PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1665434

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1665434

Alternative Fuel Injection Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

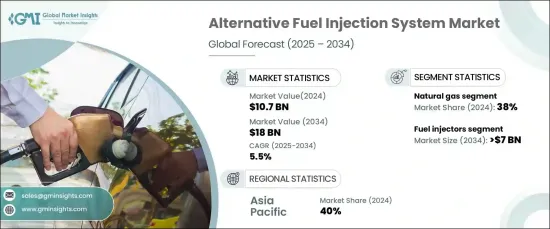

The Global Alternative Fuel Injection Systems Market was valued at USD 10.7 billion in 2024 and is anticipated to grow at a robust CAGR of 5.5% between 2025 and 2034. The rising demand for cost-effective and eco-friendly fuel options, such as natural gas in its compressed (CNG) and liquefied (LNG) forms, is driving this growth. These fuels are increasingly preferred for fleet vehicles like buses and trucks, necessitating advanced injection systems designed to maximize combustion efficiency.

The alternative fuel injection systems market is segmented into electronic control units (ECUs), fuel injectors, fuel rails, and pressure regulators. Among these, the fuel injectors segment dominated in 2024, capturing 40% of the market share, and is projected to reach USD 7 billion by 2034.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.7 Billion |

| Forecast Value | $18 Billion |

| CAGR | 5.5% |

Innovations in injector technology are revolutionizing the market by enabling precise fuel delivery, which improves engine efficiency and reduces waste. The growing demand for durable injectors compatible with alternative fuels like hydrogen and natural gas is further fueled by stricter emission regulations and the ongoing push for performance optimization. Advances in materials science-such as high-strength alloys and protective coatings-are enhancing injector durability and functionality, significantly boosting their adoption.

The market is categorized into hydrogen, LPG, biofuels, natural gas, and other alternatives. In 2024, the natural gas segment held the largest share, accounting for 38% of the market. Its popularity is largely attributed to its affordability and lower carbon emissions compared to traditional fuels, making it an attractive choice for commercial fleets and public transportation. Supportive government policies across North America and Asia-Pacific are accelerating the transition to natural gas, driven by its potential to reduce operational costs and improve sustainability. Advanced fuel injection systems tailored for optimized natural gas combustion are being developed to meet this surging demand.

The Asia-Pacific region accounted for 40% of the alternative fuel injection systems market in 2024, with countries like Japan, India, and South Korea at the forefront of the shift toward cleaner energy solutions. Governments in this region are promoting alternative fuels through various initiatives, including subsidies, tax benefits, and grants. Efforts to combat urban pollution and enhance air quality are further propelling the adoption of advanced fuel injection technologies. With a strong emphasis on sustainability and cleaner transportation, Asia-Pacific is poised to remain a critical driver for market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Pricing analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Stringent government regulations on emissions

- 3.9.1.2 Growing demand for cleaner and sustainable transportation solutions

- 3.9.1.3 Rising adoption of natural gas and hydrogen as alternative fuels

- 3.9.1.4 Technological advancements in fuel injection systems for enhanced performance

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial cost of alternative fuel injection systems

- 3.9.2.2 Limited availability and infrastructure for alternative fuels

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Natural gas

- 5.3 Hydrogen

- 5.4 LPG

- 5.5 Biofuels

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Fuel injectors

- 6.3 Fuel rails

- 6.4 Electronic Control Unit (ECU)

- 6.5 Pressure regulators

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Port injection

- 7.3 Direct injection

- 7.4 Dual fuel systems

- 7.5 Sequential injection

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Sedans

- 8.2.2 Hatchbacks

- 8.2.3 SUVs

- 8.3 Commercial vehicles

- 8.3.1 Light Commercial Vehicles (LCV)

- 8.3.2 Heavy Commercial Vehicles (HCV)

- 8.4 Off-road Vehicles

- 8.4.1 Construction Equipment

- 8.4.2 Mining Equipment

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aptiv

- 11.2 Bosch

- 11.3 Continental

- 11.4 Cummins

- 11.5 Delphi (Phinia)

- 11.6 Denso

- 11.7 Eaton

- 11.8 Honeywell

- 11.9 Infineon

- 11.10 Magneti Marelli

- 11.11 Mitsubishi

- 11.12 Pierburg

- 11.13 Ricardo plc

- 11.14 Schaeffler

- 11.15 Tenneco

- 11.16 Valeo

- 11.17 Weichai

- 11.18 Westport Fuel Systems

- 11.19 Woodward

- 11.20 Zexel