PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959638

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959638

Semiconductor Plant Construction Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

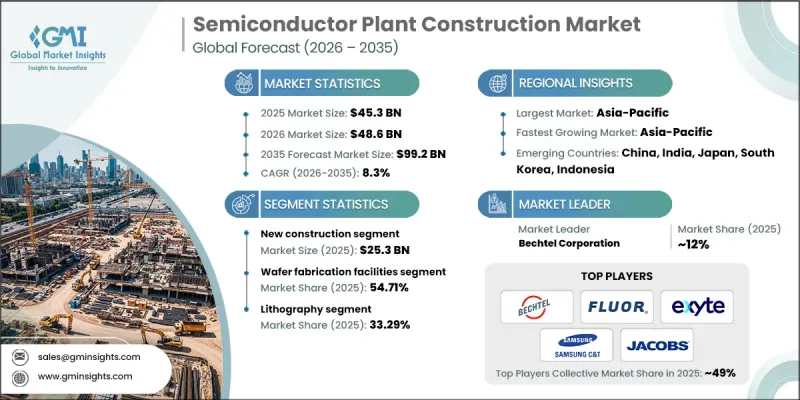

The Global Semiconductor Plant Construction Market was valued at USD 45.3 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 99.2 billion by 2035.

Market growth is driven by rising semiconductor manufacturing demand across both advanced and specialty fabrication facilities. Governments and private investors are allocating significant funding to develop next-generation semiconductor fabs, particularly in emerging economies seeking to strengthen domestic production capabilities. These fabrication plants require highly controlled environments, including advanced cleanrooms and precision HVAC systems designed to meet strict contamination standards. Specialty fabs also demand customized infrastructure and complex utility integration to support niche semiconductor processes. Emerging regions continue to attract capital investment due to cost advantages and policy incentives aimed at expanding high-tech manufacturing. To meet accelerated timelines, contractors increasingly rely on modular and prefabricated construction approaches that enhance efficiency and quality control. Expanding semiconductor capacity is essential for reinforcing global supply chain resilience and addressing rising demand from electronics, automotive, and industrial sectors. Additional momentum is coming from the growth of data centers, artificial intelligence applications, and high-performance computing infrastructure, all of which require increased chip production capacity.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $45.3 Billion |

| Forecast Value | $99.2 Billion |

| CAGR | 8.3% |

The new construction segment generated USD 25.3 billion in 2025 and is forecast to grow at a CAGR of 7.5% between 2026 and 2035. Demand for newly built semiconductor facilities remains strong as manufacturers seek purpose-built plants that support advanced wafer fabrication technologies. Constructing new facilities enables seamless integration of state-of-the-art cleanroom systems, optimized production layouts, and energy-efficient mechanical systems tailored to modern manufacturing requirements. Rising global semiconductor consumption continues to encourage investment in greenfield developments. New construction also ensures compliance with rigorous contamination control protocols, operational safety requirements, and equipment performance standards.

The lithography segment held a 33.29% share and is expected to grow at a CAGR of 7.8% from 2026 to 2035. Lithography systems play a critical role in transferring intricate circuit patterns onto silicon wafers, making them central to advanced semiconductor production. Precision patterning technologies are essential for achieving smaller process nodes and higher device performance. Increasing demand for high-efficiency electronic components and next-generation computing solutions is driving investment in advanced lithography equipment. Technologies such as extreme ultraviolet lithography significantly enhance device density and processing capabilities, contributing to higher construction complexity and specialized equipment installation requirements.

China Semiconductor Plant Construction Market reached USD 8.8 billion in 2025 and is anticipated to grow at a CAGR of 8.8% through 2035. Strong government backing for domestic chip manufacturing and the expansion of advanced electronics infrastructure underpins China's market leadership. Growth in foundry and wafer fabrication capacity has intensified demand for highly precise construction that can support contamination-controlled environments. Developers emphasize modular and scalable facility designs to accelerate project delivery while maintaining compliance with stringent international standards. Expanding production requirements linked to consumer electronics, automotive semiconductor development, and advanced communications networks continue to drive additional construction activity.

Major companies operating in the Global Semiconductor Plant Construction Market include Bechtel Corporation, DPR Construction, Exyte, Fluor Corporation, Gilbane Building Company, Hensel Phelps, Intel Construction, Jacobs Engineering Group, KBR, Inc., PCL Construction, Samsung C&T, SK ecoplant, Skanska, Toyo Engineering Corporation, and Turner Construction Company. Companies active in the semiconductor plant construction industry are strengthening their competitive position through strategic partnerships, technological innovation, and geographic expansion. Leading contractors are investing in advanced project management tools, digital modeling technologies, and modular construction capabilities to accelerate timelines and improve precision. Many firms are forming alliances with semiconductor manufacturers to deliver turnkey solutions that integrate design, engineering, and construction expertise. Expanding operations into emerging markets allows companies to capitalize on government incentives and rising fabrication investments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Burner design

- 2.2.3 Installation

- 2.2.4 Power Range

- 2.2.5 End Use Industry

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global demand for advanced semiconductors across electronics and automotive sectors

- 3.2.1.2 Expansion of data centers, AI, and high-performance computing infrastructure

- 3.2.1.3 Government incentives and subsidies supporting domestic semiconductor manufacturing

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 Extremely high capital expenditure for fab construction and tooling

- 3.2.2.2 Complex regulatory and environmental approval processes

- 3.2.3 Opportunities

- 3.2.3.1 Rising construction of advanced and specialty fabs in emerging regions

- 3.2.3.2 Growing demand for modular cleanroom and prefabricated fab components

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Construction Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 New construction

- 5.3 Expansion

- 5.4 Renovation

Chapter 6 Market Estimates & Forecast, By Facility, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Wafer fabrication facilities

- 6.3 Assembly & test facilities

- 6.4 Research & development facilities

Chapter 7 Market Estimates & Forecast, By Equipment, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Lithography

- 7.3 Deposition

- 7.4 Etching

- 7.5 Chemical mechanical planarization (CMP)

- 7.6 Cleaning

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 Bechtel Corporation

- 9.2 DPR Construction

- 9.3 Exyte

- 9.4 Fluor Corporation

- 9.5 Gilbane Building Company

- 9.6 Hensel Phelps

- 9.7 Intel Construction

- 9.8 Jacobs Engineering Group

- 9.9 KBR, Inc

- 9.10 PCL Construction

- 9.11 Samsung C&T

- 9.12 SK ecoplant

- 9.13 Skanska

- 9.14 Toyo Engineering Corporation

- 9.15 Turner Construction Company