PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1996999

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1996999

Global Defense IRST (Infra-Red Search & Track) Market 2026-2036

Global Defense IRST (Infra Red Search & Track) Market

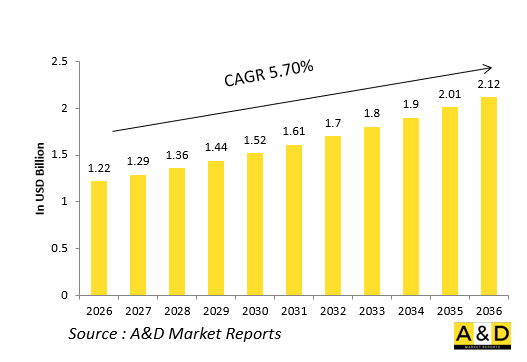

The Global Defense IRST (Infra Red Search & Track) Market is estimated at USD 1.22 billion in 2026, projected to grow to USD 2.12 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 5.70% over the forecast period 2026-2036.

1. Introduction:

Defense Infra Red Search and Track (IRST) systems are passive, long range electro optical sensors that detect and track airborne and surface targets by their infrared signatures, without emitting any active radar emissions. These systems are integrated into fighters, bombers, maritime patrol aircraft, naval vessels, and some ground based air defense platforms, providing stealth preserving situational awareness and early warning in contested environments. Over the 2026-2036 horizon, the IRST market is expanding as armed forces seek to complement traditional radar centric surveillance with passive, low probability of detection sensing capabilities.

Modern IRST suites combine high resolution infrared arrays, advanced signal processing, and multi spectral imaging to detect low observable and stealth shaped aircraft, UAVs, and missiles. They feed real time track data into mission computers and fire control systems, supporting long range engagements, electronic warfare resilient operations, and anti access/area denial scenarios. As the digital battlefield becomes more sensor dense and radar congested, IRST is increasingly viewed as a core layer of integrated air battle management and maritime surveillance architectures, enhancing both survivability and detection range in high threat environments.

2. Technology Impact in Defense IRST Market

Technology is transforming defense IRST systems from relatively narrow field, single band trackers into wide field, multi spectral, AI assisted surveillance nodes. Modern IRST sensors leverage large format infrared detector arrays with higher sensitivity, improved noise reduction, and extended wavelength coverage, enabling earlier detection of small, low observable, and stealth shaped threats. Advanced cooling and optical design techniques enhance image quality and reduce false alarm rates, particularly in complex clutter and maritime backgrounds.

Integration with onboard mission computers and AI assisted tracking algorithms allows IRST systems to perform automated target detection, classification, and data fusion with radar and other sensor inputs. These processors can distinguish between aircraft types, missile signatures, and UAV swarms, reducing operator workload and improving decision speed. Networked architectures enable IRST derived tracks to be shared via datalinks, supporting cooperative engagements and battlespace wide situational awareness. Cyber secure, open architecture designs also support software updates and waveform like reconfiguration, allowing existing IRST hardware to adapt to new threat profiles or mission sets. These innovations collectively raise detection range, survivability, and interoperability, making IRST a central sensor in modern multi domain warfare.

3. Key Drivers in Defense IRST Market

The defense IRST market is driven by the growing need to detect and engage low observable and stealth shaped platforms in environments where active radar use is tactically disadvantageous or electronically vulnerable. As air forces adopt advanced fighters, UAVs, and cruise missile like threats, military planners increasingly rely on passive IRST sensors to maintain long range track coverage without revealing their own position. This requirement is especially pronounced in anti access/area denial scenarios, where early warning and silent tracking are critical for air superiority and layered defense.

Another key driver is the modernization of air and naval fleets, which includes the integration of IRST pods, turrets, and integrated sensor suites into next generation fighters, maritime patrol aircraft, and naval surface combatants. Rising defense expenditures and homeland security demands are also expanding IRST use into border surveillance, critical infrastructure protection, and counter terrorism operations. The push for indigenous capability and reduced foreign dependency in major defense industrial states is encouraging local design and production of IRST systems and subsystems. At the same time, interoperability and standardization initiatives across allied forces are promoting common data formats and networking interfaces, enabling IRST based track sharing in coalition environments. Together, these factors are sustaining strong demand for compact, high performance, and network enabled IRST solutions across air, sea, and land domains.

4. Regional Trends in Defense IRST Market

Regionally, North America remains a leading center for advanced IRST development, underpinned by large scale fighter modernization, maritime surveillance, and air defense programs that emphasize passive, stealth resilient detection. The United States and its partners operate extensive IRST equipped platforms whose procurement contracts typically include multi spectral, AI assisted IRST architectures suitable for long range air superiority and maritime operations.

In Europe, collaborative combat air and multi role programs are driving adoption of common IRST form factors and interface standards, supporting interoperability and shared logistics across national fleets. The Asia Pacific region is emerging as a major growth area, with several countries modernizing their air and naval forces and investing in indigenous IRST technologies to reduce reliance on foreign suppliers. Middle Eastern and Gulf states are investing in advanced sensor equipped platforms whose IRST systems must support long range maritime and regional air defense operations in congested electromagnetic environments. Across these regions, there is a growing preference for modular, open architecture IRST solutions that can be reused or upgraded across fixed wing, rotary wing, naval, and ground based platforms, alongside designs that minimize size, weight, and power while maintaining wide field coverage and low probability of detection operation.

5. Key Defense IRST Market Program

Several flagship defense programs are shaping the IRST market over the 2026-2036 period. Next generation fighter initiatives are specifying advanced IRST sensors integrated into wing mounted pods, nose mounted turrets, or conformal arrays, enabling passive long range detection and tracking of stealth shaped aircraft and UAVs without activating radar. Naval aviation and maritime surveillance programs are equipping patrol and carrier based aircraft with IRST suites that support over water and littoral anti ship missile and drone detection, extending early warning coverage into contested maritime zones.

Naval surface combat and air defense programs are incorporating IRST equipped turrets and integrated sensor masts to enhance passive tracking of low flying threats and anti ship cruise missiles. Ground based air defense and counter UAV programs are deploying IRST based surveillance nodes on fixed and mobile platforms to detect and track small UAVs and loitering munitions in complex urban and mountainous backgrounds. Multinational and coalition level initiatives are standardizing IRST data formats and networking protocols, enabling shared training, exercises, and logistics support across partner nations. Through these programs, IRST systems are evolving from platform specific appendages into integrated, networked layers of the broader multi domain sensing and fire control architecture.

Table of Contents

Defense IRST (Infra-Red Search & Track) Market - Table of Contents

Defense IRST (Infra-Red Search & Track) Market Report Definition

Defense IRST (Infra-Red Search & Track) Market Segmentation

By Region

By Platform

By Detection Range

By Technology

By Wavelength

Defense IRST (Infra-Red Search & Track) Market Analysis for next 10 Years

The 10-year Defense IRST (Infra-Red Search & Track) Market analysis would give a detailed overview of Defense IRST (Infra-Red Search & Track) Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense IRST (Infra-Red Search & Track) Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense IRST (Infra-Red Search & Track) Market Forecast

The 10-year Defense IRST (Infra-Red Search & Track) Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense IRST (Infra-Red Search & Track) Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense IRST (Infra-Red Search & Track) Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense IRST (Infra-Red Search & Track) Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense IRST (Infra-Red Search & Track) Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Detection Range, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Detection Range, 2026-2036

List of Figures

- Figure 1: Global Defense IRST (Infra-Red Search & Track) Market Forecast, 2026-2036

- Figure 2: Global Defense IRST (Infra-Red Search & Track) Market Forecast, By Region, 2026-2036

- Figure 3: Global Defense IRST (Infra-Red Search & Track) Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense IRST (Infra-Red Search & Track) Market Forecast, By Detection Range, 2026-2036

- Figure 5: North America, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 6: Europe, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 7: Middle East, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 8: APAC, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 9: South America, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 10: United States, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 11: United States, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 12: Canada, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 13: Canada, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 14: Italy, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 15: Italy, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 16: France, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 17: France, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 18: Germany, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 19: Germany, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 21: Netherlands, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 22: Belgium, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 23: Belgium, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 24: Spain, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 25: Spain, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 26: Sweden, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 27: Sweden, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 28: Brazil, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 29: Brazil, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 30: Australia, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 31: Australia, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 32: India, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 33: India, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 34: China, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 35: China, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 38: South Korea, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 39: South Korea, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 40: Japan, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 41: Japan, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 43: Malaysia, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 44: Singapore, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 45: Singapore, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense IRST (Infra-Red Search & Track) Market , Region Maturation, 2026-2036

- Figure 47: United Kingdom, Defense IRST (Infra-Red Search & Track) Market , Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense IRST (Infra-Red Search & Track) Market , By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense IRST (Infra-Red Search & Track) Market , By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense IRST (Infra-Red Search & Track) Market , By Platform (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense IRST (Infra-Red Search & Track) Market , By Platform (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense IRST (Infra-Red Search & Track) Market , By Detection Range(Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense IRST (Infra-Red Search & Track) Market , By Detection Range(CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense IRST (Infra-Red Search & Track) Market , Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense IRST (Infra-Red Search & Track) Market , Global Market, 2026-2036

- Figure 56: Scenario 1, Defense IRST (Infra-Red Search & Track) Market , Total Market, 2026-2036

- Figure 57: Scenario 1, Defense IRST (Infra-Red Search & Track) Market , By Region, 2026-2036

- Figure 58: Scenario 1, Defense IRST (Infra-Red Search & Track) Market , By Platform, 2026-2036

- Figure 59: Scenario 1, Defense IRST (Infra-Red Search & Track) Market , By Detection Range, 2026-2036

- Figure 60: Scenario 2, Defense IRST (Infra-Red Search & Track) Market , Total Market, 2026-2036

- Figure 61: Scenario 2, Defense IRST (Infra-Red Search & Track) Market , By Region, 2026-2036

- Figure 62: Scenario 2, Defense IRST (Infra-Red Search & Track) Market , By Platform, 2026-2036

- Figure 63: Scenario 2, Defense IRST (Infra-Red Search & Track) Market , By Detection Range, 2026-2036

- Figure 64: Company Benchmark, Defense IRST (Infra-Red Search & Track) Market , 2026-2036