PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1716597

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1716597

Prostate Cancer Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

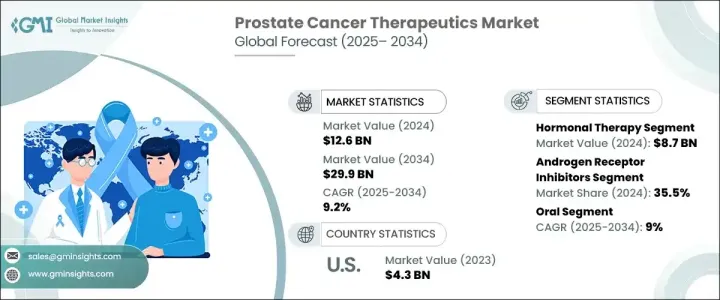

The Global Prostate Cancer Therapeutics Market generated USD 12.6 billion in 2024 and is projected to expand at a CAGR of 9.2% from 2025 to 2034. The market is witnessing significant momentum, primarily driven by the growing prevalence of prostate cancer worldwide, coupled with increasing awareness around early diagnosis and effective treatment options. With prostate cancer ranking among the most common cancers in men, healthcare systems are focusing on adopting advanced therapeutics to improve patient outcomes. The aging male population, rising incidence rates, and a surge in patient awareness through government-led initiatives and cancer advocacy groups continue to foster market growth.

Moreover, innovations in precision medicine and the integration of advanced diagnostic tools like genomic testing, biomarker identification, and AI-powered imaging are revolutionizing prostate cancer detection and treatment planning. Pharmaceutical giants are heavily investing in research and development to introduce novel drugs and personalized therapies that can effectively target resistant forms of prostate cancer, offering renewed hope for patients with advanced disease stages. Additionally, the increased emphasis on combination therapies and the adoption of immunotherapies are transforming the therapeutic landscape, making way for safer and more efficient treatment modalities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.6 Billion |

| Forecast Value | $29.9 Billion |

| CAGR | 9.2% |

The market is segmented based on different therapeutic approaches, including hormonal therapy, chemotherapy, immunotherapy, targeted therapy, and other treatment options. In 2024, hormonal therapy led the market, generating USD 8.7 billion in revenue. Hormonal therapy remains a cornerstone in prostate cancer management as it plays a crucial role in controlling the disease's progression by lowering androgen hormone levels. These hormones, especially testosterone, are known to fuel prostate cancer growth. By targeting and suppressing testosterone production, hormonal therapies significantly reduce tumor size and alleviate symptoms, which contributes to improved patient survival rates. The growing adoption of next-generation hormonal agents that are more effective in advanced and resistant cases has further cemented the dominance of this therapeutic segment in the global market.

Based on drug classes, androgen receptor inhibitors (ARIs) accounted for 35.5% of the market share in 2024. ARIs have emerged as a vital treatment option for patients with advanced prostate cancer, especially those who no longer respond to traditional androgen deprivation therapy (ADT). These inhibitors work by blocking the androgen receptor signaling pathway, thereby preventing cancer cells from utilizing androgens for growth. The increased use of ARIs in both early and late-stage prostate cancer treatment has shown improved clinical outcomes, making them indispensable in the current therapeutic arsenal. The introduction of new ARIs with enhanced efficacy and safety profiles is also expected to boost their adoption over the coming years.

North America dominated the global prostate cancer therapeutics market with a 39.2% share in 2024. The region's leadership position is largely attributed to its advanced healthcare infrastructure, cutting-edge cancer care centers, and strong focus on oncology research. High levels of public and private investments, along with collaborative efforts between pharmaceutical companies and research institutions, are continuously propelling innovation in prostate cancer treatment across the region.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of prostate cancer

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rising awareness and screening programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Side effects associated with treatment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Pipeline analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.10 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Therapy, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hormonal therapy

- 5.3 Chemotherapy

- 5.4 Immunotherapy

- 5.5 Targeted therapy

- 5.6 Other therapies

Chapter 6 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Androgen receptor inhibitors

- 6.3 GnRH receptor antagonists

- 6.4 PARP inhibitors

- 6.5 Immune checkpoint inhibitors

- 6.6 Other drug classes

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacy

- 8.3 Brick and mortar

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Astellas Pharma

- 10.2 AstraZeneca

- 10.3 Bayer

- 10.4 Dendreon Pharmaceuticals

- 10.5 Exelixis

- 10.6 Ferring

- 10.7 GlaxoSmithKline

- 10.8 Ipsen Pharma

- 10.9 Johnson & Johnson

- 10.10 Novartis

- 10.11 Pfizer

- 10.12 Sanofi

- 10.13 Sumitomo Pharma America

- 10.14 Takeda Pharmaceutical

- 10.15 Tolmar