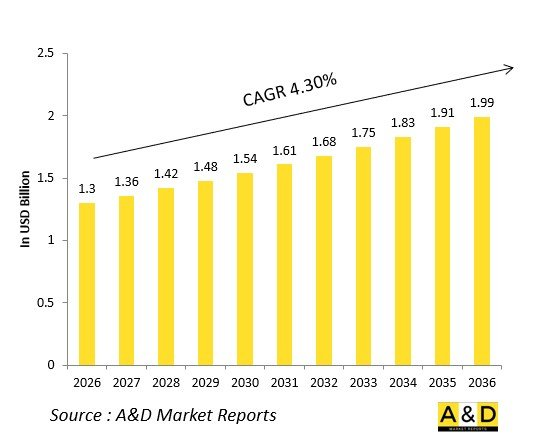

Global Defense 3D Air Search Radars Market 2026-2036

The Global Defense 3D Air Search Radars market is estimated at USD 1.3 billion in 2026, projected to grow to USD 1.99 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.30% over the forecast period 2026-2036.

Introduction

The global market for Defense 3D Air Search Radars is poised for substantial evolution, driven by escalating geopolitical tensions and the imperative for superior aerial surveillance capabilities. These radars, pivotal for detecting, tracking, and identifying airborne threats across vast expanses, integrate advanced phased array technologies to deliver precise elevation, azimuth, and range data. Key players are innovating with active electronically scanned arrays (AESA) and gallium nitride (GaN)-based systems, enhancing detection of stealthy targets, drones, and hypersonic missiles amid rising asymmetric warfare risks.

Market growth hinges on modernization programs replacing legacy systems with multi-mission platforms that support integrated air defense networks. Naval and ground-based variants dominate, bolstered by interoperability with 5G-enabled command systems and AI-driven data fusion. Emerging challenges include electronic warfare resilience and supply chain disruptions, yet opportunities abound in collaborative international programs and export deals to allied nations. This period will witness a shift toward software-defined radars, prioritizing agility, reduced lifecycle costs, and seamless integration into networked battle management architectures.

Technology Impact in Defense 3D Air Search Radars

Technological advancements are revolutionizing Defense 3D Air Search Radars, elevating their role from passive sentinels to proactive force multipliers in contested airspace. Gallium nitride amplifiers enable higher power outputs and sensitivity, extending detection envelopes against low-observable threats while minimizing size, weight, and power demands for mobile deployments. AESA architectures provide rapid beam steering, simultaneous multi-target tracking, and electronic counter-countermeasures, outpacing mechanical radars in dynamic threat environments.

Cognitive radar paradigms, infused with machine learning, adapt waveforms in real-time to jamming and clutter, enhancing accuracy in urban or littoral zones. Integration with hyperspectral sensors and quantum-enhanced processing promises clutter rejection and micro-drone discrimination. Digital beamforming and open-system architectures facilitate rapid upgrades, aligning with joint all-domain operations. These innovations reduce operator workload through automated threat prioritization and foster interoperability across air, sea, and land platforms, fundamentally reshaping air defense strategies amid proliferating precision-guided munitions and swarm tactics.

Key Drivers in Defense 3D Air Search Radars

Several interconnected factors propel the Defense 3D Air Search Radars sector forward. Heightened great-power competition fuels demand for radars capable of countering advanced aerial threats, including hypersonic glide vehicles and low-observable cruise missiles, prompting accelerated procurement cycles. Budget reallocations toward air defense prioritize systems with proven multi-role versatility, integrating seamlessly into layered missile defense architectures.

Technological convergence-merging radar with AI analytics, 5G communications, and satellite data-drives adoption of next-generation platforms that enhance battlespace awareness. Export opportunities surge as middle powers seek sovereign capabilities amid supply chain vulnerabilities exposed by recent conflicts. Regulatory pressures on electromagnetic spectrum efficiency and cybersecurity further incentivize upgrades to resilient, software-reconfigurable designs.

Sustainability mandates push for low-maintenance, energy-efficient systems using advanced materials, while collaborative R&D initiatives between governments and industry accelerate innovation. Collectively, these drivers underscore a market trajectory emphasizing robustness, adaptability, and networked superiority to maintain strategic deterrence.

Regional Trends in Defense 3D Air Search Radars

Regional dynamics shape the Defense 3D Air Search Radars landscape distinctly. In Asia-Pacific, territorial disputes intensify focus on long-range naval and coastal systems, with indigenous development emphasizing AESA integration for blue-water operations. Europe prioritizes NATO interoperability, favoring modular upgrades to legacy platforms amid hybrid threat proliferation from near-peer adversaries.

North America leads in cutting-edge GaN and cognitive technologies, exporting advanced systems while modernizing its integrated air defense grid. The Middle East sees rapid adoption driven by ballistic missile proliferation, with emphasis on mobile, high-mobility radars for expeditionary forces. In Latin America and Africa, budget constraints steer trends toward cost-effective COTS-based solutions and second-hand modernizations, bolstered by technology transfers.

Cross-regional collaborations, such as joint ventures for supply chain resilience, mitigate geopolitical risks, while climate-adaptive designs address harsh operational environments. Overall, regions converge on networked, multi-domain radars to counter evolving aerial challenges.

Key Defense 3D Air Search Radars Programs

Prominent Defense 3D Air Search Radars programs exemplify global innovation in air surveillance. Leading naval initiatives feature shipborne AESA systems with 360-degree coverage, designed for carrier strike groups and littoral combatants, incorporating GaN for hypersonic threat engagement. Ground-based programs advance mobile S-band radars with over-the-horizon extensions, prioritizing swarm defense and ballistic missile warning.

Airborne variants evolve through podded configurations for fighter jets and UAVs, emphasizing lightweight digital arrays for persistent ISR. International collaborations yield multi-national efforts like enhanced early-warning networks, fusing radar data with space-based assets for persistent domain awareness.

Key programs stress open architectures for third-party payloads, cyber-hardened firmware, and AI augmentation for reduced false alarms. These efforts, spanning upgrades to new-builds, underscore commitments to sovereign capabilities, export compliance, and integration within joint operations frameworks.

Table of Contents

Defense 3D Air Search Radars Market - Table of Contents

Defense 3D Air Search Radars Market Report Definition

Defense 3D Air Search Radars Market Segmentation

By Region

By Platform

By Frequency Band

By Range

Defense 3D Air Search Radars Market Analysis for next 10 Years

The 10-year Defense 3D Air Search Radars Market analysis would give a detailed overview of Defense 3D Air Search Radars Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense 3D Air Search Radars Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense 3D Air Search Radars Market Forecast

The 10-year Defense 3D Air Search Radars Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense 3D Air Search Radars Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense 3D Air Search Radars Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense 3D Air Search Radars Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense 3D Air Search Radars Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Frequency Band, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Frequency Band, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Region, 2026-2036

List of Figures

- Figure 1: Global Defense 3D Air Search Radars Market Forecast, 2026-2036

- Figure 2: Global Defense 3D Air Search Radars Market Forecast, By Frequency Band, 2026-2036

- Figure 3: Global Defense 3D Air Search Radars Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense 3D Air Search Radars Market Forecast, By Region, 2026-2036

- Figure 5: North America, Defense 3D Air Search Radars Market, Forecast, 2026-2036

- Figure 6: Europe, Defense 3D Air Search Radars Market, Forecast, 2026-2036

- Figure 7: Middle East, Defense 3D Air Search Radars Market, Forecast, 2026-2036

- Figure 8: APAC, Defense 3D Air Search Radars Market, Forecast, 2026-2036

- Figure 9: South America, Defense 3D Air Search Radars Market, Forecast, 2026-2036

- Figure 10: United States, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 11: United States, Defense 3D Air Search Radars Market, Forecast, 2026-2036

- Figure 12: Canada, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 13: Canada, Defense 3D Air Search Radars Market, Forecast, 2026-2036

- Figure 14: Italy, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 15: Italy, Defense 3D Air Search Radars Market, Market Forecast, 2026-2036

- Figure 16: France, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 17: France, Defense 3D Air Search Radars Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 19: Germany, Defense 3D Air Search Radars Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, Defense 3D Air Search Radars Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, Defense 3D Air Search Radars Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 25: Spain, Defense 3D Air Search Radars Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, Defense 3D Air Search Radars Market, Forecast, 2026-2036

- Figure 28: Brazil, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, Defense 3D Air Search Radars Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 31: Australia, Defense 3D Air Search Radars Market, Market Forecast, 2026-2036

- Figure 32: India, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 33: India, Defense 3D Air Search Radars Market, Market Forecast, 2026-2036

- Figure 34: China, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 35: China, Defense 3D Air Search Radars Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense 3D Air Search Radars Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, Defense 3D Air Search Radars Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 41: Japan, Defense 3D Air Search Radars Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, Defense 3D Air Search Radars Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, Defense 3D Air Search Radars Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense 3D Air Search Radars Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Defense 3D Air Search Radars Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense 3D Air Search Radars Market, By Frequency Band (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense 3D Air Search Radars Market, By Frequency Band (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense 3D Air Search Radars Market, By (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense 3D Air Search Radars Market, By Platform(CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense 3D Air Search Radars Market, By Region (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense 3D Air Search Radars Market, By Region (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense 3D Air Search Radars Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense 3D Air Search Radars Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense 3D Air Search Radars Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense 3D Air Search Radars Market, By Frequency Band, 2026-2036

- Figure 58: Scenario 1, Defense 3D Air Search Radars Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Defense 3D Air Search Radars Market, By Region, 2026-2036

- Figure 60: Scenario 2, Defense 3D Air Search Radars Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense 3D Air Search Radars Market, By Frequency Band, 2026-2036

- Figure 62: Scenario 2, Defense 3D Air Search Radars Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Defense 3D Air Search Radars Market, By Region, 2026-2036

- Figure 64: Company Benchmark, Defense 3D Air Search Radars Market, 2026-2036