PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1996993

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1996993

Global Defense Angle of Attack (AoA) Sensors Market 2026-2036

Global Defense Angle of Attack (AoA) Sensors Market

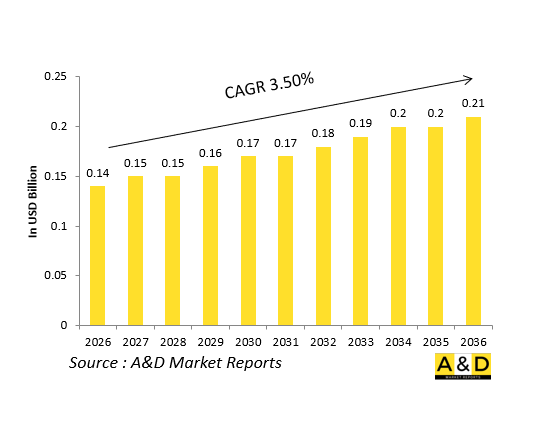

The Global Defense Angle of Attack (AoA) Sensors Market is estimated at USD 0.14 billion in 2026, projected to grow to USD 0.21 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 3.50% over the forecast period 2026-2036.

1. Introduction:

Defense Angle of Attack (AoA) sensors are critical aerodynamic instruments that measure the angle between an aircraft's oncoming airflow and its reference chord line, providing essential data for flight control systems, envelope protection, and stall awareness functions. These sensors are embedded in fighters, trainers, maritime patrol aircraft, and unmanned platforms, feeding real time AoA information to digital flight control computers and mission systems across the operational envelope. Over the 2026-2036 horizon, the defense AoA sensor market is being shaped by the continued operation and modernization of mixed generation fleets that rely on high fidelity stall margin and handling quality inputs.

As air forces adopt advanced multi role fighters and autonomous systems, demand persists for rugged, accurate, and redundant AoA sensors capable of operating under extreme aerodynamic loads, high angles of attack, and harsh environmental conditions. Safety focused incident mitigation and envelope protection programs are driving adoption of multi vane or redundant sensor configurations and integrated health monitoring schemes. At the same time, digital avionics architectures are enabling tighter fusion of AoA data with other air data and inertial sources, making AoA sensors a foundational element of modern flight control and pilot awareness systems in both manned and unmanned platforms.

2. Technology Impact in Defense AoA Sensors Market

Technology is enhancing defense AoA sensors through improved mechanical design, materials, and embedded signal conditioning, rather than replacing them with purely model based estimation. Modern AoA vanes and multi element sensors use advanced alloys and aerodynamic shapes that reduce susceptibility to ice accretion, flutter, and drag interference, improving measurement stability and durability in high speed, high angle of attack regimes. Integrated heaters and ice detection circuits mitigate blockage risks in cold and humid environments, preserving data integrity during critical phases of flight.

Miniaturization and multi redundant configurations allow a single sensor assembly to provide multiple, cross checked AoA channels, supporting fault tolerant architectures required for fly by wire systems. Digitization of sensor outputs and tighter integration with air data computers enable continuous calibration, position error correction, and adaptive gain scheduling based on flight regime. Advanced signal processing algorithms can detect and isolate anomalous vane behavior, reducing the risk of incorrect AoA readings that could trigger unsafe envelope protection responses. At the same time, designers are optimizing sensor location and fairing geometry to minimize interference with surrounding antennas and antennae fields. These innovations collectively raise measurement accuracy, reliability, and operational safety, particularly for high performance and unmanned platforms operating at the edge of the flight envelope.

3. Key Drivers in Defense AoA Sensors Market

The defense AoA sensor market is driven by the need to maintain safe and effective flight control operation across a diverse and often aging fleet of military aircraft and unmanned systems. As air forces continue to operate legacy platforms alongside next generation fighters, trainers, and UAVs, there remains a critical requirement for calibrated, high integrity AoA sensing that supports envelope protection logic, stall avoidance functions, and pilot awareness displays. High profile incidents involving AoA related misbehavior have reinforced the importance of robust, redundant, and heated sensor designs, especially in maritime, high altitude, and high angle attack missions.

Another key driver is the ongoing modernization and life extension of older fleets, which involves replacing worn or obsolete AoA vanes and signal conditioning hardware with units compatible with upgraded digital flight control and avionics architectures. The growth of unmanned combat air and long endurance UAV programs is creating demand for compact, lightweight AoA sensors that can be integrated into smaller airframes without compromising aerodynamic efficiency. Export oriented platforms often require AoA sensors that meet international certification and interoperability standards, encouraging standardized form factors and interface definitions. At the same time, safety regulations and military aviation standards are pushing for higher reliability designs, multi channel redundancy, and integrated health monitoring capabilities, making AoA sensors an integral part of broader flight safety architectures.

4. Regional Trends in Defense AoA Sensors Market

Regionally, North America remains a leading hub for advanced AoA sensor design and production, supported by large scale fighter, trainer, maritime patrol, and unmanned air programs that emphasize stall margin awareness, envelope protection, and integration with digital flight control systems. The United States and its partners operate wide ranging fleets that rely on standardized AoA sensor architectures, fostering demand for robust, multi redundant, and heated designs compatible with both legacy and next generation platforms.

In Europe, collaborative combat air and multi role programs are encouraging the adoption of common AoA sensor standards to support interoperability and shared logistics across national fleets. The Asia Pacific region is witnessing increased demand as several air forces modernize their inventories and expand indigenous UAV and trainer production, prompting local and co development efforts around AoA sensor integration and certification. Middle Eastern and Gulf states, which operate mixed generation fleets in harsh desert and maritime climates, are investing in durable, heated, and ice resistant AoA sensors to sustain reliable angle of attack data. Across regions, there is a growing preference for modular, replaceable sensor units that can be swapped or upgraded without major airframe modifications, alongside designs that minimize electromagnetic interference with nearby avionics and antennas.

5. Key Defense AoA Sensors Market Program

Several flagship defense programs are shaping the evolution of the AoA sensor market over the 2026-2036 period. Next generation fighter and multi role combat air initiatives are specifying advanced AoA sensors integrated tightly with digital flight control systems, enabling precise envelope protection and high angle attack maneuvering capabilities even at the edge of the aerodynamic envelope. Naval aviation and carrier based strike programs require robust AoA sensors capable of operating reliably during high angle of attack approaches and arrested landings in salt laden and turbulent maritime environments.

Unmanned combat air and long endurance UAV programs are adopting compact, lightweight AoA sensors that maintain accuracy across wide speed and angle of attack ranges while minimizing drag and installation complexity. Trainer aircraft programs emphasize standardized AoA sensor designs that mirror frontline platforms, enabling realistic stall margin and elevator authority behavior that reduces pilot transition time overhead. Multinational and coalition level programs are encouraging common AoA sensor interfaces and data formats, supporting shared logistics, certification packages, and replacement in theater strategies. Rotary wing and special mission programs also rely on AoA related data for low level and austere field operations where accurate stall margin awareness is essential for safety. Through these programs, AoA sensors are evolving from simple vanes into engineered, safety critical inputs that underpin modern digital flight control, envelope protection, and autonomous flight architectures.

Table of Contents

Defense Angle of Attack (AoA) Sensors Market - Table of Contents

Defense Angle of Attack (AoA) Sensors Market Report Definition

Defense Angle of Attack (AoA) Sensors Market Segmentation

By Region

By Platform

By Technology

By Output

By Redundancy

Defense Angle of Attack (AoA) Sensors Market Analysis for next 10 Years

The 10-year Defense Angle of Attack (AoA) Sensors Market analysis would give a detailed overview of Defense Angle of Attack (AoA) Sensors Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Angle of Attack (AoA) Sensors Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Angle of Attack (AoA) Sensors Market Forecast

The 10-year Defense Angle of Attack (AoA) Sensors Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Angle of Attack (AoA) Sensors Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Angle of Attack (AoA) Sensors Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Angle of Attack (AoA) Sensors Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Angle of Attack (AoA) Sensors Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Technology, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Technology, 2026-2036

List of Figures

- Figure 1: Global Defense Angle of Attack (AoA) Sensors Market Forecast, 2026-2036

- Figure 2: Global Defense Angle of Attack (AoA) Sensors Market Forecast, By Region, 2026-2036

- Figure 3: Global Defense Angle of Attack (AoA) Sensors Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense Angle of Attack (AoA) Sensors Market Forecast, By Technology, 2026-2036

- Figure 5: North America, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 6: Europe, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 7: Middle East, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 8: APAC, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 9: South America, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 10: United States, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 11: United States, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 12: Canada, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 13: Canada, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 14: Italy, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 15: Italy, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 16: France, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 17: France, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 19: Germany, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 21: Netherlands, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 23: Belgium, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 25: Spain, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 27: Sweden, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 29: Brazil, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 31: Australia, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 32: India, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 33: India, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 34: China, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 35: China, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 39: South Korea, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 41: Japan, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 43: Malaysia, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 45: Singapore, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Angle of Attack (AoA) Sensors Market, Region Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Angle of Attack (AoA) Sensors Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Angle of Attack (AoA) Sensors Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Angle of Attack (AoA) Sensors Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense Angle of Attack (AoA) Sensors Market, By Platform (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Angle of Attack (AoA) Sensors Market, By Platform (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense Angle of Attack (AoA) Sensors Market, By Technology(Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Angle of Attack (AoA) Sensors Market, By Technology(CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense Angle of Attack (AoA) Sensors Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Angle of Attack (AoA) Sensors Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Angle of Attack (AoA) Sensors Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Angle of Attack (AoA) Sensors Market, By Region, 2026-2036

- Figure 58: Scenario 1, Defense Angle of Attack (AoA) Sensors Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Defense Angle of Attack (AoA) Sensors Market, By Technology, 2026-2036

- Figure 60: Scenario 2, Defense Angle of Attack (AoA) Sensors Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Angle of Attack (AoA) Sensors Market, By Region, 2026-2036

- Figure 62: Scenario 2, Defense Angle of Attack (AoA) Sensors Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Defense Angle of Attack (AoA) Sensors Market, By Technology, 2026-2036

- Figure 64: Company Benchmark, Defense Angle of Attack (AoA) Sensors Market, 2026-2036