PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1721411

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1721411

Edge Artificial Intelligence Chips Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

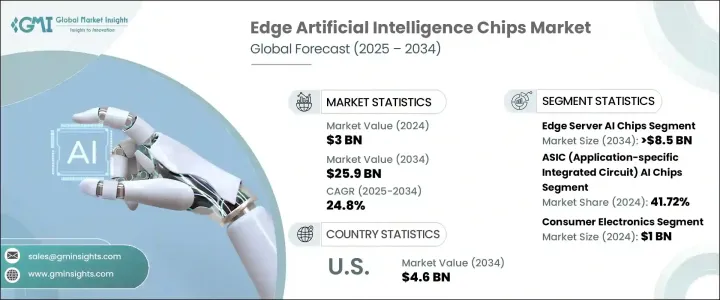

The Global Edge Artificial Intelligence Chips Market was valued at USD 3 billion in 2024 and is estimated to grow at a CAGR of 24.8% to reach USD 25.9 billion by 2034. This significant growth reflects a dynamic shift in computing paradigms, where real-time intelligence at the device level is rapidly becoming the norm. As enterprises continue to digitize operations, the demand for high-performance AI chipsets that can process data locally is surging. This evolution is particularly pronounced in sectors such as autonomous driving, smart manufacturing, and precision healthcare, where decisions must be made instantly without reliance on cloud latency. Edge AI chips enable smart devices to process, analyze, and act on data at the source, offering faster response times and improved data privacy.

With AI penetrating deeper into consumer electronics, industrial systems, and smart infrastructure, the demand for scalable, energy-efficient AI hardware is intensifying. Furthermore, advancements in fabrication technology, miniaturization of components, and growing access to 5G networks are accelerating the deployment of edge AI solutions worldwide. Companies are increasingly viewing edge AI as the key to unlocking transformative capabilities in robotics, augmented reality, and intelligent surveillance. The combination of decentralized intelligence and edge computing is redefining how data is used and secured, presenting a tremendous opportunity for chipmakers and system integrators alike.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3 Billion |

| Forecast Value | $25.9 Billion |

| CAGR | 24.8% |

The market is segmented by deployment into on-device and edge server AI chips. Edge server AI chips are projected to generate USD 8.5 billion by 2034 as industries increasingly prioritize low-latency AI operations and localized data processing. Use cases like real-time traffic monitoring in smart cities, predictive maintenance in manufacturing, and advanced diagnostics in healthcare are pushing demand for robust edge servers. The rollout of 5G infrastructure is also enhancing edge server accessibility and bandwidth, making them more viable for hosting complex AI workloads close to end-users.

In terms of chip type, application-specific integrated circuits (ASICs) dominate the landscape, capturing a 41.72% share in 2024. These chips offer unmatched performance for targeted AI applications, making them a top choice for functions like speech recognition, computer vision, and NLP. Their energy efficiency and processing speed continue to attract AI hardware developers who need scalable, cost-effective solutions for mass deployment.

The U.S. Edge Artificial Intelligence Chips Market was valued at USD 4.6 billion in 2024, largely driven by innovation in autonomous systems, military-grade technology, and smart manufacturing. Leading tech firms are heavily investing in AI chip R&D to develop advanced capabilities for healthcare wearables, automated security, and industrial robotics. Government initiatives such as the CHIPS Act are further amplifying growth by funding semiconductor development and ensuring supply chain resilience for critical AI technologies.

Leading companies in the Global Edge Artificial Intelligence Chips Market include Qualcomm Technologies, NVIDIA Corporation, Arm Limited, Advanced Micro Devices, Inc., Broadcom Inc., Apple, STMicroelectronics, Texas Instruments Incorporated, MediaTek Inc., Lattice Semiconductor, Mythic, Marvell, Synaptics Incorporated, BrainChip, Inc., HAILO TECHNOLOGIES LTD, Huawei Cloud Computing Technologies Co., Ltd, and Intel Corporation. Companies are actively investing in R&D to reduce chip power consumption and enhance processing efficiency. Many are expanding manufacturing operations to meet escalating demands from the IoT, autonomous vehicle, and smart infrastructure sectors.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for semiconductors

- 3.2.1.2 Surge in IoT adoption

- 3.2.1.3 Rising need for low-latency processing

- 3.2.1.4 Expansion of 5G networks

- 3.2.1.5 Growing demand for AI in consumer electronics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High power consumption and thermal management

- 3.2.2.2 Complex hardware and software integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Chip Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 ASIC (Application-Specific Integrated Circuit) AI Chips

- 5.3 GPU (Graphics Processing Unit) AI Chips

- 5.4 CPU (Central Processing Unit) AI Chips

- 5.5 FPGA (Field-Programmable Gate Array) AI Chips

- 5.6 Neuromorphic AI Chips

Chapter 6 Market Estimates and Forecast, By Deployment, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 On-Device Edge AI Chips

- 6.3 Edge Server AI Chips

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Consumer electronics

- 7.3 Automotive & transportation

- 7.4 Healthcare & medical devices

- 7.5 Retail & e-commerce

- 7.6 Manufacturing & industrial automation

- 7.7 Telecommunications

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 ANZ

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Advanced Micro Devices, Inc.

- 9.2 Apple

- 9.3 Arm Limited

- 9.4 BrainChip, Inc.

- 9.5 Broadcom Inc.

- 9.6 HAILO TECHNOLOGIES LTD

- 9.7 Huawei Cloud Computing Technologies Co., Ltd

- 9.8 Intel Corporation

- 9.9 Lattice Semiconductor

- 9.10 Marvell

- 9.11 MediaTek Inc

- 9.12 Mythic

- 9.13 NVIDIA Corporation

- 9.14 Qualcomm Technologies

- 9.15 STMicroelectronics

- 9.16 Synaptics Incorporated

- 9.17 Texas Instruments Incorporated