PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1996989

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1996989

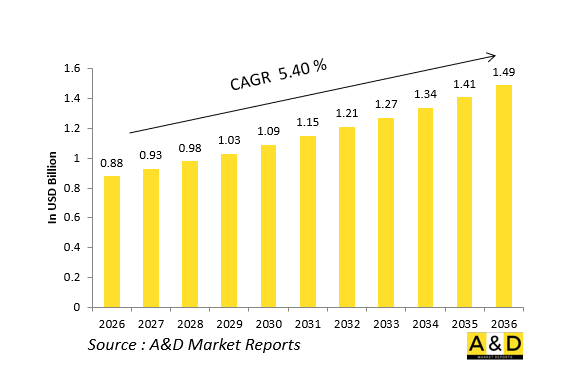

Global Defense GPS / GNSS Receivers (Anti-Jam) Market 2026-2036

Global Defense GPS / GNSS Receivers (Anti Jam) Market

The Global Defense GPS / GNSS Receivers (Anti Jam) Market is estimated at USD 0.88 billion in 2026, projected to grow to USD 1.49 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 5.40% over the forecast period 2026-2036.

1. Introduction:

Defense grade GPS and GNSS receivers with anti jam capabilities are critical navigation and timing nodes that provide secure, resilient position, velocity, and time information for military platforms operating in contested electromagnetic environments. These systems are embedded in aircraft, ships, ground vehicles, missiles, and command and control nodes, enabling precision navigation, targeting, and time synchronization without relying on vulnerable civilian grade signals. Over the 2026-2036 horizon, the market is expanding as armed forces recognize that unhardened GNSS links are increasingly susceptible to jamming, spoofing, and cyber enabled disruption.

Modern anti jam receivers integrate advanced signal processing techniques, directional antennas, and cryptographic protections to maintain reliable navigation even under heavy electronic warfare pressure. They are increasingly combined with inertial, terrain based, and alternative PNT sources to form hybrid architectures that can sustain operations during prolonged GPS outages. As multi domain and networked warfare becomes the norm, anti jam GPS/GNSS receivers are evolving from simple timing modules into secure, mission critical subsystems that underpin everything from precision strike coordination to secure communications and autonomous platform operations.

2. Technology Impact in Defense GPS / GNSS Receivers (Anti Jam) Market

Technology is transforming defense GPS/GNSS receivers from basic signal tracking units into intelligent, software defined, spectrum aware nodes. Modern anti jam receivers leverage high sensitivity, multi frequency, multi constellation architectures that exploit signals from several satellite systems to improve availability and resilience. Advanced digital signal processing, including adaptive filtering and interference cancellation algorithms, allows these receivers to reject jamming sources while maintaining lock on weak or degraded signals.

Integration with controlled reception pattern antennas (CRPA) and multi element phased arrays enables spatial nulling of jamming directions, significantly improving signal to noise margins in hostile environments. Software defined receiver architectures support over the air updates and reconfiguration for new frequencies, modulation schemes, or cryptographic keys, shortening integration cycles for next generation platforms. On the security side, military specific cryptographic modules and encrypted signals provide assured positioning and timing that are resistant to spoofing and manipulation. These innovations collectively raise platform survivability, extend operational reach in contested regions, and support autonomous and networked operations where precise, trusted timing is essential.

3. Key Drivers in Defense GPS / GNSS Receivers (Anti Jam) Market

The defense anti jam GPS/GNSS receiver market is driven by the growing threat of electronic warfare, where adversaries can easily degrade or deny civilian GNSS services using relatively low cost jammers and spoofing techniques. As a result, armed forces are investing in hardened, military specific receivers that can operate reliably in high jamming environments and support mission critical navigation, targeting, and communications. This requirement spans fighters, UAVs, missiles, artillery, naval vessels, and ground based C4ISR systems, all of which depend on precise timing and positioning.

Another key driver is the expansion of multi domain and network centric operations, where synchronized positioning and time are essential for joint targeting, coordinated strikes, and sensor fusion. Modern precision guided munitions, autonomous vehicles, and distributed sensor networks all rely on resilient GNSS inputs at every phase of flight or mission. Fleet modernization and life extension programs are also accelerating the retrofit of legacy platforms with upgraded anti jam receivers compatible with new satellite constellations and encrypted signals. Interoperability and standardization requirements across allied forces further encourage adoption of common anti jam architectures, while safety and certification standards reinforce demand for robust, fault tolerant, tamper resistant designs. Together, these factors are increasing the demand for scalable, software upgradable, and cyber secure GPS/GNSS receivers across the defense ecosystem.

4. Regional Trends in Defense GPS / GNSS Receivers (Anti Jam) Market

Regionally, North America leads the anti jam GPS/GNSS receiver market, supported by large scale fighter, bomber, UAV, missile, and C4ISR programs that prioritize resilient positioning and timing capabilities. The United States and its partners emphasize hardened, multi constellation receivers integrated into digital flight control systems, mission computers, and secure communications suites, often tied to advanced satellite navigation services. European defense programs are increasingly adopting common anti jam architectures across multi role platforms, favoring interoperable receivers that support cross national standards and shared logistics.

The Asia Pacific region is witnessing rapid growth as several nations modernize their air forces, navies, and missile forces with indigenous or co developed anti jam GNSS solutions tailored to regional electronic warfare threats. Middle Eastern and Gulf states are investing in hardened receivers for both new build platforms and retrofits, ensuring continued navigation capability in high jamming environments. Across these regions, there is a growing preference for modular, open architecture anti jam receivers that can be reused or upgraded across fixed wing, rotary wing, naval, and ground platforms. Domestic supply and technology sovereignty policies are also encouraging regional design and production, while export control and security regimes shape the availability and configuration of high end anti jam units.

5. Key Defense GPS / GNSS Receivers (Anti Jam) Market Program

Several flagship defense programs are shaping the anti jam GPS/GNSS receiver market over the 2026-2036 period. Next generation fighter and multi role combat air programs are specifying advanced anti jam receivers that integrate tightly with digital flight control systems, mission computers, and electronic warfare suites, enabling precise navigation and targeting even under heavy jamming. Naval aviation and maritime programs are equipping carrier based and long range platforms with hardened receivers that support carrier operations, over water navigation, and coordinated strike operations in contested maritime environments.

Unmanned combat air, long endurance UAV, and swarming drone programs are relying on compact, low power anti jam receivers to enable autonomous flight, waypoint navigation, and formation keeping without continuous reliance on clean GNSS signals. Missile and precision guided munitions programs are integrating miniaturized military grade GNSS modules into guidance sections to maintain accuracy when faced with jamming or spoofing during terminal phase flight. Ground based C4ISR, artillery, and electronic warfare systems are adopting anti jam GNSS receivers to provide secure, synchronized timing for communications, radar, and networked operations. Multinational and coalition level programs are standardizing GNSS receiver interfaces and data formats, enabling shared software libraries, certification packages, and sustainment arrangements across partner nations. Through these programs, anti jam GPS/GNSS receivers are becoming foundational elements of the resilient, multi domain digital warfare infrastructure.

Table of Contents

Defense GPS / GNSS Receivers (Anti-Jam) Market - Table of Contents

Defense GPS / GNSS Receivers (Anti-Jam) Market Report Definition

Defense GPS / GNSS Receivers (Anti-Jam) Market Segmentation

By Region

By Jamming Protection Level

By Platform

By Receiver Type

By Integration

Defense GPS / GNSS Receivers (Anti-Jam) Market Analysis for next 10 Years

The 10-year Defense GPS / GNSS Receivers (Anti-Jam) Market analysis would give a detailed overview of Defense GPS / GNSS Receivers (Anti-Jam) Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense GPS / GNSS Receivers (Anti-Jam) Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense GPS / GNSS Receivers (Anti-Jam) Market Forecast

The 10-year Defense GPS / GNSS Receivers (Anti-Jam) Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense GPS / GNSS Receivers (Anti-Jam) Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense GPS / GNSS Receivers (Anti-Jam) Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense GPS / GNSS Receivers (Anti-Jam) Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense GPS / GNSS Receivers (Anti-Jam) Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Anti-Jam Tech Level, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Anti-Jam Tech Level, 2026-2036

List of Figures

- Figure 1: Global Defense GPS / GNSS Receivers (Anti-Jam) Market Forecast, 2026-2036

- Figure 2: Global Defense GPS / GNSS Receivers (Anti-Jam) Market Forecast, By Region, 2026-2036

- Figure 3: Global Defense GPS / GNSS Receivers (Anti-Jam) Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense GPS / GNSS Receivers (Anti-Jam) Market Forecast, By Anti-Jam Tech Level, 2026-2036

- Figure 5: North America, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 6: Europe, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 7: Middle East, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 8: APAC, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 9: South America, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 10: United States, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 11: United States, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 12: Canada, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 13: Canada, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 14: Italy, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 15: Italy, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 16: France, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 17: France, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 19: Germany, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 21: Netherlands, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 23: Belgium, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 25: Spain, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 27: Sweden, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 29: Brazil, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 31: Australia, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 32: India, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 33: India, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 34: China, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 35: China, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 39: South Korea, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 41: Japan, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 43: Malaysia, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 45: Singapore, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense GPS / GNSS Receivers (Anti-Jam) Market, Region Maturation, 2026-2036

- Figure 47: United Kingdom, Defense GPS / GNSS Receivers (Anti-Jam) Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense GPS / GNSS Receivers (Anti-Jam) Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense GPS / GNSS Receivers (Anti-Jam) Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense GPS / GNSS Receivers (Anti-Jam) Market, By Platform (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense GPS / GNSS Receivers (Anti-Jam) Market, By Platform (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense GPS / GNSS Receivers (Anti-Jam) Market, By Anti-Jam Tech Level(Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense GPS / GNSS Receivers (Anti-Jam) Market, By Anti-Jam Tech Level(CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense GPS / GNSS Receivers (Anti-Jam) Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense GPS / GNSS Receivers (Anti-Jam) Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense GPS / GNSS Receivers (Anti-Jam) Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense GPS / GNSS Receivers (Anti-Jam) Market, By Region, 2026-2036

- Figure 58: Scenario 1, Defense GPS / GNSS Receivers (Anti-Jam) Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Defense GPS / GNSS Receivers (Anti-Jam) Market, By Anti-Jam Tech Level, 2026-2036

- Figure 60: Scenario 2, Defense GPS / GNSS Receivers (Anti-Jam) Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense GPS / GNSS Receivers (Anti-Jam) Market, By Region, 2026-2036

- Figure 62: Scenario 2, Defense GPS / GNSS Receivers (Anti-Jam) Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Defense GPS / GNSS Receivers (Anti-Jam) Market, By Anti-Jam Tech Level, 2026-2036

- Figure 64: Company Benchmark, Defense GPS / GNSS Receivers (Anti-Jam) Market, 2026-2036