PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998718

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998718

BTK Inhibitor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

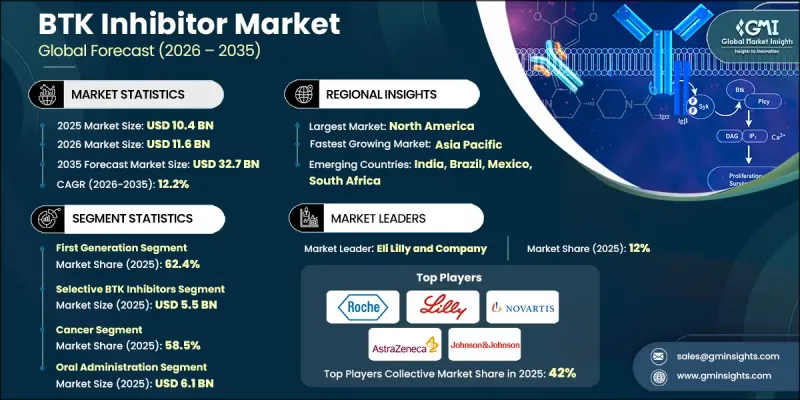

The Global BTK Inhibitor Market was valued at USD 10.4 billion in 2025 and is estimated to grow at a CAGR of 12.2% to reach USD 32.7 billion by 2035.

The consistent growth is supported by the increasing burden of cancer and autoimmune disorders worldwide, along with notable progress in targeted drug development. Pharmaceutical research has increasingly shifted toward therapies designed to precisely target molecular pathways associated with disease progression, which has elevated the clinical relevance of BTK inhibitors. The rising adoption of personalized medicine approaches is further encouraging the development of therapies tailored to specific genetic mutations, biomarker-guided treatment methods, and optimized dosing strategies. In addition, continued innovation in drug discovery is enabling the development of next-generation BTK inhibitors capable of addressing treatment resistance and improving therapeutic outcomes. BTK inhibitors function by blocking Bruton's tyrosine kinase, an enzyme that plays a central role in regulating the survival and activity of B-cells within the immune system. By suppressing abnormal B-cell signaling, these therapies help control disease progression in several hematological conditions and immune-related disorders. Over time, BTK inhibitors have become an important component of modern targeted therapy strategies, significantly influencing treatment protocols for multiple malignancies and immune system disorders.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.4 Billion |

| Forecast Value | $32.7 Billion |

| CAGR | 12.2% |

The first-generation segment reached USD 6.5 billion in 2025 and held 62.4% share. Early BTK inhibitor therapies demonstrated substantial clinical effectiveness in treating several B-cell-related conditions. Their adoption significantly improved treatment outcomes by slowing disease progression and extending patient survival. Another factor supporting the widespread use of first-generation BTK inhibitors is their convenient oral administration, which offers a less invasive alternative to traditional intravenous therapies. Oral treatment options improve patient comfort and simplify long-term disease management, leading to better treatment adherence and higher compliance rates. These therapies also work by specifically targeting Bruton's tyrosine kinase, an essential enzyme involved in B-cell receptor signaling pathways, which helps reduce many of the adverse effects often associated with conventional chemotherapy approaches.

The selective BTK inhibitors segment accounted for 52.5% share and generated USD 5.5 billion in 2025. These therapies are designed to target Bruton's tyrosine kinase with a higher degree of precision compared with earlier treatment approaches. Their improved specificity allows the drugs to focus more effectively on the intended molecular pathway while limiting interaction with unrelated kinases. As a result, the risk of off-target biological effects is reduced. Another advantage of selective BTK inhibitors is their favorable safety profile, particularly for patients who require long-term therapy or have existing health conditions that demand more carefully managed treatment options. The development of highly selective therapies reflects the broader industry trend toward precision medicine and more refined therapeutic strategies.

United States BTK Inhibitor Market was valued at USD 3.8 billion in 2025, supported by a well-established pharmaceutical research ecosystem and a strong demand for advanced targeted therapies. Increasing cancer prevalence in the United States continues to generate significant demand for targeted therapeutic solutions capable of improving treatment effectiveness. Regulatory oversight from the U.S. Food and Drug Administration has also played an important role in shaping the BTK inhibitor landscape by maintaining strict approval standards for safety, performance, and drug quality. These regulatory requirements encourage pharmaceutical companies to develop more advanced therapies that meet evolving clinical expectations while ensuring patient safety.

Key participants active in the Global BTK Inhibitor Market include Novartis, Bristol Myers Squibb, Johnson & Johnson, Amgen, AstraZeneca, Merck & Co., Sanofi, Takeda Pharmaceutical, F. Hoffmann-La Roche Ltd, Gilead Sciences, Eli Lilly and Company, Incyte, Biogen, Celgene, and Agilent Technologies. Companies operating in the BTK Inhibitor Market are implementing multiple strategic initiatives to strengthen their competitive positioning. Leading pharmaceutical firms are prioritizing extensive research and development investments to discover improved BTK inhibitor formulations with greater selectivity and enhanced therapeutic performance. Strategic collaborations with biotechnology companies, academic institutions, and clinical research organizations are also being pursued to accelerate drug development and clinical trial programs. Many companies are expanding their oncology and immunology pipelines through acquisitions, licensing agreements, and technology partnerships that support innovation in targeted therapies. In addition, firms are strengthening regulatory approval strategies and increasing global commercialization capabilities to broaden their geographic reach.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.2 Research transparency addendum

- 1.7.3 Source attribution framework

- 1.7.4 Quality assurance metrics

- 1.7.1 Quantified market impact analysis

- 1.8 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Drug type trends

- 2.2.4 Application trends

- 2.2.5 Route of administration trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cancers and autoimmune diseases

- 3.2.1.2 Advancements in targeted therapies

- 3.2.1.3 Ongoing research and development

- 3.2.1.4 Increasing focus on personalized medicine

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of BTK inhibitors

- 3.2.2.2 Stringent regulatory scenario

- 3.2.3 Market opportunities

- 3.2.3.1 Rising healthcare infrastructure in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Future market trends

- 3.6 Pipeline analysis (Driven by Primary Research)

- 3.7 Pricing analysis, 2025

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 First generation

- 5.3 Second generation

Chapter 6 Market Estimates and Forecast, By Drug Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Selective BTK inhibitors

- 6.3 Non-selective BTK inhibitors

- 6.4 Dual BTK inhibitors

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Cancer

- 7.2.1 Chronic lymphocytic leukemia (CLL)

- 7.2.2 Follicular lymphoma

- 7.2.3 Mantle cell lymphoma

- 7.2.4 Marginal zone lymphoma

- 7.2.5 Small lymphocytic lymphoma (SLL)

- 7.2.6 Waldenstrom macroglobulinemia

- 7.2.7 Other selective B cell malignancies

- 7.3 Autoimmune diseases

- 7.3.1 Systemic lupus erythematosus (SLE)

- 7.3.2 Rheumatoid arthritis (RA)

- 7.3.3 Multiple sclerosis (MS)

- 7.3.4 Immune thrombocytopenia (ITP)

- 7.4 Inflammatory disorders

- 7.4.1 Inflammatory bowel disease (IBD)

- 7.4.2 Asthma and allergic diseases

- 7.4.3 IgG4-Related diseases

- 7.4.4 Vasculitis

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Oral administration

- 8.3 Intravenous administration

- 8.4 Subcutaneous administration

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital pharmacy

- 9.3 Retail pharmacy

- 9.4 Online pharmacy

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Amgen

- 11.2 AstraZeneca

- 11.3 Agilent Technologies

- 11.4 BristolMyers Squibb

- 11.5 Celgene

- 11.6 Biogen

- 11.7 Eli Lilly and Company

- 11.8 F. Hoffmann-La Roche Ltd

- 11.9 Gilead Sciences

- 11.10 Johnson and Johnson

- 11.11 Incyte

- 11.12 Merck and Co

- 11.13 Novartis

- 11.14 Sanofi

- 11.15 Takeda Pharmaceutical