PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1666909

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1666909

Automotive Predictive Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

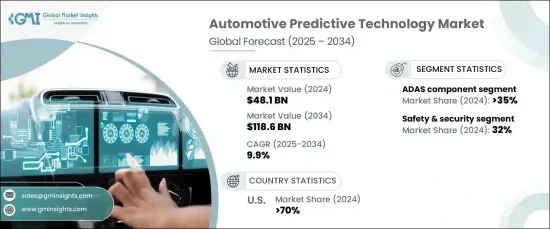

The Global Automotive Predictive Technology Market, valued at USD 48.1 billion in 2024, is expected to experience robust growth at a CAGR of 9.9% from 2025 to 2034. This growth is driven by the increasing demand for advanced safety features and driver assistance systems. Automakers are adopting predictive technologies at an accelerating pace to enhance vehicle safety, prevent accidents, and improve overall driving experiences by analyzing real-time data such as traffic patterns, driver behavior, and vehicle performance. Predictive maintenance has also gained significant traction, allowing for early detection of potential issues to prevent unexpected breakdowns and ensure greater vehicle reliability.

A key factor fueling market expansion is the rise in electric vehicle (EV) adoption. As the automotive industry moves toward greater sustainability, predictive technologies are becoming essential for optimizing EV performance and extending battery life. These technologies use advanced analytics to forecast battery wear, monitor charging habits, and enhance energy efficiency, ensuring optimal performance and longevity of EVs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $48.1 Billion |

| Forecast Value | $118.6 Billion |

| CAGR | 9.9% |

The hardware segment of the market includes ADAS components, OBD devices, and telematics systems. In 2024, ADAS components accounted for 35% of the market share and are expected to generate USD 48 billion by 2034. The increasing demand for automation and safer driving solutions has led to the integration of ADAS features such as adaptive cruise control, lane assist, and collision detection. By leveraging sensors, cameras, radar, and artificial intelligence, these technologies enable vehicles to predict and mitigate risks in real-time, significantly enhancing road safety.

The market is also segmented by applications, including predictive maintenance, vehicle health monitoring, safety and security, and driving pattern analysis. In 2024, the safety and security segment held 32% of the market share, driven by the global focus on reducing traffic fatalities. With human error being a major factor in road accidents, predictive technologies have become crucial in anticipating hazards and improving overall road safety.

The U.S. automotive predictive technology market led the global market with a dominant 70% share in 2024. The country's leadership in developing autonomous vehicles (AVs) and advanced predictive systems has attracted significant investments from automakers and tech companies alike. Predictive technology is crucial for AVs, enabling them to process data from sensors and cameras to navigate complex environments, avoid collisions, and make quick, precise decisions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Automotive OEMs

- 3.1.2 Technology providers

- 3.1.3 Data analytics & cloud service providers

- 3.1.4 End use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Case study

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing demand for vehicle safety & efficiency

- 3.9.1.2 Demand for personalized & connected experiences

- 3.9.1.3 Rapid integration of Artificial Intelligence (AI) and Machine Learning (ML)

- 3.9.1.4 Rising adoption of connected cars

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Data privacy & security concerns

- 3.9.2.2 High implementation costs

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

CHAPTER 4 : Competitive Landscape

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Predictive maintenance

- 5.3 Vehicle health monitoring

- 5.4 Safety & security

- 5.5 Driving pattern analysis

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premise

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By Hardware, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 ADAS component

- 7.3 OBD

- 7.4 Telematics

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Passenger vehicle

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUVs

- 8.3 Commercial vehicles

- 8.3.1 Light Commercial Vehicles (LCVs)

- 8.3.2 Heavy Commercial Vehicles (HCVs)

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 94.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aisin

- 10.2 Aptiv

- 10.3 Bosch

- 10.4 Continental

- 10.5 Garrett Motion

- 10.6 HARMAN

- 10.7 Honeywell

- 10.8 Infineon

- 10.9 Intel

- 10.10 Lear

- 10.11 Magna

- 10.12 Mobileye

- 10.13 NVIDIA

- 10.14 NXP

- 10.15 Qualcomm

- 10.16 Renesas

- 10.17 Siemens

- 10.18 Valeo

- 10.19 Visteon

- 10.20 ZF Friedrichshafen