PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1708166

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1708166

Plastic Drums Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

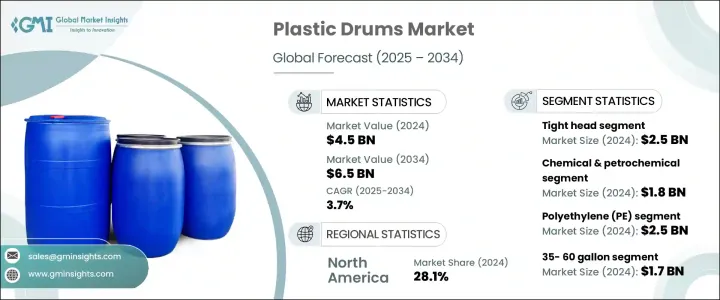

The Global Plastic Drums Market generated USD 4.5 billion in 2024 and is projected to expand at a CAGR of 3.7% between 2025 and 2034. This growth trajectory is largely fueled by the surging demand for plastic drums across industries such as chemicals, food and beverage, pharmaceuticals, and paints and coatings, among others. As businesses worldwide continue to focus on efficient, durable, and cost-effective packaging solutions, plastic drums are gaining momentum as a preferred choice for storing and transporting a wide range of materials, including hazardous and non-hazardous substances.

With increasing emphasis on safe and compliant packaging for industrial products, the adoption of plastic drums has witnessed significant growth. The market benefits from rising industrialization, growing international trade, and the need for reliable bulk packaging options that meet regulatory and safety standards. Moreover, as supply chain networks grow more complex and globalized, the need for robust, reusable, and secure containers becomes imperative, positioning plastic drums as a versatile solution across multiple verticals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.5 Billion |

| Forecast Value | $6.5 Billion |

| CAGR | 3.7% |

The chemical industry continues to be a major driver of plastic drums demand, primarily for handling petrochemicals, fertilizers, and specialty chemicals. Industries in these sectors require heavy-duty, highly durable containers to store and transport liquids and powders safely. As regulatory bodies enforce stringent guidelines for the storage and transportation of hazardous substances, the preference for plastic drums that offer leak-proof, corrosion-resistant, and safe packaging solutions is rising. These drums not only ensure the safe handling of dangerous goods but also comply with environmental and safety regulations, making them essential across chemical supply chains.

Plastic drums are mainly categorized into open head and tight head types, each serving specific industrial needs. The tight head drum segment generated USD 2.5 billion in 2024, driven by rising demand for packaging hazardous liquids, oils, and solvents. Tight head drums feature sealed lids and narrow openings, which make them ideal for long-distance transportation under harsh conditions, preventing leaks or contamination. The segment continues to gain traction due to stringent safety mandates by authorities like the DOT and FDA, ensuring compliance when handling flammable and hazardous materials. As global trade in chemicals and oils grows, tight head drums are increasingly recognized for offering durable, tamper-resistant solutions that ensure product integrity throughout transport.

Based on end-use industries, the chemical and petrochemical segment generated USD 1.8 billion in 2024, owing to the rising need for secure, leak-proof containers to store and transport chemicals, fuels, and solvents. Regulatory standards and environmental concerns have led to growing reliance on plastic drums for efficient and safe packaging across industrial ecosystems.

The U.S. Plastic Drums Market alone generated USD 1.1 billion in 2024, with expansion in chemical manufacturing and bulk storage solutions being key drivers. The growing need for safe and efficient transportation across industries keeps demand steady, cementing the role of plastic drums in supporting modern industrial supply chains.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in E-commerce and global trade

- 3.2.1.2 Rising demand from chemical industry

- 3.2.1.3 Cost effectiveness and durability

- 3.2.1.4 Rapid expansion of food and beverage industry

- 3.2.1.5 Agriculture sector reliance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Raw materials price volatility

- 3.2.2.2 Competition from alternative materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Polyethylene (PE)

- 5.2.1 High-Density Polyethylene (HDPE)

- 5.2.2 Low-Density Polyethylene (LDPE)

- 5.3 Polypropylene (PP)

- 5.4 Polyethylene Terephthalate (PET)

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Capacity, 2021 – 2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Below 35 gallons

- 6.3 35-60 gallons

- 6.4 60-80 gallons

- 6.5 Above 80 gallons

Chapter 7 Market Estimates and Forecast, By Head Type, 2021 – 2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Open head

- 7.3 Tight head

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 Chemical and petrochemical

- 8.3 Food and beverage

- 8.4 Pharmaceuticals

- 8.5 Paints and coatings

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 C.L. Smith

- 10.2 Cospak

- 10.3 CurTec

- 10.4 Eagle Manufacturing

- 10.5 FDL Packaging Group

- 10.6 Fries KT

- 10.7 Greif

- 10.8 Jiangsu Xinhuasheng Packaging New Materials

- 10.9 Jiangsu Xuan Sheng Plastic Technology

- 10.10 Kodama Plastics

- 10.11 Mauser Packaging Solutions

- 10.12 Muller Group

- 10.13 Nova Chemicals

- 10.14 P. Wilkinson Containers

- 10.15 Pyramid Technoplast

- 10.16 Schutz

- 10.17 Snyder Industries

- 10.18 The Cary Company

- 10.19 Time Technoplast

- 10.20 US Coexcell