PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1928911

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1928911

Marine Radar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

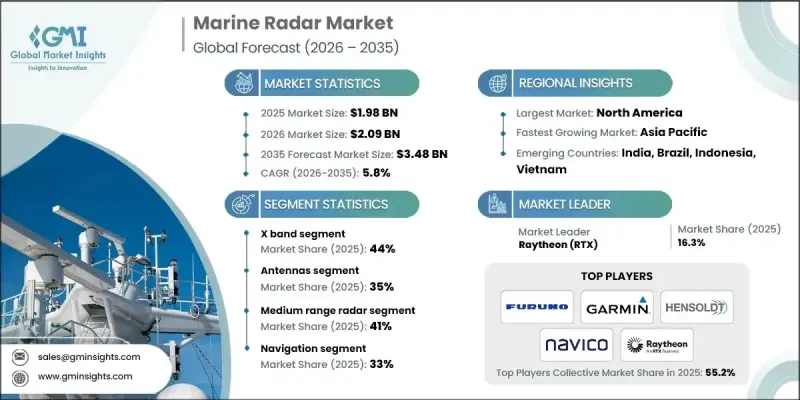

The Global Marine Radar Market was valued at USD 1.98 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 3.48 billion by 2035.

Rising seaborne trade volumes and growing vessel congestion are increasing the need for reliable navigation and surveillance systems. Heightened awareness around maritime accidents in heavily trafficked waterways is encouraging greater investment in advanced radar solutions. Continuous innovation in radar technology is accelerating upgrade cycles, while aging commercial and defense fleets are driving replacement demand. Solid-state radar solutions are increasingly favored due to their durability, operational stability, and reduced maintenance needs. Marine radar systems are now more frequently integrated with electronic charting platforms and vessel identification technologies to improve situational awareness. Expansion of vessel traffic monitoring services is supporting demand for coastal and shore-based radar installations. Growing focus on navigational accuracy in poor visibility conditions is further improving radar performance standards. Fleet modernization initiatives are also contributing to sustained demand for radar replacements.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.98 Billion |

| Forecast Value | $3.48 Billion |

| CAGR | 5.8% |

The X-band segment held a 44% share in 2025 and is forecast to grow at a CAGR of 5.3% from 2026 to 2035. These systems are widely used for navigation support, collision avoidance, and operational control over short to medium ranges. International maritime regulations mandate radar installation on vessels exceeding 300 gross tons, reinforcing segment demand.

The antenna segment accounted for 35% share in 2025 and will grow at a CAGR of 5.3% through 2035. Antennas represent a major share of radar maintenance expenditure, as performance accuracy, detection range, and resolution heavily depend on antenna quality across commercial and fishing fleets.

United States Marine Radar Market held an 88% share and reached USD 574.5 million in 2025. High adoption across commercial shipping, naval operations, and recreational boating, combined with strict maritime safety standards and dense coastal traffic, continues to support ongoing demand for modern radar systems.

Key companies operating in the Global Marine Radar Market include Garmin, Furuno Electric, Raytheon RTX, Kongsberg Gruppen, Raymarine, Navico, Hensoldt, Sperry Marine, JRC Nisshinbo, and Terma. Companies in the Marine Radar Market are strengthening their competitive position by investing heavily in solid-state radar innovation and enhanced signal processing capabilities. Strategic product upgrades focused on higher resolution, improved target detection, and seamless system integration are a core priority. Manufacturers are expanding their aftermarket and service offerings to capture recurring revenue from maintenance and replacement cycles. Partnerships with shipbuilders and fleet operators are helping firms secure long-term supply agreements.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Radar

- 2.2.3 Component

- 2.2.4 Range

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Growth in global seaborne trade

- 3.2.1.3 Stricter maritime safety regulations

- 3.2.1.4 Increasing traffic congestion in coastal and port waters

- 3.2.1.5 Technology upgrades and digital integration

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High installation and maintenance costs

- 3.2.2.2 Signal interference and clutter in congested waters

- 3.2.3 Market opportunities

- 3.2.3.1 Retrofit demand from aging global fleets

- 3.2.3.2 Expansion of offshore wind and offshore energy projects

- 3.2.3.3 Adoption of solid state and digital radar

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States Coast Guard (USCG) Radar Carriage and Observer Requirements

- 3.4.1.2 USCG Approval of Radar Equipment under 46 CFR

- 3.4.1.3 Federal Communications Commission (FCC) Radar Certification Standards

- 3.4.1.4 Canada Transport Canada Marine Radar Compliance Guidelines

- 3.4.2 Europe

- 3.4.2.1 European Maritime Safety Agency (EMSA) Oversight and Implementation

- 3.4.2.2 Marine Equipment Directive (MED) Type Approval Requirements

- 3.4.2.3 EU Flag State and Port State Control Radar Inspections

- 3.4.2.4 Harmonized EN Standards for Radar Equipment

- 3.4.3 Asia Pacific

- 3.4.3.1 China Classification Society (CCS) Radar Type Approval Standards

- 3.4.3.2 India Directorate General of Shipping Radar Compliance Rules

- 3.4.3.3 Japan Ministry of Land Infrastructure Transport Radar Regulations

- 3.4.3.4 South Korea Korean Register of Shipping Radar Requirements

- 3.4.3.5 ASEAN Regional Maritime Safety and Radar Harmonization Guidelines

- 3.4.4 Latin America

- 3.4.4.1 Brazil Maritime Authority (ANtaq) Radar Equipment Standards

- 3.4.4.2 Argentina Prefectura Naval Radar Compliance Regulations

- 3.4.4.3 Mexico Secretariat of Navy and Transport Radar Rules

- 3.4.4.4 Regional SOLAS Implementation and Flag State Controls

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Federal Transport Authority Maritime Radar Standards

- 3.4.5.2 Saudi Arabia Ports Authority Radar Requirements

- 3.4.5.3 South Africa Maritime Safety Authority (SAMSA) Regulations

- 3.4.5.4 Regional Adoption of IMO and IEC Radar Performance Standards

- 3.4.1 North America

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.10.1 Radar system acquisition costs

- 3.10.2 Installation and integration costs

- 3.10.3 Operational and maintenance costs

- 3.10.4 Software upgrade and calibration costs

- 3.10.5 Regulatory certification and type approval costs

- 3.10.6 Training and crew familiarization costs

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Marine radar system architecture & integration framework

- 3.13.1 Standalone vs integrated bridge systems (IBS)

- 3.13.2 Radar integration with ECDIS, AIS, ARPA, and INS

- 3.13.3 Open vs proprietary navigation system architectures

- 3.13.4 Role of radar in sensor fusion environments

- 3.14 OEM differentiation & technology positioning factors

- 3.14.1 Detection range, resolution, and clutter suppression benchmarks

- 3.14.2 Solid-state vs magnetron radar differentiation

- 3.14.3 Software-defined radar capabilities

- 3.14.4 Reliability, MTBF, and lifecycle performance metrics

- 3.15 Retrofit vs newbuild demand dynamics

- 3.16 Impact of SOLAS, IMO & naval procurement standards

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Radar, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 X-band

- 5.3 S-band

- 5.4 C-Band radar

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Transmitters

- 6.3 Antennas

- 6.4 Receivers

- 6.5 Processors

- 6.6 Displays

- 6.7 Other

Chapter 7 Market Estimates & Forecast, By Range, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Short-range radar (1-20 NM)

- 7.3 Medium-range radar (20-50 NM)

- 7.4 Long-range radar (50-100 NM and above)

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Navigation

- 8.3 Collision Avoidance

- 8.4 Surveillance & Security

- 8.5 Fishing Operations

- 8.6 Monitoring Coastal Traffic

- 8.7 Weather Monitoring

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Commercial vessels

- 9.3 Naval & Defense / Military Naval

- 9.4 Recreational Boats / Yachts

- 9.5 Private boat owners

- 9.6 Fishing vessels

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Netherlands

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 BAE Systems

- 11.1.2 Furuno Electric

- 11.1.3 Garmin

- 11.1.4 Hensoldt

- 11.1.5 Kongsberg Gruppen

- 11.1.6 Leonardo

- 11.1.7 Lockheed Martin

- 11.1.8 Navico

- 11.1.9 Northrop Grumman

- 11.1.10 Raymarine

- 11.1.11 Raytheon RTX

- 11.1.12 Saab

- 11.1.13 Sperry Marine

- 11.1.14 Teledyne FLIR

- 11.1.15 Thales

- 11.2 Regional Players

- 11.2.1 GEM Elettronica

- 11.2.2 JRC Nisshinbo

- 11.2.3 Koden Electronics

- 11.2.4 Samyung ENC

- 11.2.5 TOKIO KEIKI

- 11.3 Emerging Players/Disruptors

- 11.3.1 Alphatron Marine

- 11.3.2 Rutter

- 11.3.3 Terma